Corporate dark arts: one bizarre case study, one false signal, and three setups to watch

Corporate dark arts, part 7

Today’s post continues my corporate dark arts series: cases where executive comp, buybacks, and corporate actions hint at how management really sees a stock’s value1. The headline case today is FRMM, where management granted themselves aggressive upside exposure and then almost immediately rolled out a series of value-unlocking announcements. After that case, I contrast it with one example that looks flashy but probably means very little, then run through three other strange setups.

FRMM: a dark arts case study in strangeness

CAG: when “aggressive” PSUs mean almost nothing

GTM: aggressive buyback or value-destructive YOLO?

MMED: are the PSUs telling us anything about the post-IPO path?

SKLZ’s big Christmas present

Let’s dive in:

FRMM: a dark arts case study in strangeness

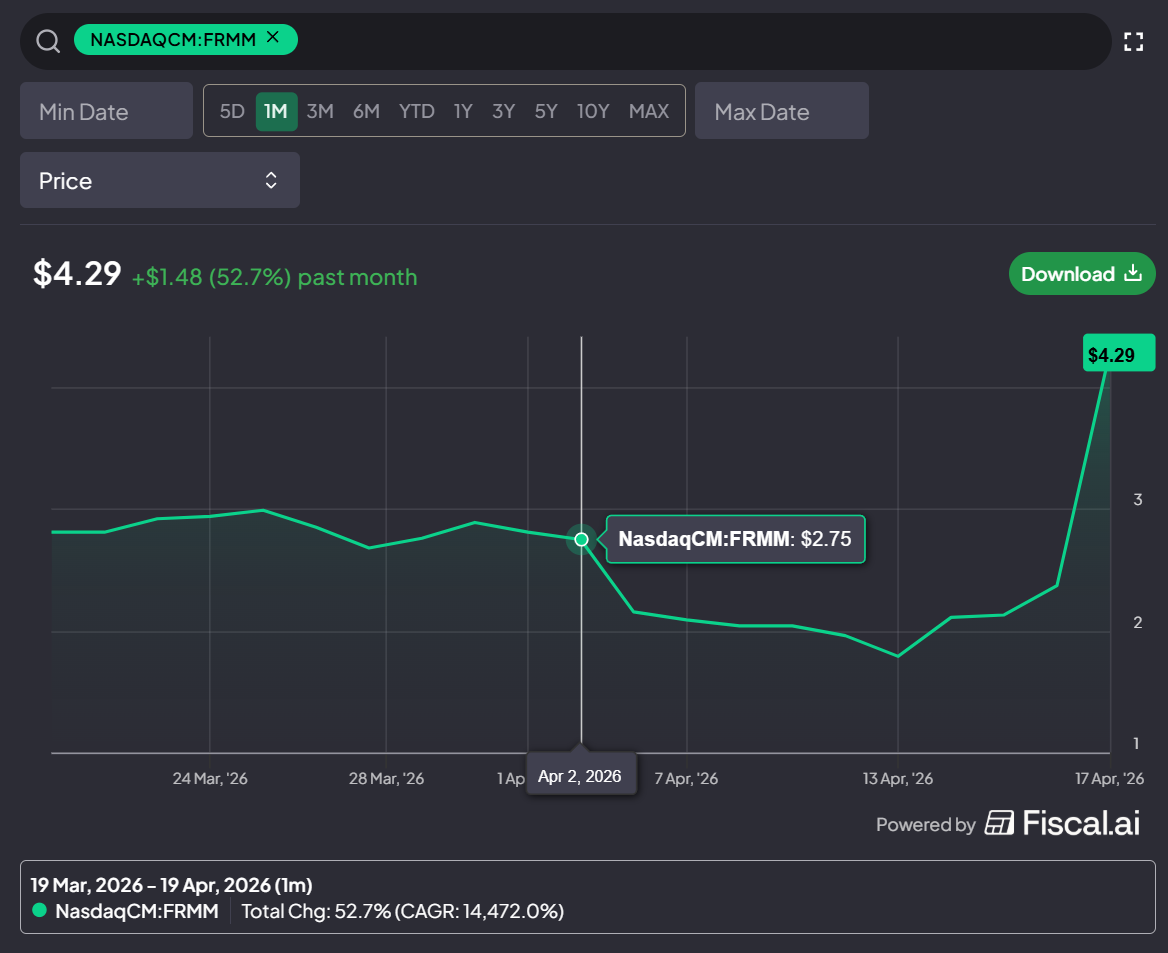

FRMM’s board and SEC filing team had a busy day on April 3.

