Not All Bullish CEO Pay Packages Are Equal: $OPEN vs. $RELY

Corporate dark arts, part 1

My friend Mike at Nongaap once said about the corporate dark arts, “once you see them, you’ll never stop seeing them.”

I’ve increasingly felt that way over the past year; with the market awash in volatility, I’ve seen more companies and insiders use aggressive, equity-heavy packages to capitalize on dislocated stock prices or clear inflections in value.

Today, I wanted to compare and contrast two specific examples of equity heavy packages that are clean, easy to understand, and very similar on the surface

OPEN’s package for their new CEO in September 2025

RELY’s package for their new CEO in February 2026

Why choose these two specific examples?

Because while any share price heavy package is interesting on its own, comparing these two shows how you can combine “the corporate dark arts” with fundamental work to separate real signals from noisy ones.

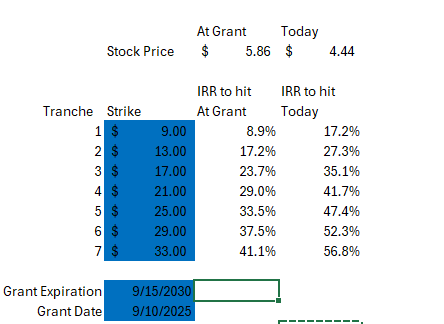

Let’s start with OPEN; in September, they hired Kaz Nejatian as their new CEO. To say Kaz is betting on OPEN stock is something of an understatement: the terms of his contract call for him to make $1/year and he is not eligible for annual bonuses.

Why would he take a package that paid him basically nothing? As part of the deal, Kaz received a bunch of performance stock units (PSUs) that vest if OPEN’s stock hits different price levels; I’ve included a table below that shows all the different levels and share vests:

That package has 7 tranches of PSUs and each tranche has just over 5.8m PSUs. At the high end, if OPEN’s stock can hold $33/share, the combined value of the tranches will be worth ~$1.4B (pre-tax). OPEN was trading for ~$5.85/share when the grants were made in early September 2025; to hit the low end of the package, the stock needed to do ~9% annualized. Again, that’s just to hit the low end of the package. The table below shows the annualized return for the stock to hit different tranches of the package at the time of the grant and at today’s share price:

On paper, this is about as good a CEO incentive package as you can get. The award is heavily tied to share price performance, which means management only really gets paid if shareholders do too. That kind of package is always worth noticing. If a board and CEO are willing to load compensation so heavily toward equity upside, it usually tells you they want maximum exposure to the stock price. And, as a little cherry on top, as part of the CEO appointment you had a new board member join and write a $5m check into OPEN alongside a respected VC fund (Khosla) writing a $35m check. That’s great alignment and a wonderful sign that sophisticated investors have bought into the vision / upside here.

Which begs the question: if the signaling and alignment at OPEN is about as good as it gets, why aren’t I personally that excited about the opportunity (read: why don’t I have a position)?

I’ll be honest: it’s because I hate the OPEN business. I just see no way it’s profitable through a whole cycle. I'll eat crow if and when proven wrong about the underlying viability of OPEN, and obviously the insiders here who are betting on the stock should be more knowledgeable than me… but I’ve always thought this business would be challenged for a host of reasons, and I don’t think any amount of management incentive can change that basic reality. I’m also a little turned off by how retail focused the company is; things like “special dividend of tradable warrants” seem designed to (try to) lure in retail shareholders and a massive distraction12.

So I think OPEN is so useful here because it helps show that “dark arts” style grants matter, but they are not sufficient on their own. You still have to marry the compensation analysis to your view of the fundamentals… and that is what makes RELY more interesting to me.

