Corporate dark arts gone awry: how executive incentives can destroy shareholder value $NNBR $GME $HAIN

Corporate dark arts, part four

Probably the quote I think about the most is Charlie Munger’s quote on incentives,

Well, I think I’ve been in the top 5% of my age cohort all my life in understanding the power of incentives, and all my life I’ve underestimated it. And never a year passes but I get some surprise that pushes my limit a little farther.

I’ve written two articles around that quote (2023’s Trite Munger quotes that hit me, H1’23: Incentives rule all and 2025’s Weekend thoughts: incentives and bad corporate governance), and the “incentives rule all” is part of my fascination with the corporate “dark arts” and the driving force behind my recent posts on RELY + OPEN’s pay package and META’s YOLO options (as well as this premium write up on my favorite current dark arts set up).

However, sometimes incentives can go wrong. Today, I wanted to highlight a few examples where stock heavy packages might not be as bullish as they appear, where a comp package could actually disincentivize management from maximizing shareholder value, or (at the extreme) where a poorly designed package could encourage management to destroy shareholder value in order to maximize management’s payout.

Let’s start with the most fun example, and also the one I see the most:

A comp scheme that could encourage management to destroy value to maximize their own payout.

Gamestop (GME) serves as a perfect example here. In January, they gave their CEO a huge option package: the CEO got >171m options struck at $20.66/share (the stock’s closing price). The options don’t expire for 10 years, and they only vest if the company hits certain market cap and EBITDA targets. The company was really proud of this award and the alignment it encourages; they put out a PR touting it and everything!

You can certainly see the logic behind the award: GME’s market cap is <$10B, and their 2026 EBITDA was ~$345m. This comp package is encouraging massive market cap and EBITDA growth in order to even begin vesting.

Corporate governance ninjas can probably already see the issue with this package: it encourages any growth in market cap and EBITDA, not per share numbers. That incentive carries a host of issues. To take it to the most extreme: the CEO could easily hit all of his targets by issuing stock like a wild man in order to boost the company’s market cap. He could then take all of that cash and go on an acquisition spree in order to drive the company’s EBITDA up. It doesn’t matter whether the acquisitions create value for shareholders; if they boost EBITDA, they help from a vesting perspective. The EBITDA metric also encourages a certain type of acquisition: buying low multiple businesses is much better for the company than buying higher multiple businesses because a low multiple means each acquisition dollar creates more EBITDA and thus gets them closer to vesting the EBITDA hurdle. It doesn’t matter if the higher multiple business is a better one that would create more shareholder value; the CEO is not incentivized by shareholder value. He’s incentivized to increase market cap and EBITDA.

Or consider this: pretend Gamestop makes an incredible acquisition or investment. Say they take $5/share and put it into Bitcoin 2.0 at $100 and it goes to $1,000. GME now has an investment worth $50/share…. but let’s say GME’s stock stays stuck around $20/share, so it’s trading at a huge discount to this awesome investment in Bitcoin 2.0. The best thing GME could do in that case would be to buyback stock as aggressively as possible….. but doing so would significantly reduce GME’s market cap even though it would significantly increase GME’s per share value.

Now, there is a limit to how far this specific example can be gamed; GME’s CEO was given options, not PSUs, so he can’t just keep issuing equity at any price in order to hit the market cap requirement as he needs the stock to be above the strike for the options to have value…. but I think you can pretty clearly see the misalignment issues he’s going to face with this structure going forward.

And, by the way, this type of misalignment is not rare; I’ll see PSUs granted all the time with market cap or particularly EBITDA or free cash flow requirements. Let me show you one of the more dangerous ones I’ve seen recently: Dollar General’s (DG) walkaway package with their CEO.

Some background: in March, DG appointed a new CEO who would take the helm in January 2027. They gave their current CEO a transition agreement to encourage him to stick with the company through the end of the year. It includes a PSU package that vests 50% based on 2026’s EBITDA and 50% based on ROIC from 2026-2028.