That alone is a strange statement. April 3 was Good Friday, meaning it was a stock market holiday, but the SEC remained open because it was not a federal holiday. In my experience, companies try to jam in 8-Ks with news that they don’t want investors to notice on days when the SEC is open and the market is closed, so the fact that FRMM filed an 8-k alongside seven form 4s should raise eyebrows.

What did FRMM file? Well, they did four things:

They gave all of their directors big stock grants. Each director was given >200k RSUs; with FRMM’s stock trading for ~$2.75/share, that was a nice little $550k windfall for each director. Not bad for working on a Friday!

They gave their CEO a “one-time initial equity award and a pro-rated 2025 annual award” and their CFO an equity award. These awards mirrored each other and consisted of 60% PSUs with share price targets and 40% RSUs.

The stock price targets for these awards were reasonably aggressive. A third vest at $5/share, a third at $7.50, and a third at $10/share. FRMM’s stock was ~$2.75/share when the awards were granted and they expire in five years, so the stock would need to do reasonably well even to vest at the low end.

They halted their ATM equity agreement (ok, this 8-k was filed April 8, but given the timeline I don’t think it’s crazy to say the board and management made the decision to halt on April 3!).

They approved an investment into “AI Chip Infrastructure Financing to Purchase NVIDIA GPUs” that was targeting “Returns in the Mid-Teens”

Again, this announcement was made April 8; given the timeline, I don’t think it’s crazy to think it was approved April 3!

They followed those moves with a big announcement on April 17: the initiation of a share repurchase program and the establishment of a special committee to unlock value. The special committee would “examine the full range of value-maximizing pathways”, including mergers (and here the PR reveals that people have approached the company about a merger2) and a liquidation of the company.

The market liked FRMM’s actions; just two weeks into their five years PSU package, the CEO and CFO are almost in the money on the low end of their vesting targets, and the board is already up ~50% on their RSUs.

In many ways, FRMM is a classic “dark arts” case study (perhaps even more so than my prior case study of ACHC). FRMM management and board granted themselves big equity upside exposure and then went through a series of announcements designed to boost the stock price and maximize shareholder value.

But I think FRMM’s corporate background actually makes the pivot even more interesting. FRMM was one of the original Ethereum DATs; in July 2025, what was then 180 Life Sciences raised a ton of money to become ETHZ (they’d eventually rebrand as FRMM; we’ll get there). As the shine came off the DAT business model, ETHZ has shifted wildly on what to do with the huge slug of capital they raised and how to generate shareholder value. In just the past six months, they have:

October 23: Announced a strategic partnership with Liquidity.io, including a $15m equity investment.

October 27: sold $40m of ETH to facilitate stock repurchases at a “significant discount to NAV”

December 3: spent $10m for a 20% stake in Karus to “Power AI-Modeled Auto Loan Tokenization”

December 10: took a 15% stake in Zippy for ~$20m to “Tokenize Manufactured Home Loans On-Chain”

They also “streamlined” their capital structure by paying down $516m in converts

February 5: “Purchases Manufactured Home Loan Portfolio, Plans Tokenization on Ethereum L2”. ETHZ buys ~$5m of manufactured loans in the transaction.

February 12: spends ~$12m to buy jet engines and then “Announces First Ever Tradable Tokenized Aviation Assets on Ethereum Network Secured by Jet Engines on Lease with a Leading U.S. Air Carrier”

February 25: rebrands from ETHZ to FRMM to reflect “Next Step of Strategic Evolution Toward Institutional-Grade Real-World Asset Tokenization”

March 9: finances a $10m warehouse to establish an “Auto Loan Warehouse Facility Enabling 24/7/365 Loan Settlement via Blockchain Infrastructure”

March 31: FRMM reports Q4 results; notes they’ve sold the “vast majority” of ETH holdings and their current cash position is >$100m. On their earnings call, CEO estimates NAV at “$175 million-$185 million today, with 20.3 million shares outstanding.”

That’s a lot of asset activity; the reason I highlight it is because FRMM’s market cap is under $100m even after the pop from the strategic alts announcement. The CEO is describing their NAV as ~$180m, and within that NAV there are a lot of ~$10m VC style investments into blockchain businesses. Curiously, that $180m NAV number would imply $9/share in value…. just below where the high end of the CEO’s stock priced link PSUs vest.

