Corporate dark arts: mulligans, midstream cuts, and one fast double $AGL $TPB $DUOL $COTY $RIVN

Corporate dark arts, part 12

Today’s post is the 12th post in my “corporate dark arts” series1. Today, I want to highlight a few more interesting case studies; while I don’t think any of these are imminently actionable, I think all of them are instructive in some way, shape, or form, and sharing them will help you better understand the dark arts going forward. The cases are:

AGL: another proof point that these can work FAST

RIVN gets a mulligan

COTY’s midstream adjustment

DUOL: what happens when you halfway vest?

TPB’s CEO chooses stock

Let’s dive in.

AGL: another proof point that these can work FAST

On April 27, AGL hired a new CEO. His contract had 200k PSUs that started to vest at $50 and vested in full at $150. Given the stock was trading <$30 at the time, it was a pretty bullish signal.

On May 6, the company reported blow out earnings. The stock more than doubled, and it’s almost doubled again. Not only are the first set of PSUs set to vest imminently, but it seems like the second set might vest before the summer is over!

RIVN gets a mulligan

One of the issues with the “dark arts” is management can turn it into “heads, I win; tails, I try again and then win” pretty easily: give yourself an aggressive stock grant…. and then if you miss it give yourself another one! Thus, there is no signal in a dark arts grant because management is greedy and will just keep giving themselves packages until they get fabulously wealthy, fairness (and shareholders!) be damned.

Rivian serves as a nice example. They gave their CEO a massive package in the boom days when they deSPAC’d…. but with the stock getting hammered and the CEO going through a divorce, they just reloaded him with a $400m package that would be worth >$4B if it vests in full.

The option targets are definitely aggressive….

But if you’re a shareholder, you have to ask yourself: is this package a one time thing meant to incentivize a CEO to pursue a massively value accretive path that insiders are seeing? Or will the board just keep handing these big packages out until one of them pays out?

COTY’s midstream adjustment

COTY pairs well with the RIVN example; instead of a mulligan, COTY appears to have slow walked setting the actual terms of their new CEO’s pay package to adjust for the business melting down as he took the reins.

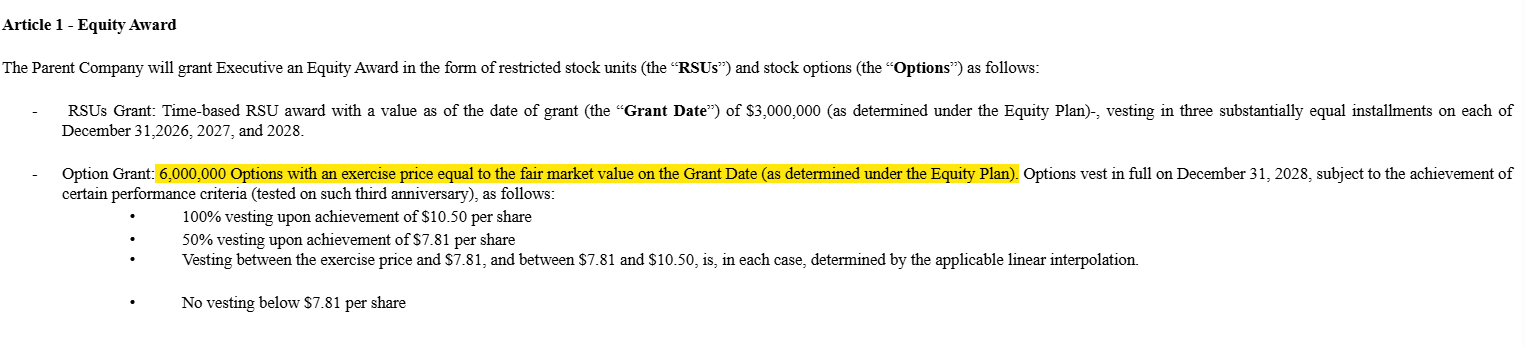

Let’s back up; here’s a little secret: sometimes a company will make an executive hire and they won’t give all of the details in the 8-K. When that happens, it’s worth tracking closely to see what’s going on. That’s exactly what happened with COTY; they brought in a new exec chair and interim CEO in late December. His contract called for 6m performance options to be granted, but it didn’t detail what the performance criteria for those options were. COTY buried the performance criteria in their next 10-Q, and they are aggressive. COTY’s stock was trading for ~$3/share when the options were granted (and that’s where they are struck); the stock needs to hit $7.81/share for anything to vest, and full vesting isn’t until $10.50. If the options do vest in full, they’d be worth just shy of $50m pretax. Again, aggressive. Also interesting that the bottom end of the vest is $7.81/share; that is a strange number. How was that specific number chosen? Does management and the board have some view or inside information that informed that number?