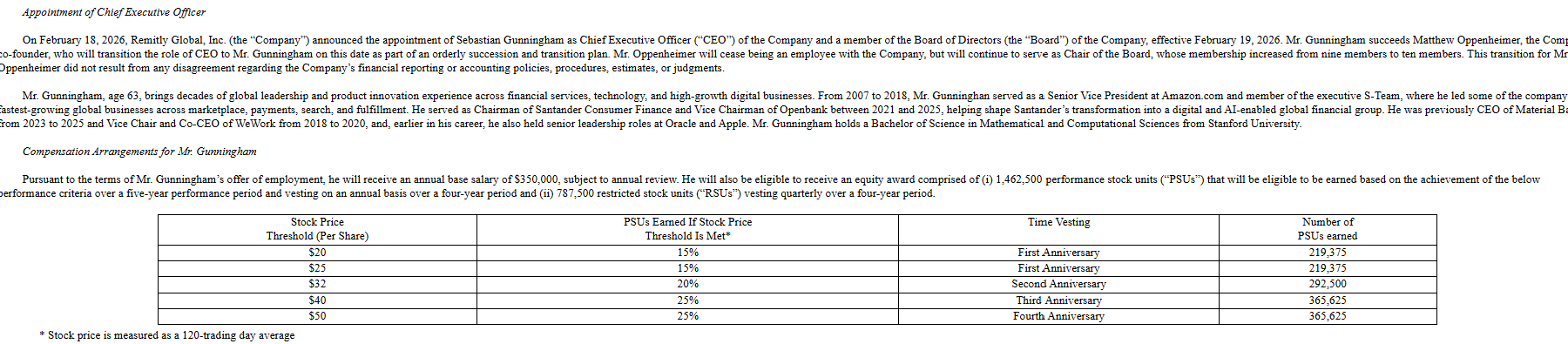

RELY is a company I’ve spent a lot of time looking at and thinking about (largely because I think highly of Mario Cibelli and he’s laid the story out so well on the podcast3); in February, they hired a new CEO and gave him a very interesting equity comp package:

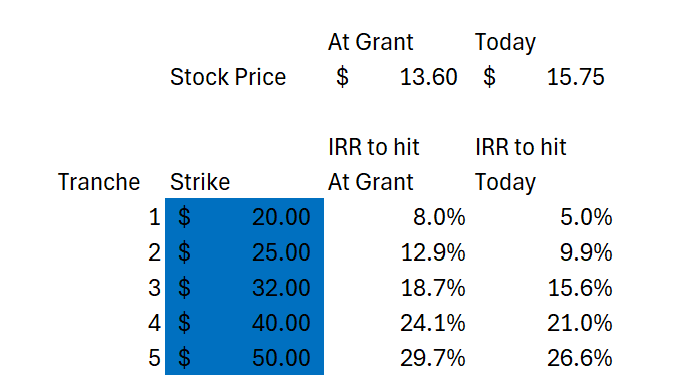

RELY’s stock was trading at ~$13.60/share when they gave the CEO that package in mid-February. Just to hit the low end of that grant, the stock had to do ~8% annualized from then until 2031. To hit the high end, the stock had to do almost 30% annualized. Here’s a quick table I put together with the IRRs to vest the different tranches:

All in, the RELY set up is very similar to OPEN. You’ve got a new CEO stepping in with minimal salary (RELY’s CEO will make $350k/year, a pittance for public CEO!) with an aggressive share price schedule that requires the stock to do pretty darn well just to hit the low end and will create generational wealth if the CEO can hit the high end and deliver incredible stock performance (the high end of $50/share would be worth ~$70m to the CEO). The plan isn’t quite as aggressive as OPEN’s plan (RELY’s CEO is taking home some salary and can get bonuses; OPEN’s gets nothing but the PSUs and becomes a billionaire versus a mere ~centi-millionaire if they hit the high hend), but it’s pretty damn torqued to the stock price (RELY’s CEO is also being given ~787k RSUs to go along with those PSUs; those are worth ~$10m at market price so he should be pretty darn equity motivated even ignoring the almost nine-figures he’s got on the line if he can get the stock to hit $50!).

So the set ups are similar…. but why am I a lot more positive on the RELY grant than the OPEN one? Here’s where I think you can bring in some fundamental analysis / critical thinking to these types of “dark arts” setups.