FRMM’s move from <$3/share to approaching $5/share on the strategic alts announcement was basically the market giving them credit for their cash balance…. but there’s not much value built in that price for FRMM’s other investments. Perhaps the market is right…. but there’s no one better positioned to know their value than the board and CEO, and he and the board agreed to a share price linked package that implies a decent bit of value from those investments.

FRMM is a great reminder that stock grants do not just signal undervaluation. They can also align incentives for management to take the actions needed to unlock that value.

CAG: when “aggressive” PSUs mean almost nothing

I’ve detailed a lot of different examples of dark arts in this series. I think it might be natural to think “oh, we should just follow every company that gives stock price based incentives and buy a basket of them.”

Do I think that’s the worst idea in the world? No, I could think of plenty of worse investing strategies! But I also doubt a strategy like that is going to generate any alpha. It’s just too broad. To me, you want to use the corporate dark arts to identify a management team and board that are taking an outsized, unusual swing on the stock and then marry that swing with your own view of a fundamental inflection or investment thesis on the business.

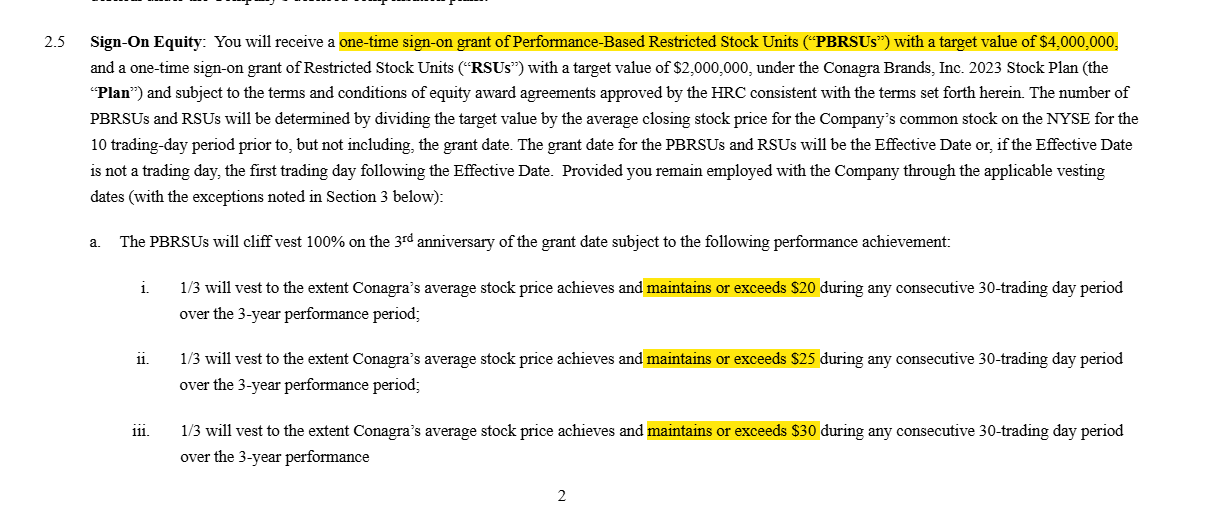

So let’s do a mini-case study of a meaningless signal. The type that I try not to highlight in this series (or invest in!). CAG just announced a new CEO; as part of his pay package, he was given $4m of stock price based PSUs that require the stock to hit $20-30/share within three years to vest.

CAG’s stock is currently trading for ~$14/share, so those are decently aggressive IRR targets. ~12.5%/year on the low end; ~29%/year on the high end. And $4m is no small amount of money!

But CAG is paying their CEO a $1.15m salary, a target annual bonus of 150% of his salary, and an “an annual equity grant value target of $7.3 million”; all together, he’ll be taking in >$10m/year as CAG’s CEO. I’m sure, all else equal, he would like the stock to go higher and all of those options to vest; every CEO wants their stock higher all else equal! But I’d also argue that CAG’s CEO is much, much more likely to be motivated by job preservation and his annual salary / bonus than he is by those PSUs.

Contrast CAG’s package to something like the RELY package I mentioned in the first part of this series. There, the new CEO is making $350k/year in salary and, as far as I can tell, no annual bonus. Instead, his whole motivation is an aggressive series of PSUs that would be worth $70m+ if he can get the stock price up. That’s a grant that screams alignment / everyone thinks they can get this stock up!