Why is that package so dangerous? DG is a retailer. There are really easy ways to boost near term EBITDA; for example, both marketing expenses and IT investments are expensed in the current quarter but should have benefits down the line. If you’re a CEO who’s leaving at the end of the year, won’t you pull every lever to make sure you hit your EBITDA targets and get paid this year? If it leaves the company at a deficit in the long term…. well, that’s the next guy’s problem! That’s the type of incentive that results in a CEO cutting costs to the bone and leaving the next guy to clean up a mess.

Let’s move on the next example; I’ll admit, as an investor, this one scars me the most:

A comp package could actually disincentivize management from maximizing shareholder value.

Why does this one scare me? Because I’m so focused on incentives, and I’m always worried I’ll be lured into a situation where the incentives look positive but are actually insidious.

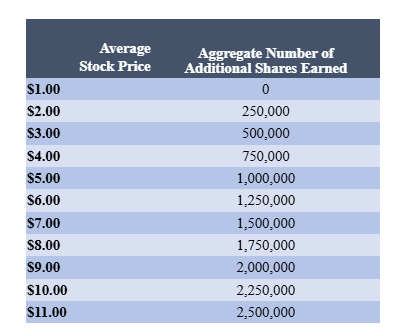

A live example will show this best: consider NNBR. In 2023, the stock was trading for just over $1/share, and they recruited a new CEO with a contract that would give him up to 2.5m shares if the stock price could hold $11/share:

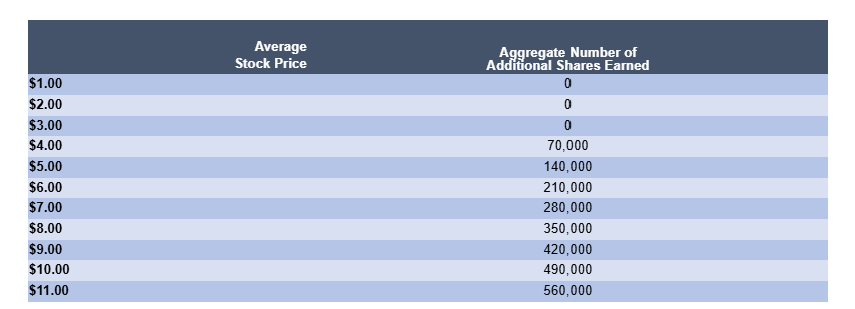

It’s not just the CEO who could get pretty wealthy if the stock screams higher; the COO took a similar package:

Fast forward to today, and things haven’t gone that well. The stock is back down to $1.50/share (though some early strength in the stock resulted in the $2 and $3 tranches vesting), and the company is reviewing strategic alternatives. Imagine you’re the CEO and had two choices right now: sell the whole company for $3/share, or max out the company’s credit line, head to Vegas, plop down at a roulette table, and bet it all on lucky #13.

If we ignored the fact that option #2 would result in some jail time, the CEO is actually incentivized to pursue that “lever up and risk it all” option. Why? Selling the company doesn’t help him vest more units, so he’s not super incentivized to pursue a sale (particularly because it puts him out of a job). In contrast, if he got lucky with the “lever up and risk it all” strategy all those PSUs would go in the money and he’d grab a multi-million dollar windfall.

Obviously that’s a very extreme example, but it contains an interesting nugget: when a CEO has a bunch of deep out of the money grants or options, they become increasingly incentivized to take high variance bets with the company, even if those bets are hugely suboptimal for the company and negative expected value for its shareholders. Who knows how the NNBR review plays out, and there are some big shareholders that can hopefully help steer the ship there….. but it seems clear to me that a lot of the legacy incentives there are pushing strongly to a “one more YOLO” even if selling the company might make more sense for everyone except a handful of insiders….

Alright, let’s move on to the last example:

Stock heavy packages that might not be as bullish as they appear at first blush.

I find these often happen in companies that are in distress; the company will give a key executive a super equity heavy package. If you don’t look into it, it’s easy to mistake that package for a bullish sign…. but what it actually is is the company handing out lottery tickets. They’re not actually expressing a fundamental view of the company; they know they’re screwed and they’re writing massive lottery tickets in case something wild happens.

