What $META’s YOLO options package says about its AI upside

Corporate dark arts, part 2

Meta just handed its top executives one of the most aggressive options packages I’ve seen in years. What makes it remarkable is what management appears willing to underwrite in setting the option price targets: an upside case where Meta’s stock rises more than 6x in five years, pushing its market cap toward $10 trillion. I don’t think any company makes an equity grant like this lightly, but for a company as analytical as META to give out option targets this aggressive suggests they see some fundamental path to hit those targets… and, given fundamental upside that large would need to be driven by META’s AI business, those targets suggest META is partly underwriting1 an AI outcome far more optimistic than even most bulls assume.

Note that I’m not the only one to notice META’s interesting options package; it’s the example people emailed me about the most over the past week on the heels of the RELY / OPEN piece. But, even with all the eyeballs that come with META being a trillion dollar company and every corporate dark arts guru picking up on these crazy out-of-the-money options, I still don’t think people realize how insanely bullish the options grant is nor do I think people appreciate what it implies about the upside META sees in its business (and, given that the upside is probably being driven by META’s AI efforts, by extension I don’t think people realize how big META is saying they think the upside to AI is).

Let me give a juicy sound bite to let you know just how damn bullish these options are: as an investor, I generally just don’t buy mega-cap companies. Too many eyeballs, too much competition…. but despite that, META’s options are so insanely bullish that I’m tempted to buy some LEAPs on META just to avoid the FOMO of missing out on the clear upside they’re showing if it actually plays out2.

