Corporate dark arts: when incentives tell you what might be coming $GME $EKSO $VAC $RPD

Corporate Dark Arts part 9

Today's post includes yet another case study that the dark arts1 can work fast (EKSO), confirmation that boards get what they incentivize (GME), and two of the more torqued (and active!) setups I'm following (VAC, RPD2).

Let’s dive in.

Case study: Yeah, incentives matter (GME)

Friday afternoon, the WSJ broke a report that GME is looking to buy eBay. It’s an audacious “fish that swallowed the whale” potential deal; GME's market cap is ~$10b and EBAY's is ~$50b.

I noted last month that GME’s new exec comp package encouraged absolute growth in market cap and EBITDA with no regard to per share value. Perhaps I’m a jaded skeptic, but I can’t help but note that the board is (potentially) getting exactly what they encouraged with this deal.

If a GME / EBAY deal comes to pass, I’ll be surprised if GME shareholders end up happy with the outcome.

Case study: MNPI? What MNPI? EKSO’s big PSUs

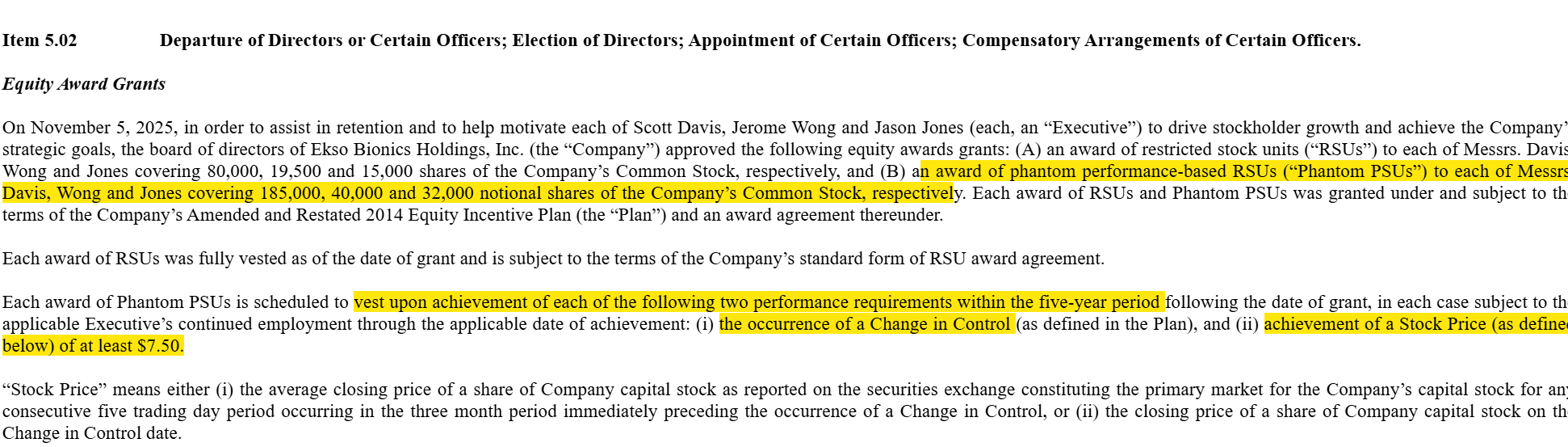

EKSO is a tiny little company; its market cap for most of last year was <$10m. But it’s a perfect case study in the dark arts and why paying attention to them can be profitable. In late November they gave all of their executives’ PSUs that vested only if the company underwent a change of control and the stock was “at least $7.50” per share within the next five years. The stock was trading in the mid-$4s at the time.

I’m not sure I’ve ever seen a single PSU grant that flashes “we are for sale” harder than that grant.

Sure enough, at the end of December EKSO announced a deal to merge with APLD’s cloud business spinoff. A few weeks later, EKSO did a private placement; it will shock you to learn the placement was priced at $8.22/share, above the mark that vested EKSO’s PSUs.

It wasn’t guaranteed that the market would respond positively to EKSO’s merger…. but I’d suggest EKSO’s board and management knew something was in the pipes when they made those grants, and that whatever was coming was likely to excite the market.

As I write this, EKSO is trading at $12/share.

Well played, EKSO.

Both EKSO and GME were post-mortem case studies. The next two are “live”.

