Corporate dark arts: five bullish signals that aren't $AMCX $ALHC $VCTR $CHTR $BXP

Corporate dark arts, part 11

Today’s post is the eleventh in my “corporate dark arts” series1 and it inverts the usual post in this series; I’ll highlight setups that look interesting on the surface but aren't great signals on a closer look (at least IMO). My hope is that highlighting some less bullish setups will help illustrate why some of the prior examples I’ve highlighted are so uniquely bullish (at least IMO!).

Topics today include:

AMCX isn’t quite STRZ 2.0

ALHC: upside for me, but not for thee

VCTR’s pay for below average performance

CHTR’s token buys

BXP’s “big” extension

Let’s dive in:

AMCX isn’t quite STRZ 2.0

I mentioned STRZ in one of my earlier pieces. It’s a fascinating case study: an orphaned business that seems like a melting ice cube where the CEO and board are betting on huge upside.

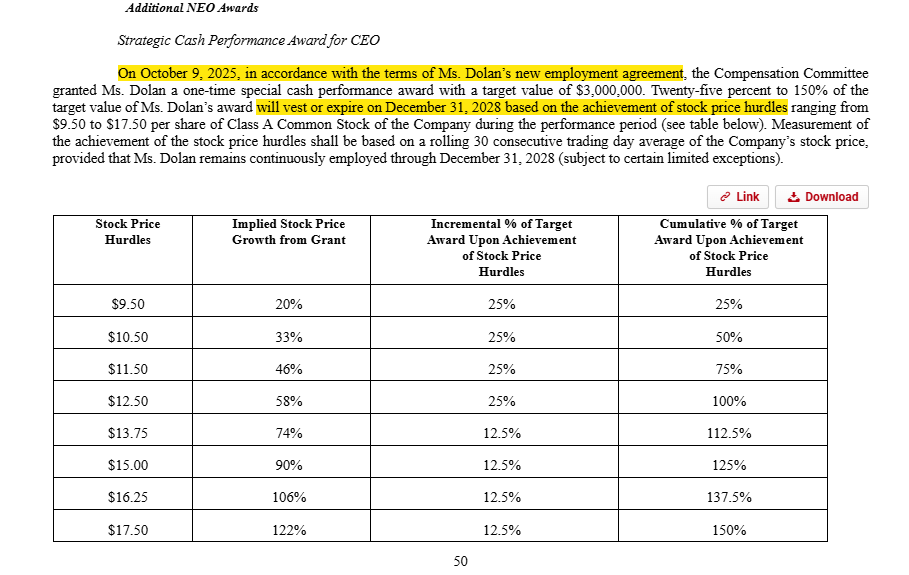

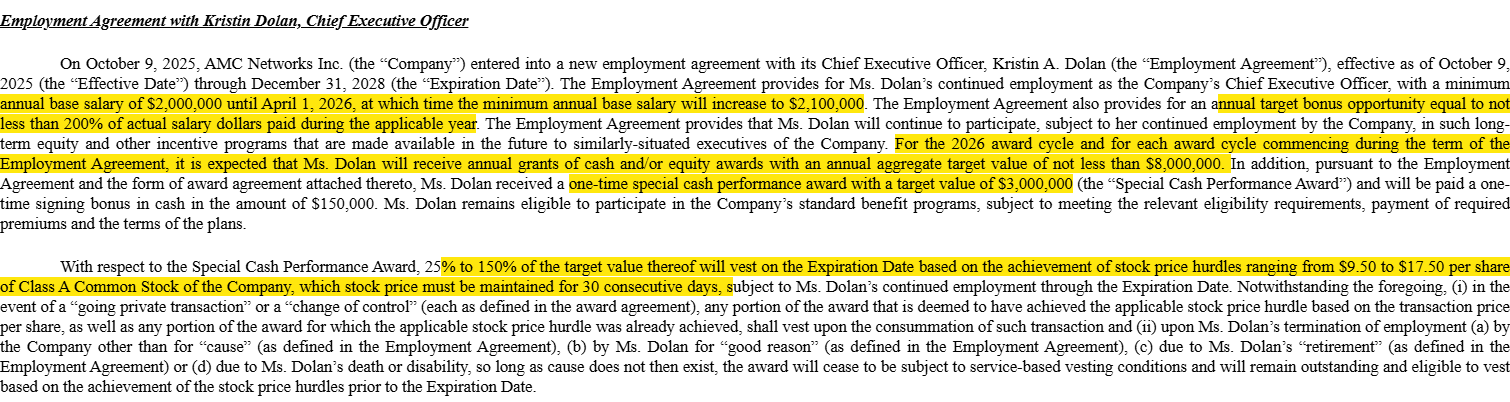

I’d be remiss if I didn’t mention AMCX alongside STRZ, as they gave a very similar grant to their CEO that requires the stock to more than double by the end of 2028 to vest in full:

While any aggressive grant is interesting, I have to admit I find these awards much less interesting.