GTM: aggressive buyback or value-destructive YOLO?

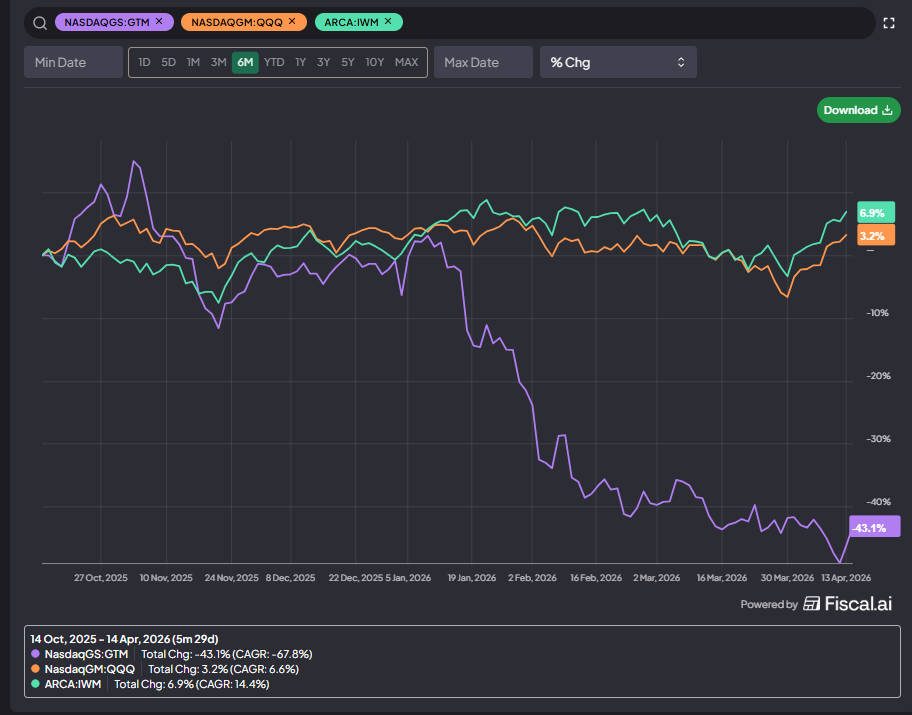

GTM is interesting because it presents the dark arts bull case and the dark arts bear case at the same time: management has a wildly upside torqued comp package and the company is embarking on a massive share repurchase program…. but the AI fears are very real and the market clearly thinks this is a structurally broken business. So are the massive buybacks management’s way of showing the AI fears are overblown, or does the comp package incentivize them to throw good money after bad and buyback stock even if the business is melting away?

Let’s back up. In late November, GTM gave their CEO one of the most upside-torqued pay packages I’ve ever seen. Mojo had an (excellent) post detailing the package and the (likely) behind the scenes activism that led to it (and the post is well worth reading), but the key points of the package are that the CEO was granted a ton of options that required the stock to, at minimum, >4x in 10 years to start vesting….

Obviously, that’s an aggressive package, but the rewards were fantastic if the CEO could hit them: the package would be worth ~$400m if the high end of the options vested.

So, as of late November, GTM and their CEO should be fully aligned with driving towards massive and explosive shareholder value creation. That alignment came just in time for the SaaSpocalypse, and GTM’s stock has been slaughtered:

GTM’s response to their share price has been interesting. You’ll see a lot of SaaS companies say “we’re unique; AI won’t hit us”…. but then they’ll do nothing as their share price dwindles to nothing. GTM is not sitting still as their stock melts; in 2025, they repurchased ~12% of their stock for ~$10.06/share. With the stock getting smashed, they believe they “have been presented with a generational opportunity to create value” and got “Board authorization to repurchase more than 50% of the company's outstanding shares.” They also noted their “commitment to using the majority of the cash we generate to repurchase ZoomInfo shares for as long as that is the best and highest return use of our free cash flow and at these price levels.”

That all sounds incredible…. but I will admit to wondering if the company is accurately seeing the playing field. The way most investors blow up is doubling down on a stock again and again as it heads to zero. Why should it be any different for companies? If they thought the stock was a great buy at $10/share, and now it’s at $5/share, do they have a great grasp of the fundamental value and outlook? Or is it possible buying back stock is actually negative expected value for shareholders but positive expected value for insiders because buying back stock aggressively makes it easier for them to vest / hit those aggressive share price targets if the company can pull the proverbial rabbit out of its hat?