VAC is buying their turnaround

VAC’s recent history has been rocky, to put it kindly.

John Geller became CEO of VAC January 1, 2023, and he didn’t exactly cover himself in glory during his tenure; the stock fell ~61%, dramatically trailing both the index and its key competitors:

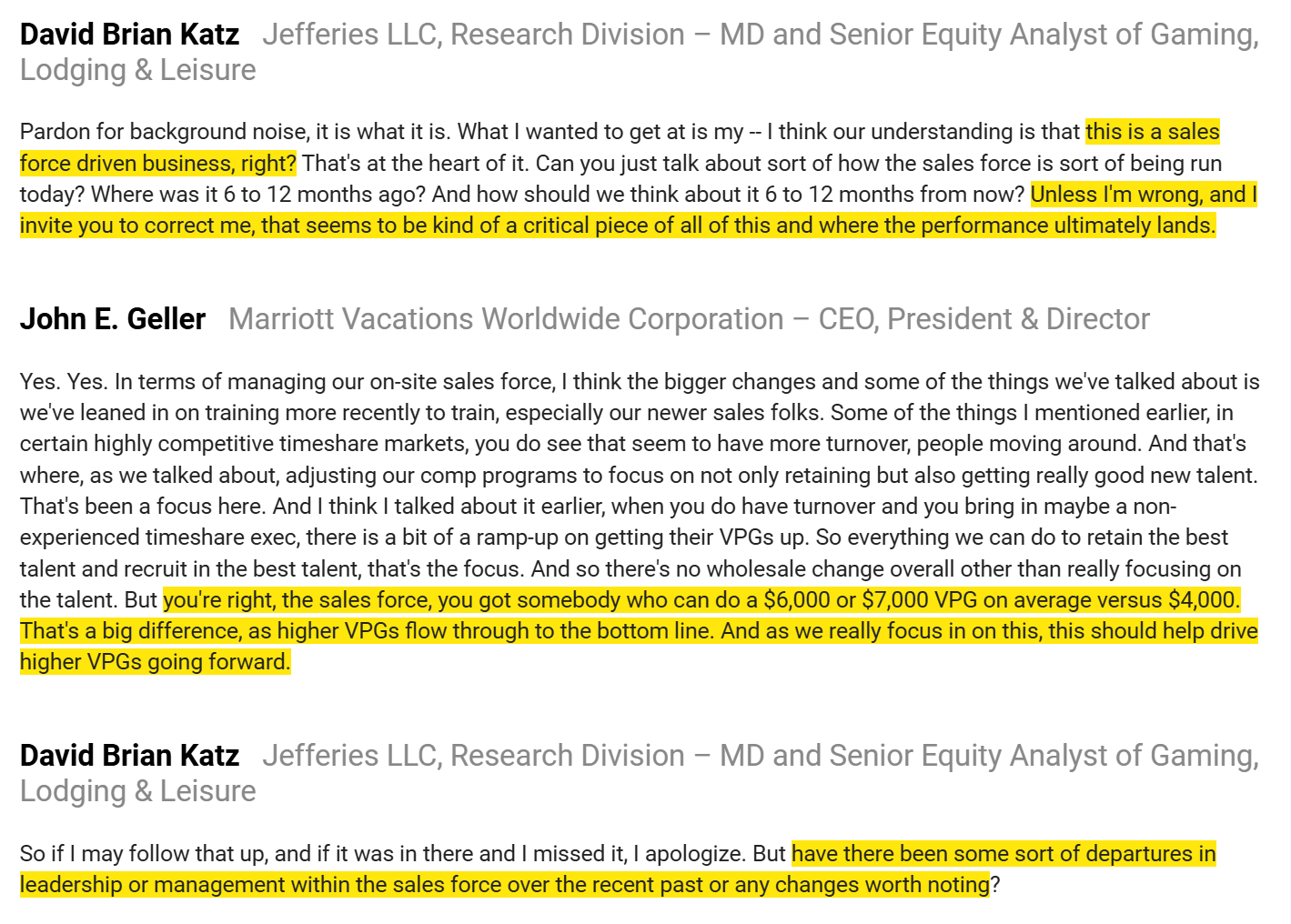

The breaking point came with VAC’s Q3’25 earnings, which saw the stock crash by ~33%…

…. and had analysts openly wondering if the sales force was stable, or if there had been management turnover there….

