A hopeless $LION and some dim $STRZ dabble in the corporate dark arts

Corporate dark arts, part five

This month, YAVB has been fully focused on the corporate dark arts, with three public posts (OPEN vs RELY, META’s YOLO options, and incentives gone awry) and one premium post (i.e. behind paywall) covering a particularly unique situation.

Today, I want to highlight two companies intertwined at the hip that might be practicing the corporate dark arts: Lionsgate and Starz. The interesting thing here isn’t just that the companies have a hilarious history of shooting themselves in the foot (though they definitely have that)…. what’s interesting is that both companies suddenly started giving their CEOs incentive packages with aggressive stock price hurdles. Aggressive stock hurdles on their own are interesting, but they matter a lot more when a company suddenly adopts them after years of not using them. The question is always why does a company decide to make a switch to aggressive stock price comp? In this case, I think the signal relates to M&A: after over a decade of teasing a sale, LION may finally be serious about selling itself, while STRZ as a standalone might see a path to acquiring their way to growth.

But, before we get to that shift in comp, let’s start with some brief corporate history.

Brief corporate history

Perhaps no company has bungled the media landscape more over the past decade than Lionsgate / Starz; they’ve shown an almost uncanny ability to choose the wrong path at basically every turn. The original sin was the 2016 merger that brought the two together; in 2016, Lionsgate bought Starz for ~$4.4B. The deal almost instantly proved a poor fit as the media landscape shifted against them, but management compounded the mistake by repeatedly overplaying its hand when chances to sell emerged. The headliner here would be 2017, when Hasbro offered “more than $40/share” for Lionsgate and Lionsgate rejected it as too cheap(the stock would trade <$30 within months). Then Lionsgate had the chance to snatch victory from the jaws of defeat and sell Starz to CBS for $5B in 2019. They passed (demanding $5.5B); to show you how disastrous that decision was, STRZ is currently a standalone publicly traded company with an enterprise value under $1B.

Alright, let’s fast forward to today. In late 2023, Lionsgate merged a piece of their studio business with a SPAC. That merger was the first step in a plan to fully separate Lionsgate studios from Starz; they would conclude the plan with a full split in mid-2025.

LION has been pretty clear since they first started talking about splitting studio and STRZ up: the studio side deserved a premium multiple and was a valuable strategic asset, and by separating it out from a rapidly declining (and low multiple!) STRZ business both sides increased strategic optionality (LION likely to explore a sale or at least serve as a neutral “arms dealer” to the streamers; STRZ to pursue M&A and gain scale in some form).

LION post spin

Since the spin, LION’s management has been clear: they are open to a sale. For example, here’s a fun quote from a recent conference: “we're very cognizant of those values and the ability to create outsized valuation for our shareholders in the world of consolidation. So I think the library just becomes more scarce than ever.” And that quote is far from the only quote I could show you; their Vice Chair (Michael Burns) went on CNBC in the middle of the WBD bidding war to talk about how in demand their studio business was and how big the synergies would be if a variety of strategic bidders combined with them! And there are rumors that Legendary has been looking at LION for most of the past year.

However, I will be honest: as a longtime follower of the industry, LION saying that they’d be an attractive target and are considering selling themselves has a “boy who cried wolf” feel. They’ve been saying the same thing for years; for example, in early 2018, Michael Burns went on CNBC and said LION is a “pint-sized bite for some of these giant market cap companies” and therefore would “talk to anybody at any time” about a merger; does that quote sound at all like the quote he gave CNBC in the WBD bidding war last December?

So I’ve generally been pretty dismissive of the rumors that LION is looking to sell; I’ve been BURNed (pun on Michael Burns last name extremely intentional) way too many times to believe something is happening here.

Which makes this 8-k filing updating and extending their CEO’s contract so interesting. It makes me think this time might actually be different and that the company really might sell themselves this time. There are two things in particular worth calling out from the filing.

First, the CEO’s old deal ran through July 2029, and this deal extends him two more years. July 2029 is a long way away; it’s not like LION needed to extend him right now. Curious.

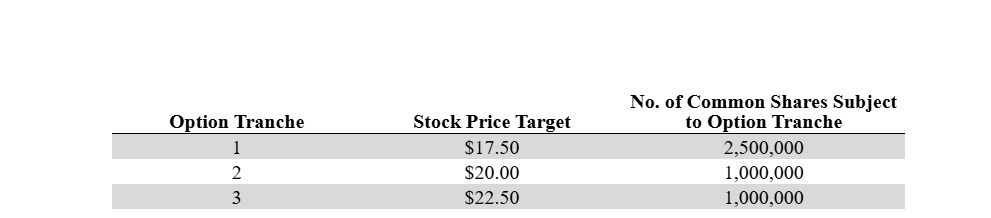

Second, the big kahuna: the agreement gives him a mix of options and PSUs that vest in five years and require the stock to hit prices much higher than the current stock price (~$11/share as I write this).

Any package that requires the stock to go up substantially is interesting… but two things stand out to me about this package.

First, I’ve looked at a lot of these types of packages. It’s exceedingly rare to have the lowest tranche ($17.50 in this case) trigger significantly more options / shares to vest than the higher tranches. In general, companies have each tranche vest a similar number of shares, or they have the higher tranches vest even more shares (paying more for significant share appreciation). I can’t remember a package where the lowest tranche vests so much more than the higher tranche.