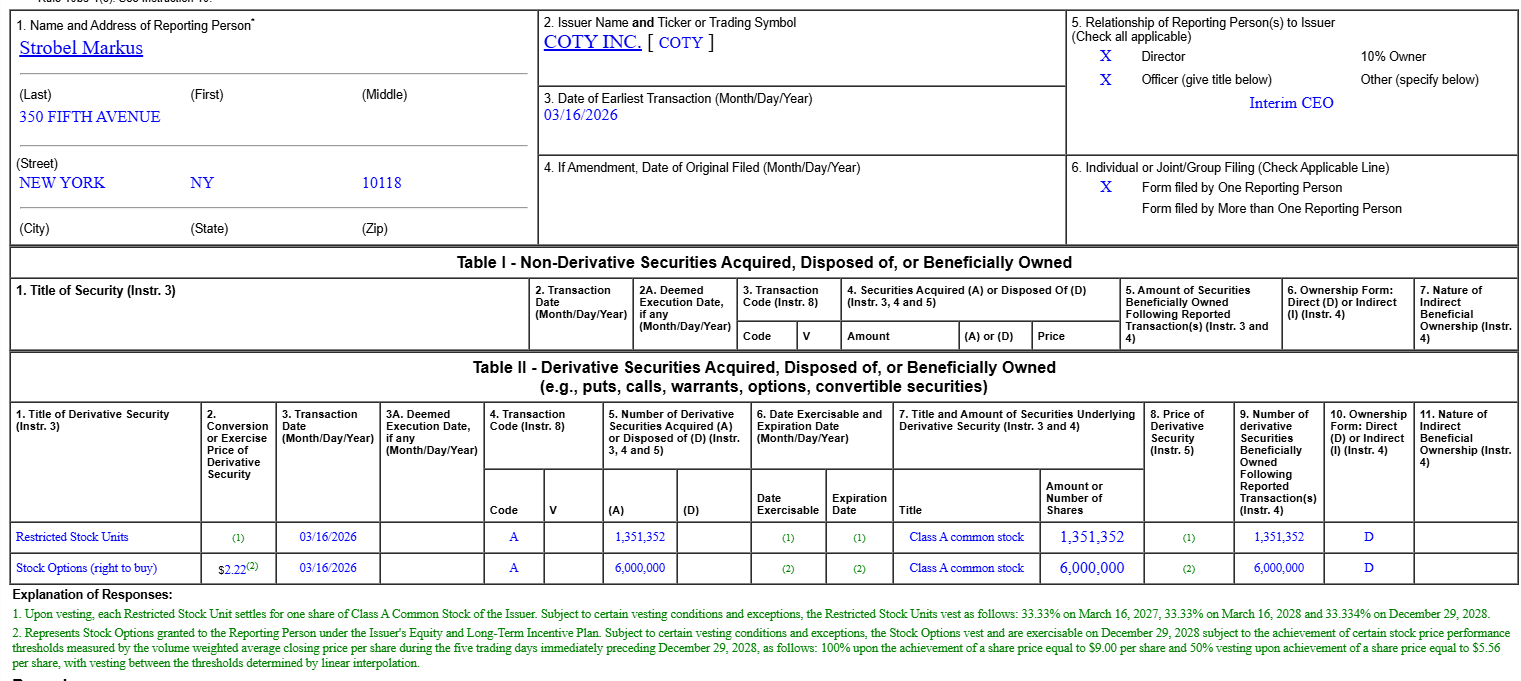

Even more interesting, the exec chair / interim CEO didn’t file a Form 4 until March 18 (the same day COTY revamped their whole board). Curiously, if you read footnote 2, both the strike price and the option vesting prices appear to have been nudged down (the strike from the ~$3/share COTY was trading for in December to its current price around $2/share; the vesting from $7.81 on the low end to $5.56/share). Makes you wonder what the company was seeing to adjust all of these down midstream…. though perhaps worth noting that this package (and the adjustments) keeps the CEO in line for a ~$50m payout if he vests the full high end.

DUOL: what happens when you halfway vest?

I was reading my friend Adam Wilk’s DUOL write up, and he had this table on the PSU DUOL’s CEO got at the time of the IPO.

As I write this, DUOL’s stock is trading for ~$108/share.

Which creates a kind of interesting hypothetical: if a CEO vests ~half of their PSUs and then the stock falls off a cliff, do they have a perverse incentive structure now? Are they incentivized to lever up to try to increase volatility and hit the out of the money options? Or are they incentivized to tamp down volatility and hold on to what they’ve already vested?

I’m not saying either is the case at DUOL; the CEO owns enough stock outside of the PSU grants that he’s probably pretty aligned / not suffering from perverse incentives. But it’s fascinating to think about, and the DUOL structure provides a nice little hypothetical even if it doesn’t fit perfectly!