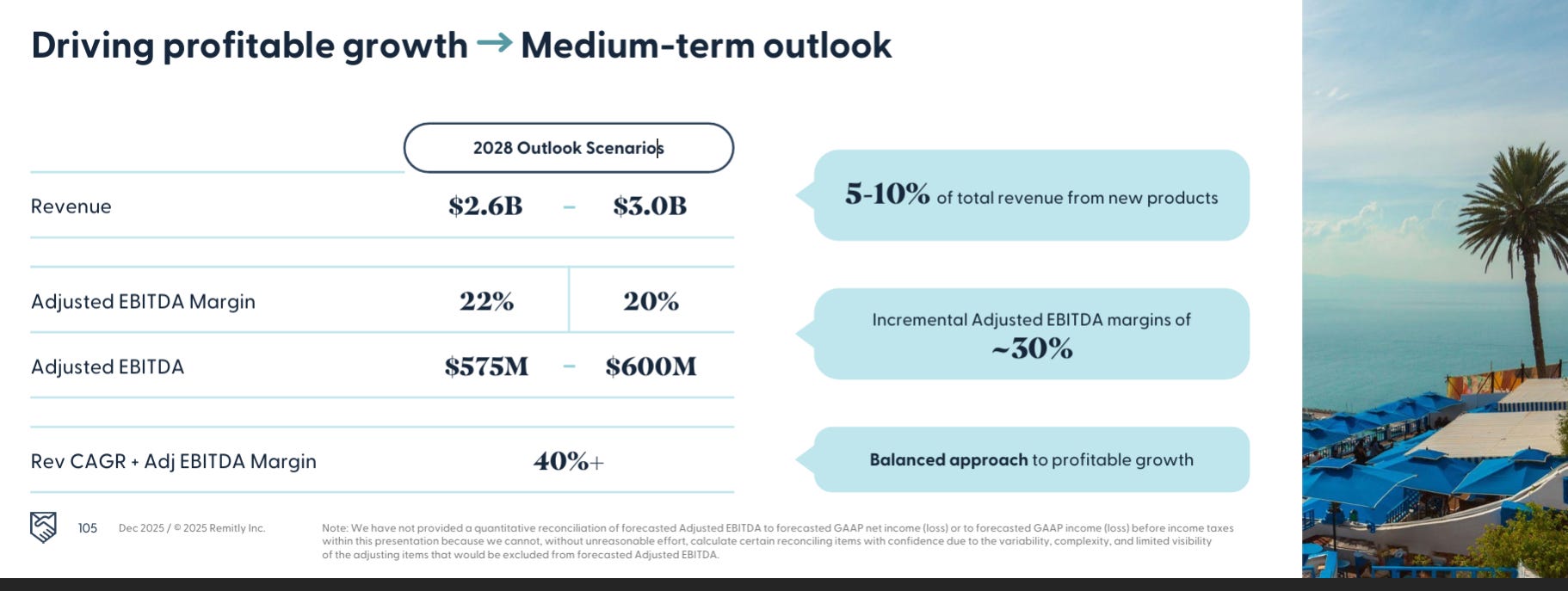

RELY just hosted an investor day in December. The investor day included a whole bunch of fundamental stuff on RELY’s business and outlook, including this “medium-term outlook.”

RELY is a net cash company that is currently doing ~$1.6B in revenue and <$300m in EBITDA. They’re talking about growing revenue 20%+ annualized and EBITDA basically doubling in three years. The CEO’s pay package explicitly notes “the stock price range implies an increase in the Company’s estimated market capitalization up to $10.5 billion.” That valuation is <20x the 2028 EBITDA guidance; it’s absolutely not crazy to think that RELY would trade for 20x+ EBITDA if they hit that outlook and are growing that quickly.

What makes RELY especially interesting is that the company put out firm guidance targets before it hired the CEO. That timing gives the new CEO a chance to “underwrite” the stock and the guidance: he could examine the assumptions behind those targets, ask questions about the path to hitting them, and decide whether taking a heavily equity-weighted package was worth the risk. That’s why I think RELY’s package carries more signal than the average heavy incentive grant: it suggests both the board and the incoming CEO believe the path to those investor day numbers is real.

Odds and ends

A true skeptic might think that companies are just throwing these PSUs around and treating them like funny money. I’m sure there’s a little bit of that with stock based compensation at publicly traded companies, but I believe that CEOs are going to put a lot of thought into taking a job that’s equity heavy and have reasonable confidence in an event path that will help them to hit those targets. Why? CEOs aren’t dumb when it comes to their pay package. No CEO is going to join a company and sign away five years of their life for an equity heavy package unless they feel there is a very good chance they can vest that equity. And no board wants to have a CEO join, do a great job, and then make no money because the equity package was struck at ridiculous numbers. That’s a recipe for an unhappy CEO who starts taking some weird risks or doing some weird stuff. So, at a high level, I’d contend that the CEO and board only approve these types of packages if they have a clear plan for how they get to their targets.

As long as I’m ranting on OPEN, a quick comment: they’ve added an accountability tab where you can keep track of their weekly metrics. It’s a cool idea…. but I think it’s just very showy / can easily encourage bad behavior. The core of the tab is tracking how many contracts they get every week; that is very gameable. You could increase your contract turnover instantly by just throwing out a ton of insane bids on houses! Real turnarounds and share price growth take work; I’m not sure diluting it down to one measure for external shareholders is all that productive (and it might be counter productive!).

My plan is to turn this post into a multi-part series over the next few weeks. Each part will break down an interesting “dark arts” style grant in a different way; if you enjoyed this post and want to see more of them, I have two requests:

My emails are always open for tips on interesting set ups like this; I try to track all the juicy exec comps, but the real interesting stuff happens when you can combine a juicy pay package with fundamental research and a thesis on what’s driving the bullishness.

It’s actually quite helpful if you hit the “like” button at the end of this article to let me know you like these types of posts / help the substack algo spread the word

I’ll also note that the big PSU package adjusts for dividends and distributions, so paying out a special warrant dividend of out of the money warrants could be a way to lower the vesting target of some of those PSUs…….

I’ll admit to finding the “every OPEN home comes with an American flag and flag pole” bit cringe as well

After I largely finished this post, Mario tweeted out a bit more on RELY’s set up and (likely) margin inflection. Worth a read!

LOVE the highlights on special comp packages and corp gov dark arts!

NNBR is my only pushback to CEOs being thoughtful about not signing away years of their life.