Why?

Well, to start, note that the award pays out in cash, not stock. I just think it’s a little strange in a “telling on yourself” way if you’re incentivizing stock movement with a cash payout.

But the award is also very small. At max, the award would pay out $4.5m. The CEO gets $2.1m/year in base salary, an annual target bonus of 200% of base, and “not less” than $8m of equity awards/year. I’m sure everyone would love to get the stock up and have the bonus in full…. but hitting that full bonus would be worth ~half a year of the CEO’s annual comp. Just hard to look at the incentives and everything and think this is a real signal.

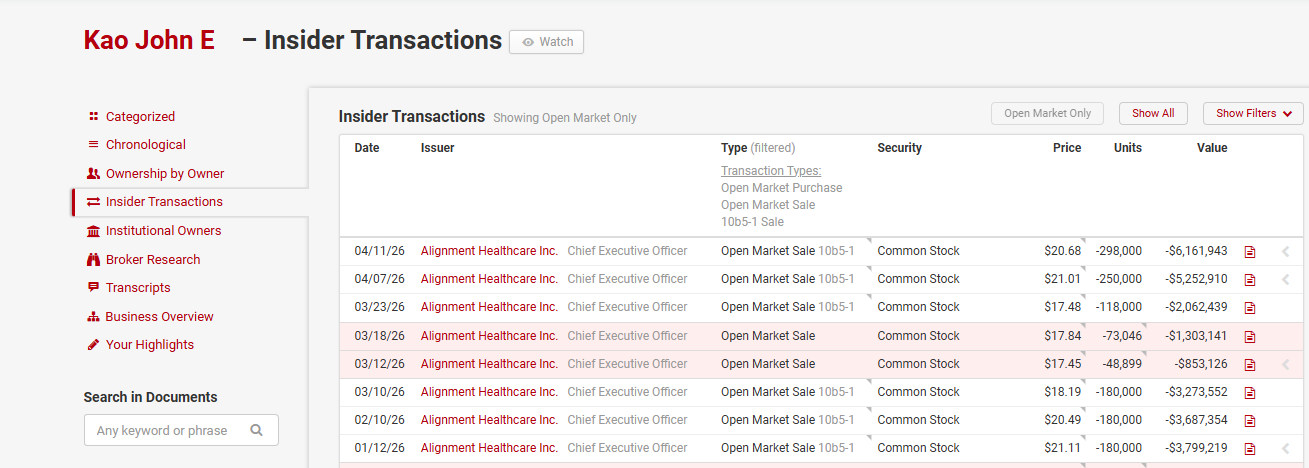

ALHC: upside for me, but not for thee

In February, ALHC gave their CEO a stock price based PSU grant. The stock was trading in the low $20s (it’s in the high teens now!), and it called for the CEO to get up to 1m shares if the stock could almost triple and hit $55/share over the next five years:

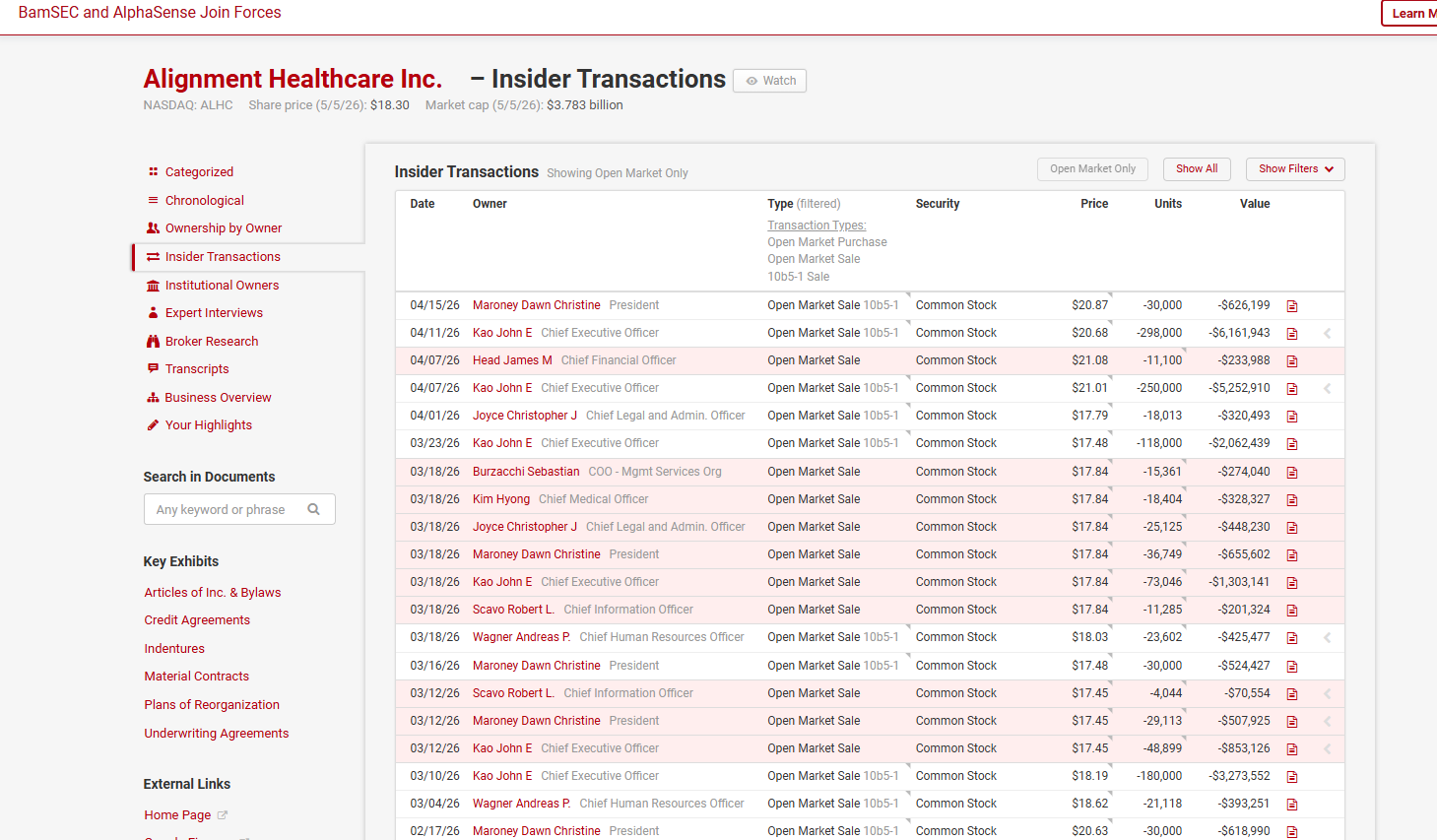

That’s an interesting setup…. but I’ll admit it’s hard for me to get pulled up on a PSU grant as a real bullish signal when everyone at the company is selling on the open market…

And the CEO has sold more shares on the open market since the start of this year than he’d earn in this PSU grant…

In general, I like grants that seem like everyone around the table is bullish on the company and trying to get equity upside exposure. At a glance, ALHC’s grants look like that…. but when you see the everyone involved selling stock like crazy while making this grant, it kind of seems like they’re trying to have their cake and eat it too (sell all of their stock without losing the upside).