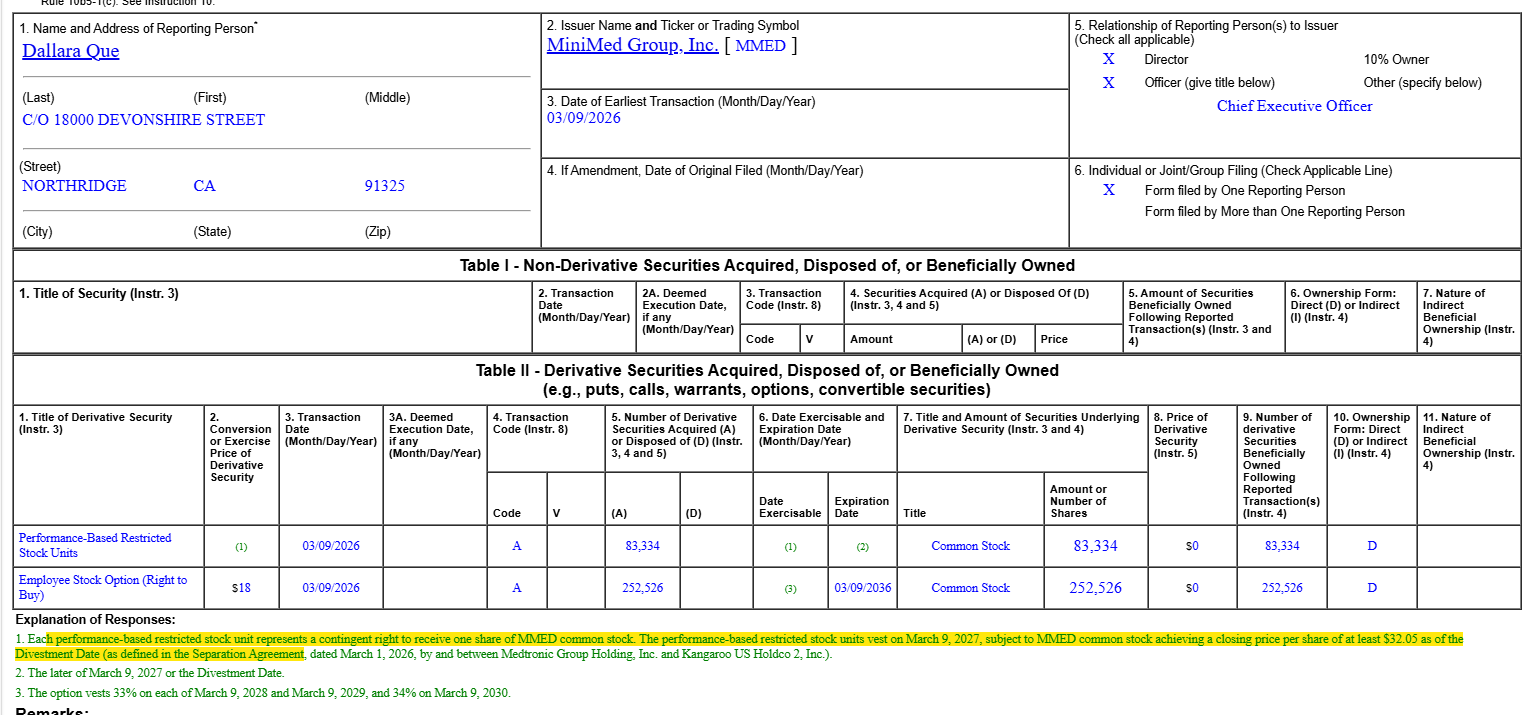

MMED: are the PSUs telling us anything about the post-IPO path?

MMED is a recent IPO from Medtronic (MDT); they IPO’d in early March at $20/share, and Medtronic continues to own ~90% of them. It was “the second biggest MedTech IPO in history”, and MDT has been clear that they will eventually exit their full position (likely through an exchange offer3).

What makes MMED interesting is that, alongside the IPO, basically every key executive (CEO, CFO, GC, etc.) was given PSUs that vest if MMED stock hits $32.05 by the later of March 2027 or when MDT disposes of their MMED stock.

Again, MDT has already said that they plan on exiting MMED in ~6 months, so it’s probably safe to assume that the “later” will be March 2027. MMED IPO’d at $20 and is currently trading in the mid-teens; for those PSUs to vest, management is going to need the stock price to more than double in less than a year.