To put it bluntly: if things are so bad internally that the sell side is asking questions about sales force stabilization on your earnings call, then it’s basically a five alarm fire. The sell side never wants to ask questions that blunt.

Within a week of that earnings disaster, VAC had replaced their CEO with a board member serving as interim CEO. The interim CEO would get named permanent CEO in mid-February; alongside getting named CEO permanently, he brought on an industry vet he’d worked with to serve as President / COO (and heir apparent). And that’s where the dark arts come in….

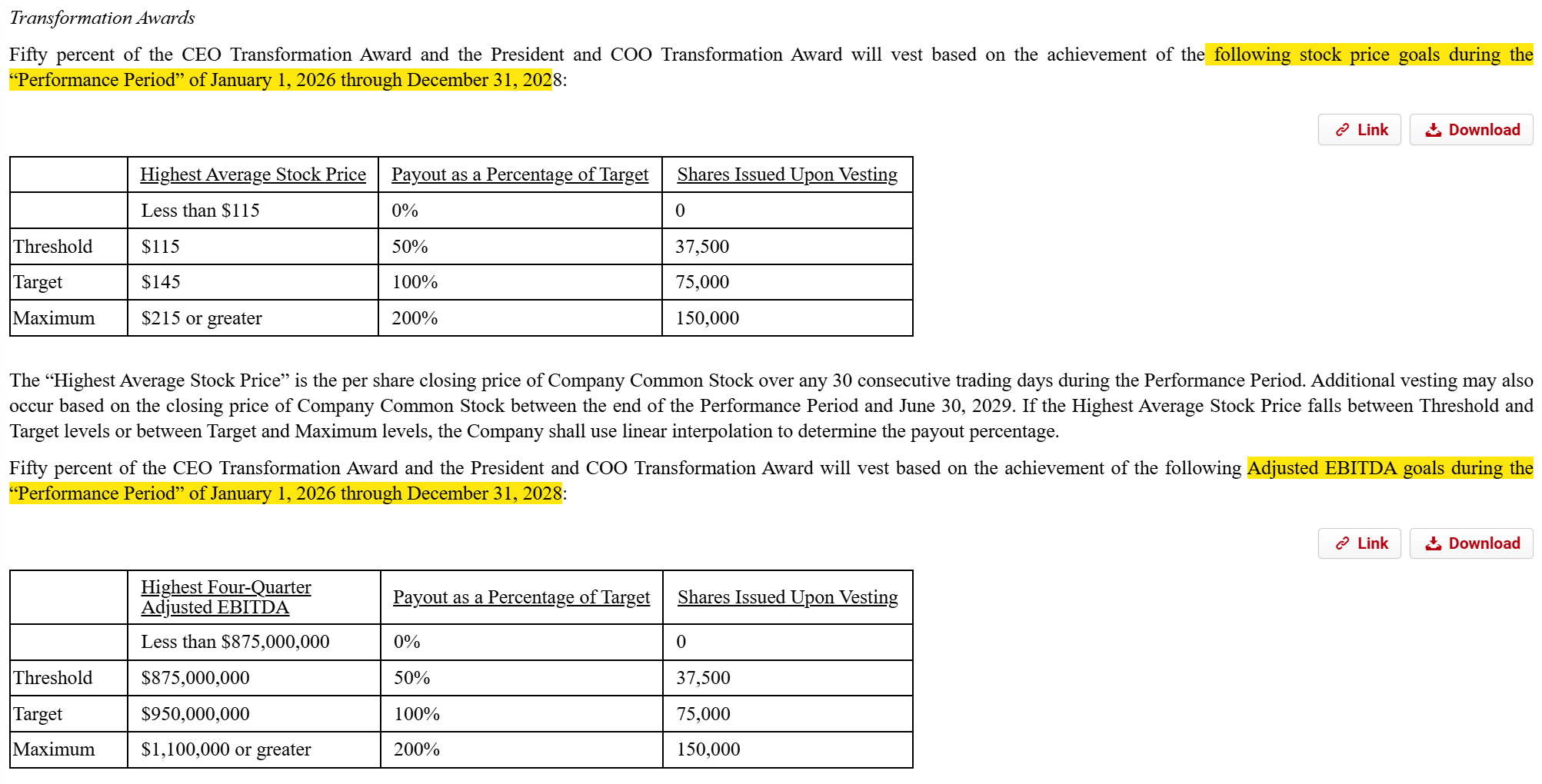

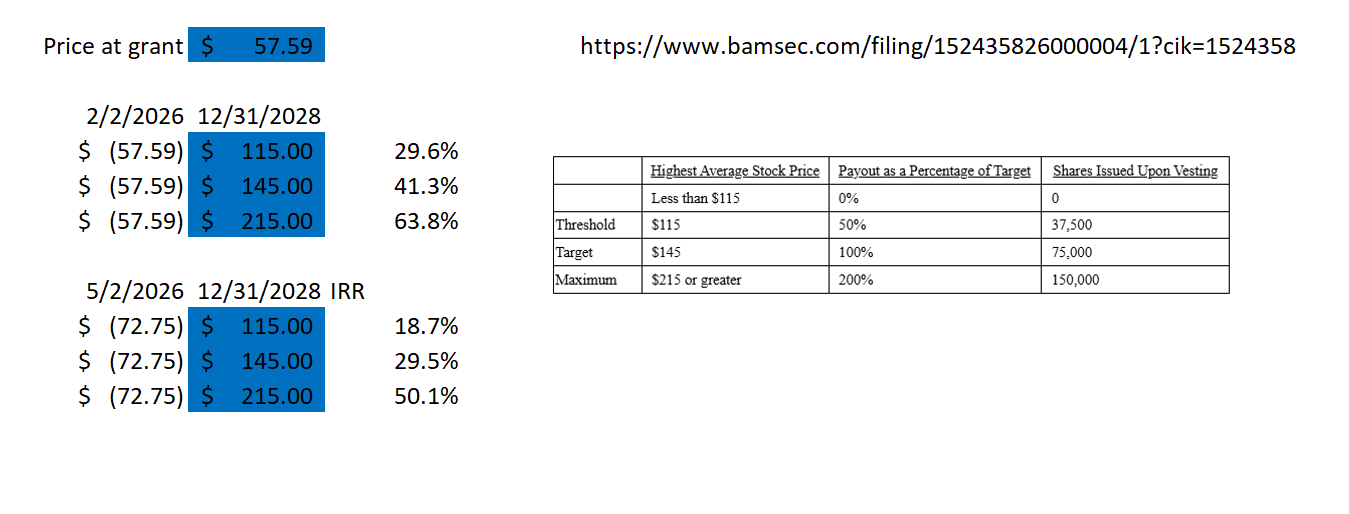

Both the new CEO and the new President took on a very stock / incentive heavy plan. The press release gives the high level: “This plan reinforces pay‑for‑performance, with two‑thirds of long‑term equity awards contingent on delivering $950 million in Adjusted EBITDA and achieving a $145 stock price over a three‑year horizon.” That statement makes the awards seem aggressive…. but I think they’re actually more aggressive when you see the real terms of the awards / look at just how torqued to the upside they are:

There are a lot of interesting things about those packages. One minor one: it’s interesting that the vest calls for the same payout for both the CEO and COO. Normally you’d have the CEO get a bigger package. Now, VAC probably set the CEO and COO PSU payouts at the same level because the COO is the heir apparent (his contract requires the company to promote him to CEO by the end of 2027 or else his whole contract vests), but it’s interesting nonetheless!

Still, the real headliner here is the comp package; it requires VAC stock to go up quite a bit on a tight timeline to vest. At the low end, the stock needs to hit $115/share by the end of 2028. VAC’s stock was <$60 in early Feb. when these grants were made; the stock would have needed to go up ~30%/year just to vest the low end. Even after a nice run over the past few months that has sent the stock to the low $70s, the stock still needs to do ~19%/year from now through the end of 2028 for the low end of the awards to vest. On the high end, the stock still needs to go up ~3x (implying a ~50%+ multi-year IRR).

The EBITDA targets are no less interesting. VAC is guiding to ~$765m in EBITDA in 2026; the low end of their payouts requires annual adjusted EBITDA to grow to $875m by the end of 2028 ($950m at target).