Again, an example will highlight this nicely. Consider HAIN; in December, they promoted their interim CEO to full time. As part of that promotion, they gave her a big PSU grant upfront and explicitly stated that the big grant represented three years’ worth of grants (i.e. she would not get any grants in FY27 or FY28). HAIN’s stock was trading for just over $1/share, and the grants required the stock to get to $3-9/share within three years. At the high end, this package was worth ~$13.5m in PSUs if the stock could 5-10x inside of three years.

A CEO giving up three years of awards to take them all up front and bet on a turnaround? That’s about as bullish a signal as you can get on the surface!

But there is another way to look at that grant: what if the company is facing distress, so the CEO and board decide they might as well front load all of the grants because there’s a decent chance the company won’t be around in the ensuing years to hand out bonuses anyway?

I’d suggest there’s a decent chance that’s what’s happening at HAIN. Just two months after being appointed full time CEO, HAIN sold their better for you business for $115m in cash. While the company suggested the business hadn’t earned anything in the past twelve months, the business was historically a strong earner; a subsequent filing suggested that the business had earned ~$30M in EBIT in the twelve months ending June 2025. So HAIN sold the business for <4x a very recent EBIT number; on top of that, their financials discloses they’ll incur $7.7m in transaction fees for the sale, and a subsequent earnings call revealed ~$25m in stranded costs they’ll have to whittle away with the division sold.

Obviously I’ve been unimpressed by these results…. but it’s not just me; the market has actually traded the stock down on the news. It’s pretty rare for an overlevered company to sell a division that’s not generating any profits and see the stock go down!

It’s impossible to know the whole story from the outside… but it’s really hard to look at those numbers (plus the resulting share price!) and think anything other than “HAIN is really stressed and forced to firesale assets to try to deal with their leverage.” I’d suggest that sale was in the works when the CEO switched from interim to fulltime and that YOLO PSU package was negotiated. My guess is everyone looked around and said, “we’re screwed; no one else will take this role and step into this mess. On the off chance we survive this, here’s some generational wealth to make it worth your while.”

Odds and ends

Pay can obviously get funky in other ways. Someone highlighted COOK’s pay to me recently, and I’d be remiss if I didn’t mention it. COOK’s financial performance for 2025 missed all of their executive team’s performance goals, resulting in their stock declining >50% during the year and “no payments under the program to the Company’s named executive officers”…. but “the Board decided to award Jeremy Andrus, the Company’s Chief Executive Officer, and Michael Joseph (Joey) Hord, the Company’s Chief Financial Officer, discretionary cash bonuses equal to $956,250 and $270,938, respectively, due to their significant contributions to the Company in 2025 and to promote retention.” Well done guys; if I was a shareholder I know I’d be thrilled with that decision!

LCID hired a new CEO this month and gave them market cap hurdle PSUs; again, just not sure why any board would go for market cap weighted over per share. Just creates lots of opportunities for misalignment for no reason.

One more example of PSU grants that could cause problems: PLAY gave their new CEO PSUs that vest based on SSS growth and adjusted EBITDA targets. You could think of a worse way to incentivize a CEO, but this one is pretty bad. Why? It’s near impossible for a restaurant to report negative adjusted EBITDA, so you just handed the CEO a comp package that said “go open a ton of units no matter the return on investment and you will get paid. And, if you do it quickly, those units enter the comp base while still in the honeymoon period, thus helping you hit your SSS target!” Combine them, and the CEO is incentivized to rush to open a ton of units. Yikes.

I don’t know a single person who has been to or bought anything from Game stop…I feel like this company is in the same category as Long John Silvers.

The market cap vs per share distinction is the one most comp committees get wrong on purpose. Per share alignment kills the acquisition spree narrative the CEO brought to the table, so it loses in the room. The HAIN lottery ticket read is sharp. Boards front load grants when they have already privately priced the enterprise for distress. The COOK line is the one shareholders should keep on a card. Formula missed, pay delivered anyway. That is a vote of no confidence from the comp committee in their own design.