Perhaps they’ll never get to that price…. but MMED got FDA approval for their next gen insulin pump soon after the IPO, and I have to imagine that management and MDT at least saw some fundamental path to hitting that stock price target if they gave every high level employee a package that called for it. And I’d note that given MMED’s very small float while MDT still owns 90%+ of the stock, you could imagine that a few of the levers MMED could pull could cause the stock to overshoot on the upside.

There are a lot of companies that incentivize through stock price, but it’s pretty rare for a company with a thin float and a major controlling shareholder intent on disposing their shares to have such an aggressive stock price incentive. It’s a potentially explosive combo; will be fascinating to watch.

SKLZ’s big Christmas present

2025 was a rough year for SKLZ.

The main issue was accounting related. They were unable to get their 10-K filed on time in March, and the accounting issues cascaded from there. They didn’t get their 10-K filed until November, and then they couldn’t file their Qs until mid-December. To add insult to injury, on December 18th SKLZ filed an 8-k noting they’d hired a new CFO who would start in January…. but on December 23 the new CFO “withdrew his acceptance of the Chief Financial Officer position.”

Not great, Bob.

On top of the messy accounting / finance functions, operational performance wasn’t exactly great either; while revenue grew a bit, cash burn was enormous (>$50m in adjusted EBITDA loss), and the company went current on their debt (which is due in December 2026).

After such a rough year, you could imagine everyone at the company was looking forward to a nice, relaxing Christmas. SKLZ’s board certainly did their best to help make everyone comfortable: on December 23, they filed an 8-k noting they’d given “ordinary course 2025 annual long-term equity incentive grants to its employees”; in addition, the company gave the CEO a special one time grant of PSUs that vested at increasingly aggressive stock price targets:

Those special PSUs vest in four years, and SKLZ stock was trading <$5/share when the awards were given. So, on the low end, SKLZ needs to be a 4 year double for the awards to even start vesting. On the high end, you’re looking at a 4 year four bagger.

I have no view on SKLZ. But I highlight it because the company is seemingly a mess and they filed an 8-k after 4 PM on December 23 noting they’d given their CEO a special award that could be worth almost $20m. As detailed in the FRMM case study, when companies make filings around holidays, it’s generally because they’re trying to hide the information from investors, and I’d argue both the timing and the structure of this grant (with the awards being really buried inside the 8-K’s text) suggest a company that is trying not to draw investors’ eyes to the award. That’s curious; most companies try to shout from the rooftop when they’ve given their CEO an award that aligns them with the stock going up (GME certainly did)!

Why was SKLZ so shy about this award? Is it possible they’ve got some rabbit in their hat that makes hitting the targets likely, and they didn’t want shareholders to accuse them of tilting the scales for their executives when the stock takes off and the execs make a fortune?

Ok, that’s it for today. See you early next week for part 8 (and, if you haven’t yet, don’t forget to subscribe to get the rest of the series delivered to you!):

Today’s post is the seventh in the series; the previous posts include RELY + OPEN’s pay package, META’s YOLO options, incentives gone awry, an analysis of LION + STRZ new packages, the ACHC case study + premium dark arts basket, and this premium write up on my favorite current dark arts set up.

The line “the Special Committee will engage with parties who have approached the Company to date and evaluate proposals therefrom” is sneaky but reveals that people have approached about a merger

From early March, “I think we should target sort of 6 months after the IPO, market conditions providing, and then we will have completely separated the business. It will be an accretive deal for Medtronic over time. The impact on ‘27 depends on the timing of the split because the EPS accretion that you get is based on the number of shares -- share reduction that you get. So when we do the split, we exchange Medtronic shares for MiniMed shares”

Did some digging / scenario modeling on GTM

If stock stays down here, they retire one third of the float in two years with existing FCF, which makes the $2.50 per share FCF (first award tier) achievable. But they can't really guarantee the market will cooperate with a higher multiple so even then the first tier may be out of reach let alone the other tiers.

Also worth noting the founder CEO Schuck has already pulled ~$1.1B worth of stock proceeds out since IPO (~21.7 million shares sold), so the $600 million max upside comp package is probably not life changing for him anyway.

Interesting situation regardless, thanks for highlighting!

Hi Andrew, I have read several of your “dark arts” posts and wondered whether you have any data on how these situations tend to work out on average. My impression is that it is quite difficult to separate the wheat from the chaff.