Corporate dark arts: one case study and three premium setups

Corporate dark arts, part 6

Today is part 6 in my “corporate dark arts”, and this post will be a little different than the prior five parts1. I’ve got two completely different sections for you:

A case study: A question I’ve frequently gotten since I started this “corporate dark arts” series: who cares? All management teams are greedy; does seeing management get a little greedier really have any signal value? My answer is (obviously) yes. But don’t take my word for it; let me present ACHC as a great example of why it can pay to pay attention to executive compensation signals!

Building the premium dark arts basket: I’ve already written up my favorite dark arts setup on the premium side, but there are three more stocks that I think are worth tossing into a “dark arts basket”. One combines a botched dark arts attempt with a heavy event angle, one is a “hero or zero” (the stock could easily 10x or be a zero), and one has a management team suddenly giving out stock price linked packages to the whole C-Suite while the environment underneath seemingly inflects for the better.

Let’s dive in:

ACHC case study: these things can play out fast

In January, ACHC hired Debbie Osteen back as CEO. Debbie had been CEO of ACHC from December 2018 to March 2022, during which time ACHC had outperformed both the indices and some loose peers2:

Things at ACHC have fallen apart without her; the stock has collapsed and drastically underperformed peers:

ACHC has a lot of Medicare and Medicaid exposure; healthcare businesses with big government exposure are often subject to reimbursement changes outside of their control. So it’s probably not fair to lay all of ACHC’s drastic underperformance on her successor…. but stocks rarely collapse ~80% over <4 years without quite a few strategic and operational missteps.

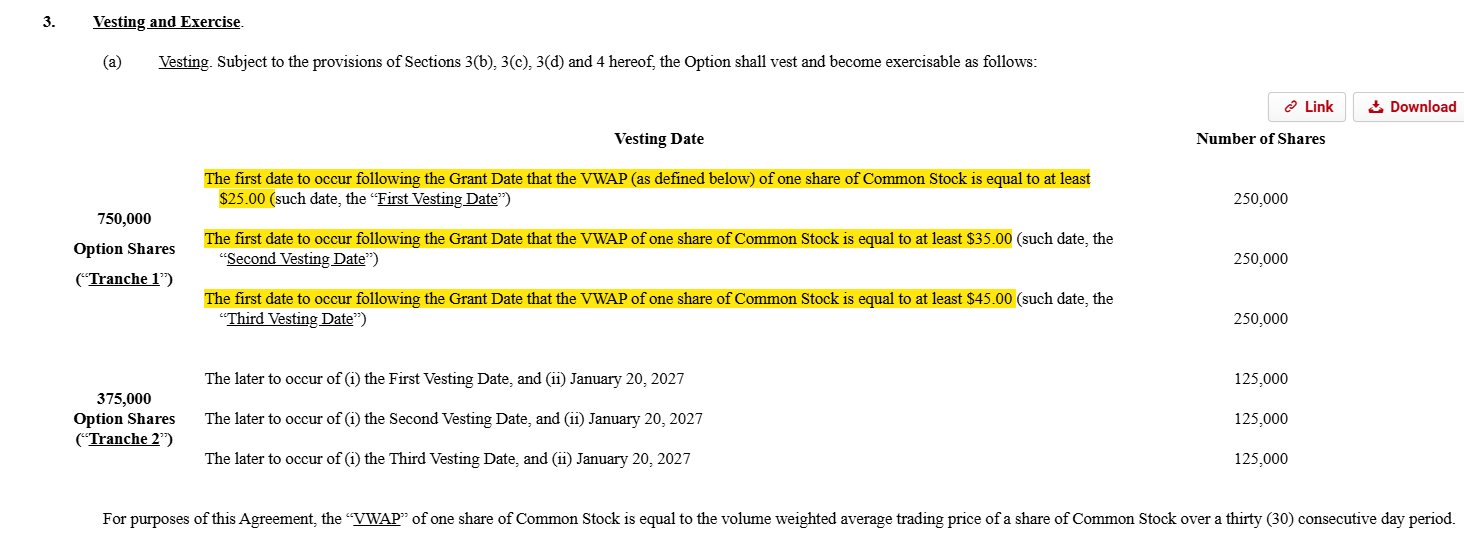

Given those operational issues, investors were rightly excited when Debbie stepped back into the CEO seat. I mean, investors were really excited to have her: the stock was up >20% on the news she was coming back. And the board was eager to have her back too; they gave her >1.1m options that vested at different prices.

Those options were struck at $11.68/share, which is where ACHC was trading before Debbie came back. Obviously, that’s an aggressive options package; yes, they’re 10 year options, so Debbie has a lot of time, but the stock needed to more than double just to vest the first tranche… but with an aggressive options package comes significant upside. ACHC was trading ~$70/share when Debbie left in early 2022; if Debbie could get the stock back to that level, this package would be worth ~$70m. Debbie makes ~$1m/year in salary with a target bonus of ~$1.3m, so I don’t think it’s a stretch to say that this options package will leave her very stock price motivated.

You can probably guess what happened next. In February (~a month after Debbie took the CEO job back), ACHC reported results that beat guidance. More importantly, 2026 guidance was much better than expected; I saw sellside notes with quotes like “we believe Debbie has drawn the line in the sand with this guidance, which is way above buy-side expectations” and “beat on EBITDA in 4Q and formal 2026 guidance that we believe came in comfortably above both bull and bear expectations.”