Second, Jon has been CEO of Lionsgate since 2000. I went through the six contracts and extensions he’s signed since 20131; this contract is the only one that has any type of share price incentive or target in it. That’s quite the signal; it’s really strange for a company to change its comp practices like this, and companies generally do so for a reason!

Combine those two, and that’s why I think the M&A rumors are real this time. Jon has been CEO for 25+ years. He’s in his mid-70s. He just got a pay package that has share price targets in it for the first time. I’d suggest that this deal serves as a sweetener for him to sell the company, and that he and the board are pretty confident the company goes for $17.50+ in a deal and that’s why the majority of the payment sits there, with the two higher packages there to give him extra juice if the bidding gets really frothy.

So that covers the studio side… but the STRZ side is perhaps just as interesting.

STRZ post spin

Let’s be clear: the STRZ business is challenged. It’s a completely subscale premium channel without a studio. There’s not really a reason for it to exist anymore; it really needs to sell or merge with something.

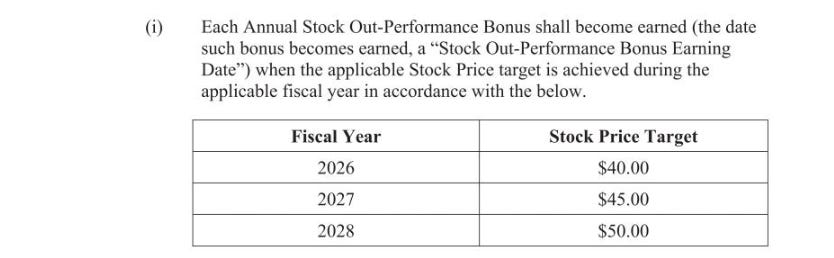

But that doesn’t mean it’s not interesting. Like LION, STRZ just gave their CEO a contract extension that, for the first time, had share price targets to vest. And those targets are aggressive and fast; the first tranche requires the stock to hit $40/share in 2026 (an almost four bagger inside of fifteen months from signing!) and the final tranche calls for the stock to hit $50/share in 2028.

That is a fascinating comp scheme. I’d also note that STRZ is optically very cheap. The company has a market cap of <$300m and has ~$600m in debt for a ~$900m EV. They did $200m in OIBDA in 2025, so they’re trading for maybe 4.5x trailing OIBDA and they’re guiding to ~$100m in unlevered free cash flow in 2026. A $40/share stock price would put their trailing OIBDA multiple around 6.5x and their unlevered free cash flow multiple at ~12x. Not crazy!

You could imagine a world where STRZ tries to hit those comp targets by buying back stock as fast as possible at these low multiples, but it seems they’re going to go the other way and become an acquirer. Here’s their Q4 earnings call:

That “we can acquire profitably angle” becomes even more interesting when you think about the timing of STRZ grant: November 2025. That grant comes right before Comcast completed the Versant spin-off and in the middle of the WBD bidding process. While STRZ business is challenged, it would likely have some synergies with a lot of legacy media assets. Perhaps STRZ looked at all of the pending merger activity and thought “hey, we’re going to have the potential for some very accretive M&A in the near term; we need to get our CEO a package that incentivizes him to get creative”?

One last interesting angle at STRZ: in mid-March, Byron Allen bought Steve Mnuchin’s 10%+ stake in STRZ in mid-March. Allen’s a media mogul who has been floated to a variety of media assets (Tegna, Paramount, and several others… though most of his offers have failed). Perhaps he wants to merge STRZ with his other media assets, or maybe he wants to use STRZ as a piece in a larger consolidation play…

Conclusion

Here’s what I hope you’ve taken away from this piece: over the past decade, Lionsgate has made the wrong move at basically every turn.

But this time might actually be different. On the heels of the WBD / PSKY / NFLX bidding war, the demand for studio assets seems insatiable, and there simply aren’t many standalone studios out there. Lionsgate has said for years that their assets are strategically valuable, but they’ve never seemed willing to pull the trigger. The CEO’s new contract suggests they’re getting ready to make him whole / incentivize him in a sale, and it’s the first time they’ve ever really prepped him for that.

On the other side of the coin, STRZ is in a tough spot… but it’s really cheap, and the CEO is highly incentivized to make it work. It’s not a perfect set up, but the upside is enormous if he can pull it off.

Like many investors, I’ve been BURNed (pun again intentional) over and over by Lionsgate. But the incentives here are really screaming that this time is actually different2.

Prior contracts and extensions: 2013 Employment Agreement — SEC, 2016 Amendment — SEC, 2020 Employment Agreement — SEC, 2022 Amendment — SEC, 2024 Employment Agreement — SEC

One other different worth noting: Lionsgate was controlled by MHR through supervoting stock until recently; post spin, they are no longer a controlled company, and Steve Mnuchin’s Liberty Capital has ~the same size position as MHR. MHR has a history of wanting perhaps unrealistic premiums to sell their assets; the combo of a large new shareholder and lack of control might help in making this time different.

Thanks for connecting the dots on this Andrew!

Love this. Management is finally incentivized with shareholders $LION