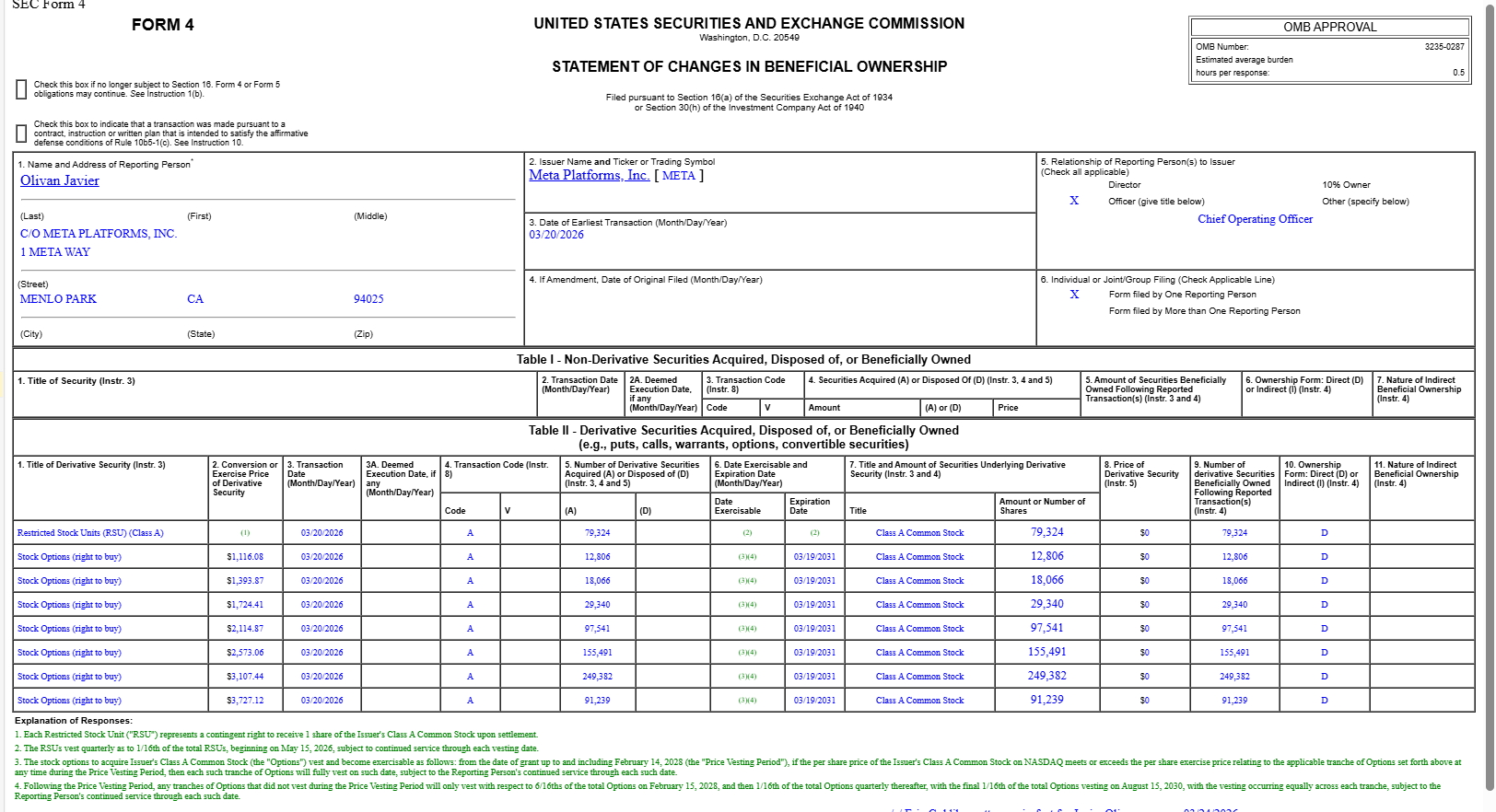

Alright, tease out the way, let’s actually dive into the options. In late March, META gave basically all of their C-Suite (except for Zuck) multi-year stock options that require the stock to almost double before they’re even in the money (for example, the bottom end of the options package is struck at >$1,100/share versus a current trading price of ~$600/share!).

The company was even clear3 with the press that this package was all about the executives aggressively betting on themselves and value creation. It’s worth clipping the statement from the company on the options in full, because it’s more akin to how a meme stock tries to rile up their shareholders than a trillion dollar company talking about rewarding / incentivizing their employees:

This is a big bet. These pay packages will not be realized unless Meta achieves massive future success, benefiting all of our shareholders. As with all stock options, there is only value if the share price meaningfully exceeds the exercise price, and in this case, it must be on an exceedingly aggressive 5-year timeline

META’s “big bet” is interesting for a host of reasons. Let me start with a non-obvious interesting thing: Zuck is already plenty rich, and he famously takes a salary of $1/year with no bonuses (though META does drop >$25m/year on hiring security for him and his family); instead of getting big bonuses and salary, Zuck just benefits from his 300m+ shares of stock increasing in value, so he still gets plenty rich / upside exposure if the stock works…. but it’s still extraordinarily rare to see a bunch of top execs get some “if this stock goes parabolic, you’ll make multi-generational wealth” options and have the CEO excluded. It’s really interesting to compare Zuck’s “take nothing” approach with Elon’s “give me huge upside at every turn” approach. Both seem to be working for them (though it is kind of funny that Elon’s 2018 options package at Tesla is now worth ~Zuck’s entire stake in Facebook is worth; if Zuck was demanding huge package every few years at Facebook, what would he be worth today?).

So the CEO incentive angle is interesting…. but the most interesting thing to think about here is what it implies the team thinks about the fundamental upside if META “wins” or succeeds over the next few years. In fact, I don’t think people understand just how big or how bullish META is suggesting the upside at the company is.

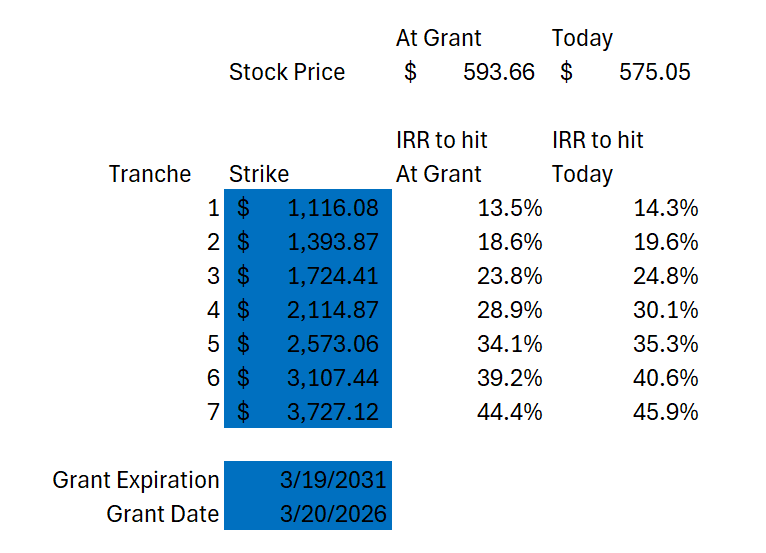

Let me start with a quick table: the table below shows the different strikes that META gave their executives and the IRR required to get to those strikes before the options expire:

It doesn’t take a financial wizard to look at those IRR numbers and think, “dang, that’s bullish”…. but it’s even more bullish than you think. Why? Remember that these are options, not grants, so META’s stock needs to really work for these to have value. An option struck at $1,116/share is worth $1 if the stock closes at $1,117 the day the option expires; in contrast, a PSU that vests if the stock is trading at $1,116/share would be worth $1,117/share if that’s where the stock closes that same day.

This package would already be aggressive if it were structured as PSUs… but the fact it’s done in options suggests that META thinks they have the potential to go on some insane run that sends the stock into the stratosphere and makes these options really worth something.

Now let’s tie that bullishness into what META is saying about the potential for their business. META has ~2.5B shares outstanding. The highest end option is struck at $3,727/share (and, again, the stock needs to be much, much higher for those to be worth anything); at that price, the stock would have ~6x’d in five years and META’s market cap would be over $9 trillion.

Will the stock do that well? Probably not; the base rate of a trillion dollar company 6x’ing in five years is…. well, it’s zero, as it’s never been done before! But if you believe in corporate dark arts, then grants and options are handed out with at least some eye to them being achievable / valuable. For Meta to hand out options like these suggests insiders see at least some plausible path to a ~$10 trillion valuation on a surprisingly short timeline. What does that tell you about how they’re thinking about the AI event path and how they can monetize it? What are the odds they have an internal financial roadmap backed by the early returns from their AI investments that suggests these options have some chance of paying off big?

PS- Completely unrelated, but my friends at AlphaSense are hosting a webinar on using AI for earnings prep and analysis. It’s an area I’ve been spending a lot of time on recently and will likely have some upcoming posts on, so figured I’d highlight if of interest! You can sign up for the webinar here:

And maybe seeing internal metrics supporting that future underwriting?

Not investing advice, options are insanely risky, see the legal disclaimer here, etc.

“This is a big bet. These pay packages will not be realized unless Meta achieves massive future success, benefiting all of our shareholders. As with all stock options, there is only value if the share price meaningfully exceeds the exercise price, and in this case, it must be on an exceedingly aggressive 5-year timeline”

Hey Andrew, Fantastic piece! It felt like you were reading my mind regarding the insane bullishness of Meta’s recent options package.

I completely agree that for a company like Meta to hand out out-of-the-money options where the floor is $1,116 signals massive internal conviction. However, I do want to offer a gentle pushback on your thought that the stock multiplying to hit these targets is "probably not" going to happen due to the base rate of trillion-dollar companies…

In my latest piece, ""Back to the EBITDA: Decoding Meta’s $1,116 Executive Playbook", I reverse-engineered the math needed to hit that $1,116 floor target by the board's Feb-2028 accelerator date. When you break down the income statement, that lower tranche is actually very achievable.

Assuming a standard 25x multiple, Meta needs to generate roughly $111 billion to $115 billion in net income to justify the $1,116 share price.

To do that while keeping their ~42% operating margins intact, they need about $315 billion in revenue. This implies an optimistic, but very doable, ~25% annualized revenue growth.

The market is panicking over CapEx, but they don't have to sacrifice margins to fund the AI buildout. By trimming the fat—specifically cutting Reality Labs' burn down to a $5 billion to $6 billion baseline and executing a 20% workforce reduction (or more)—they offset the massive data center depreciation hits with hard cash operating savings.

If hitting $1,116 just requires baseline operational discipline and pulling the right margin levers, the upper-end strikes get incredibly interesting. In my next article, I'll actually be sharing the math on what the income statement needs to look like to push the stock into the $2,000 and $3,000 per share range.

Keep up the great writing! Best, Simeon

Deep dive here: https://www.accruedint.com/p/back-to-the-ebitda-decoding-metas

Maybe a much smaller organic IRR layered atop 10% annual inflation rate?