TPB’s CEO chooses stock

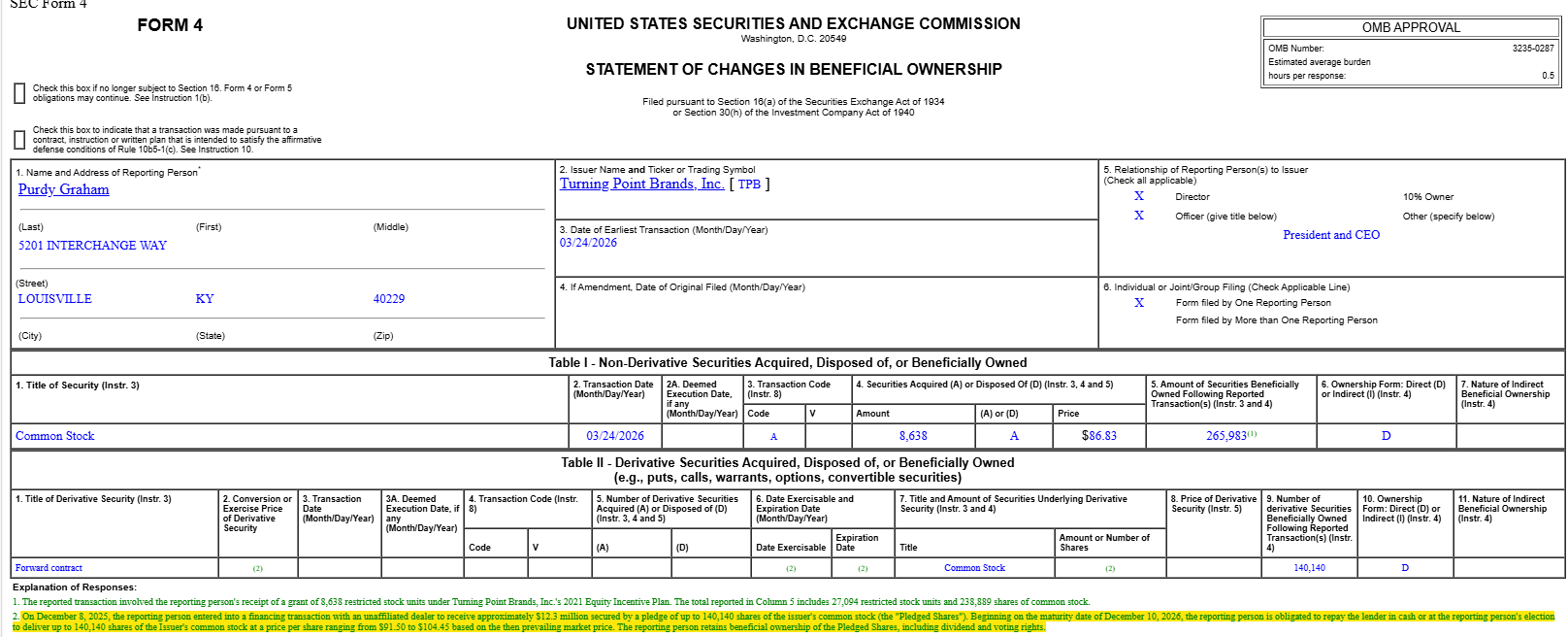

Sometimes, the signal is not in the action… it’s in how an action changes. Consider TPB: earlier this year, their CEO took his 2025 bonus in RSUs2 with the stock in the mid-$80s/share. Plenty of executives do that…. what’s noteworthy is that he took the bonus in cash in 2024.

Sure enough, Q1 earnings crushed, and the CEO managed to increase his bonus by >10% by taking stock instead of cash.

Side note: the CEO engaged in an interesting forward swap on >$12m of stock that settles in cash or shares; I could definitely see how a swap like this incentivizes him to keep the stock price elevated this year, but I haven’t fully thought it through…

/Fin

Ok, that’s it for post 12. I’ll be back next week with post 13 to wrap the series up with high level takeaways. Don’t forget to sign up to make sure you don’t miss the conclusion of the series (or any future posts)!

Previous posts include RELY + OPEN’s pay package, META’s YOLO options, incentives gone awry, an analysis of LION + STRZ new packages, five more dark arts ideas, dark arts clues $SOX was about to go parabolic, the ACHC case study + premium dark arts basket, the incentives driving moves at VAC/GME/EKSO/RPD, five grants that aren’t as bullish as they appear, and this premium writeup on my favorite current dark arts setup.

“Mr. Purdy received a 2025 bonus valued at $750,000, which was paid through the issuance of 8,638 restricted stock units (RSUs) under the Company’s 2021 Equity Incentive Plan in lieu of cash.”

thanks for the article. It would seem that the lower price adjustment for Coty doesn't instill confidence of a turnaround . Thoughts? Thanks

really enjoying this series Andrew 👍