Put the EBITDA targets together with the stock price targets and the requirement for the CEO to hand the reins to the COO in a few years, and I think you can paint a pretty clear story: VAC was hopelessly mismanaged by its last CEO. A board member steps into the CEO role on an emergency basis after the disastrous earnings report in November, and a few months later he comes back and says “things are bad here…. but there’s a path to stabilizing and making this work in a few years.” The board gives him a big package to work for another year or two, gives him a clear successor who can help him manage the load, and heavily incentivizes both of them to hit targets that both they and the board think are reasonable, and that would make shareholders very happy if hit.

VAC is one live setup. Here's a second, and the only one in this post I have a position in:

RPD: SaaSpocalypse meets activism meets big incentives

Rapid7 (RPD) would like you to know that things are going great. Their Q4 earnings report noted “outperformance against fourth quarter ARR, revenue, and profitability guidance” driven by their “differentiated approach to AI security operations,” and they devoted a huge piece of their most recent earnings call to explaining why they “believe Rapid7 is on the right side” of the AI evolution and its impact on software and that AI might be helpful, as their “business is built on proprietary data that becomes more valuable as we scale AI capabilities.”

To say the market is not buying any of that is an understatement; the stock has been decimated over the past year:

That decline has been rough for Jana. Jana first filed a 13-D on RPD in September 2024 when the stock was in the $30s. Right after that filing, RPD fielded some buyout interest, but that appears to have fizzled (interestingly, Jana’s 13-D was initially filed with Cannae, who dropped out of the group to “engage in confidential discussions with the Issuer and other parties without restricting” Jana). While Jana did not get a quick buyout win, they did get a reasonably quick corporate governance victory: they leveraged their ~6% stake to get 3 new board members in March 2025. Since then, Jana has been a consistent buyer of RPD stock3; by mid-March 2026, Jana had almost doubled their stake to >10% while the stock has dropped by >80% in a rising market.

Here’s where things get interesting: in late March4, Jana entered into a nomination agreement with RPD. The previous agreement capped Jana’s ownership at 14.9% of the company; the new agreement lets Jana go up to 19.9% of the company. Almost immediately after signing the agreement, RPD gave their CEO and CFO chunky PSUs that “vest upon the Issuer’s Common Stock attaining specified stock price thresholds over a three-year performance period.”

Now, we don’t know what the share price targets for RPD are5… but we do know that we have a sophisticated activist who is way down on their position, has a bunch of people they nominated to the board, and just negotiated an agreement that allows them to buy ~10% more of the company and take their stake to 19.9%. Plus, immediately after signing that cooperation agreement, the company gave their two top execs chunky, share price driven grants.

I will be honest that I have no particularly strong view on RPD’s business; in fact, I think there’s a decent shot they are an AI loser. But I have a tracking position in RPD for the simple fact it checks three really interesting boxes:

Bombed out share price due to AI fears

Highly motivated and aligned board and incentivized management

Reasonable buyout interest historically (on top of the October 2024 approach, Rapid7 explored options in early 2023).

I have built a little research function in Claude that I use to get a brief overview when I’m looking at a stock; when I was using it to ramp on RPD it suggested “RPD is arguably the most ‘in-play’ name in mid-cap cybersecurity”

No guarantee that RPD works (nothing is ever guaranteed in investing, and to show my level of conviction I have just a tracking position here)…. but it’s hard not to feel like this is an asymmetric, positive EV bet with that setup.

Four stocks with four very different setups… but all with one thing in common: boards are incentivizing very specific outcomes, and management seems to be working towards giving them exactly what they are paying for.

Today’s post marks the 9th in the series. Previous posts include RELY + OPEN’s pay package, META’s YOLO options, incentives gone awry, an analysis of LION + STRZ new packages, five more dark arts ideas, dark arts clues $SOX was about to go parabolic, the ACHC case study + premium dark arts basket, and this premium write up on my favorite current dark arts set up.

Disclosure: long a tracking position

It’s also interesting the agreement came days after RPD did an acquisition of an “agentic AI security platform.” No terms were disclosed and there was no 8-K, so I assume this was a very small bolt on…. but still interesting timing!

Great post and very interesting substack overall. Please continue!

The EKSO case is a perfect illustration of why comp filings are worth reading cover to cover. Setting a vesting target 65% above the current stock price isn't aspirational. It signals someone in the boardroom knows something. RPD with Jana doubling their stake while the stock is down 80% is the one I'd be watching.