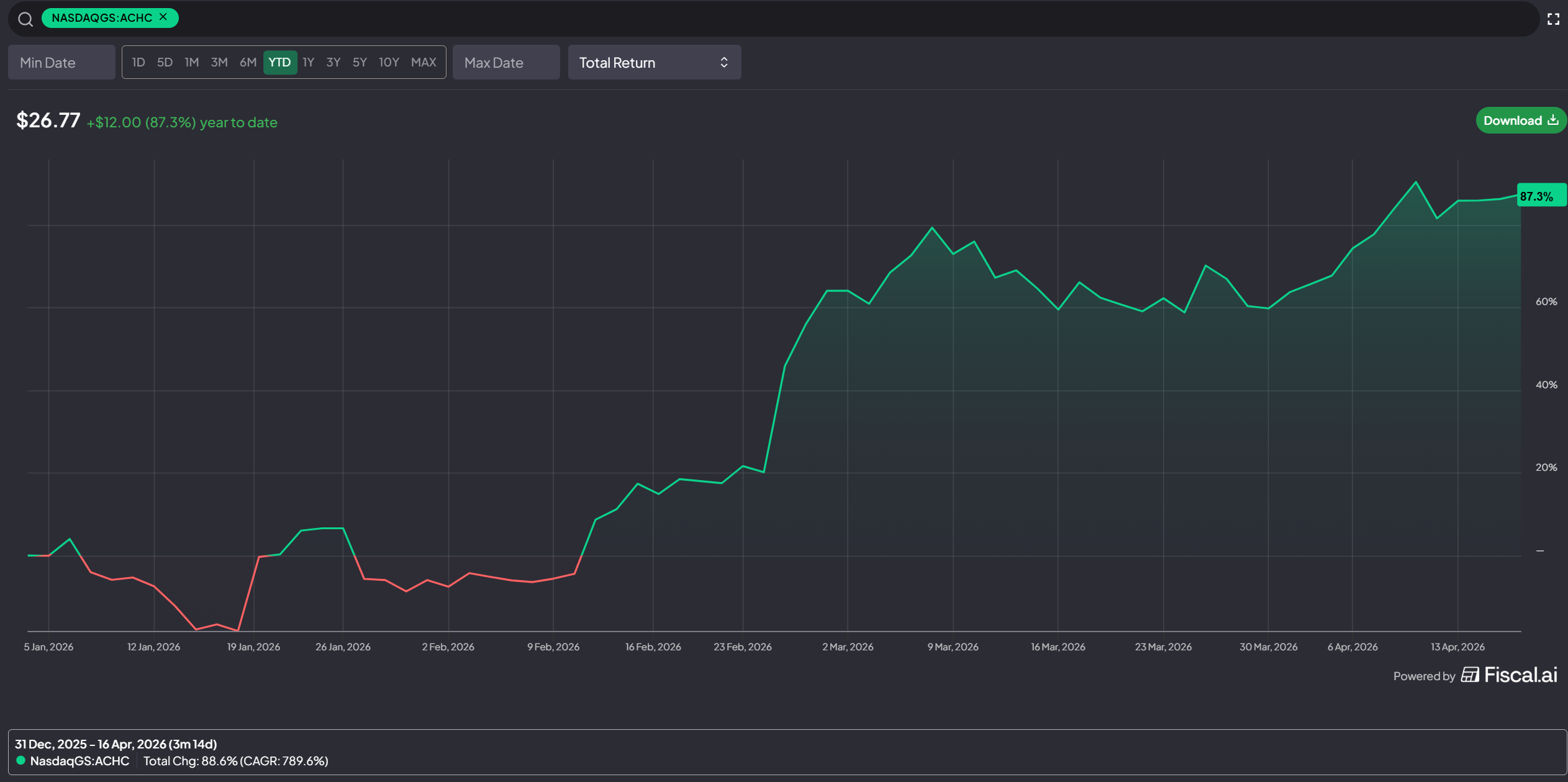

The stock has been a rocket ship since. It’s almost doubled on the year, and it seems like the first tranche of Debbie’s options will vest imminently:

I’d call ACHC about as perfect a case study in the dark arts as you can get. Debbie took the CEO role in late January. The board and investors were thrilled to have her, and she and the board negotiated a massive comp package that called for the stock to hit $25 on the low end.

Does that mean the stock was guaranteed to hit $25? Absolutely not! But I would wager quite a bit of money that Debbie and the board both had a very good idea what the 2026 guidance was going to be and how the stock market was likely to value the company on the heels of that guidance, and they priced the options with that reaction in mind.

ACHC is a clean example of why these setups are worth tracking: boards do not hand out aggressive packages like these by accident, and when the signal is real, it can matter fast. This series has already covered several interesting dark arts setups, but there are three current examples worth a deeper dive as part of a “dark arts” basket: one event-driven, one distressed, and one with both turnaround and M&A optionality.

Keep reading with a 7-day free trial

Subscribe to Yet Another Value Blog to keep reading this post and get 7 days of free access to the full post archives.