VCTR’s pay for below average performance

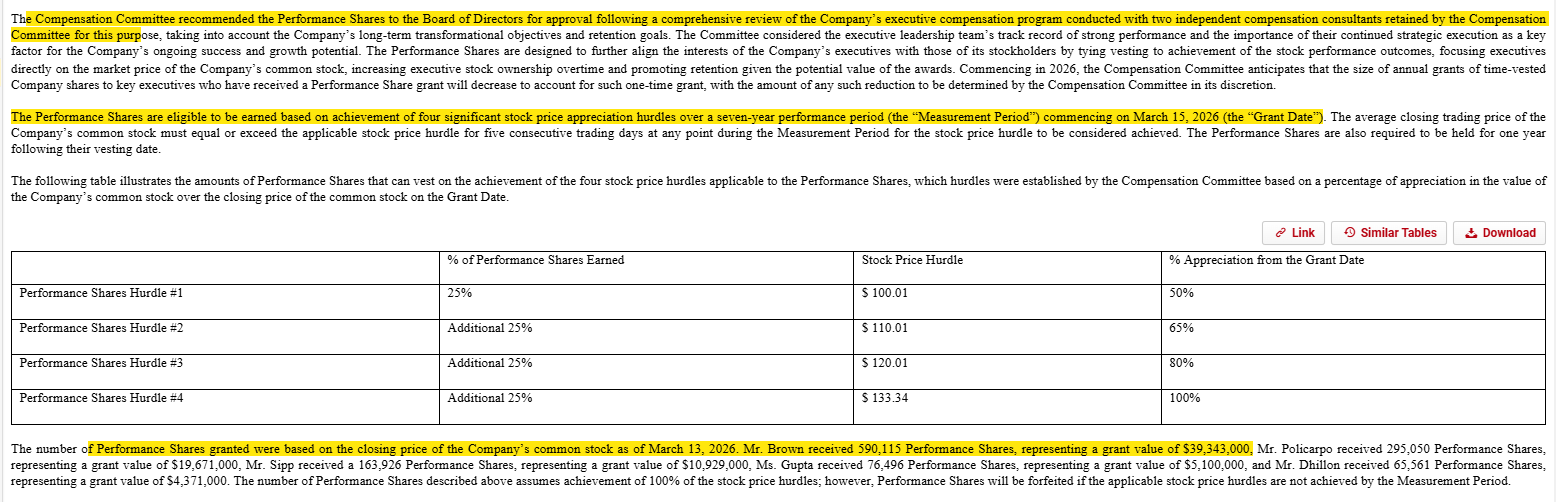

Sometimes the details matter. VCTR gave their CEO a huge stock price based grant that would see their CEO make >$70m if he hits the high end of their targets.

Seems aligned, right?

But take another look. Those grants vest over seven years. VCTR’s stock was in the mid-$60s when the grants were made. So, yes, the high end of the grant requires the stock to double…. but a double over 7 years is a ~10% IRR. That’s good but nothing spectacular. Is it really worth giving the CEO a $70m windfall for good performance?

And the stock would need to increase by >6% to vest on the low end. That’s less than the average annual return for the stock market; what’s the point of giving the CEO a bonus for below average performance?

Weird and disappointing.

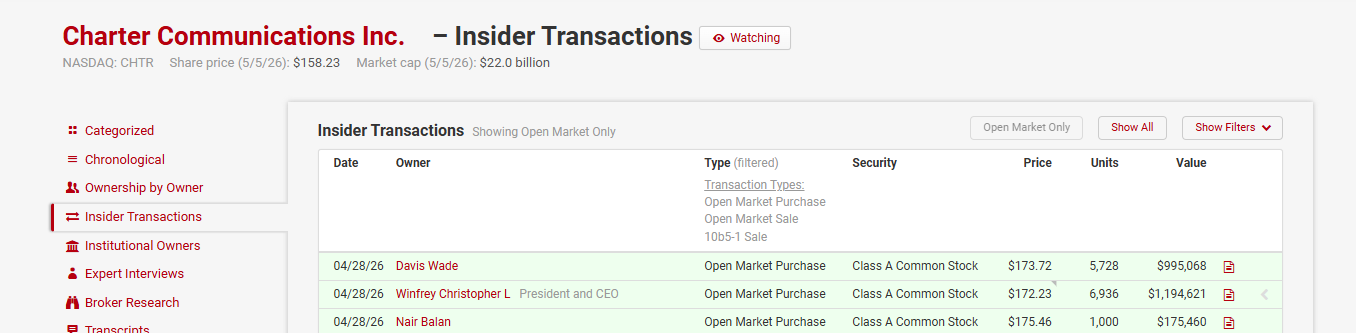

CHTR’s token buys2

After their stock puked (yet again) on a horrific Q1 earnings report, Charter saw multiple insiders step in and buy stock on the open market, including a ~$1m buy from their CEO.

Cluster buys (where multiple insiders buy a stock in a short period) are generally bullish signals…. but I’d contend CHTR is much more “window dressing / trying to prop up the market” than any actual bullish signal.

Why?

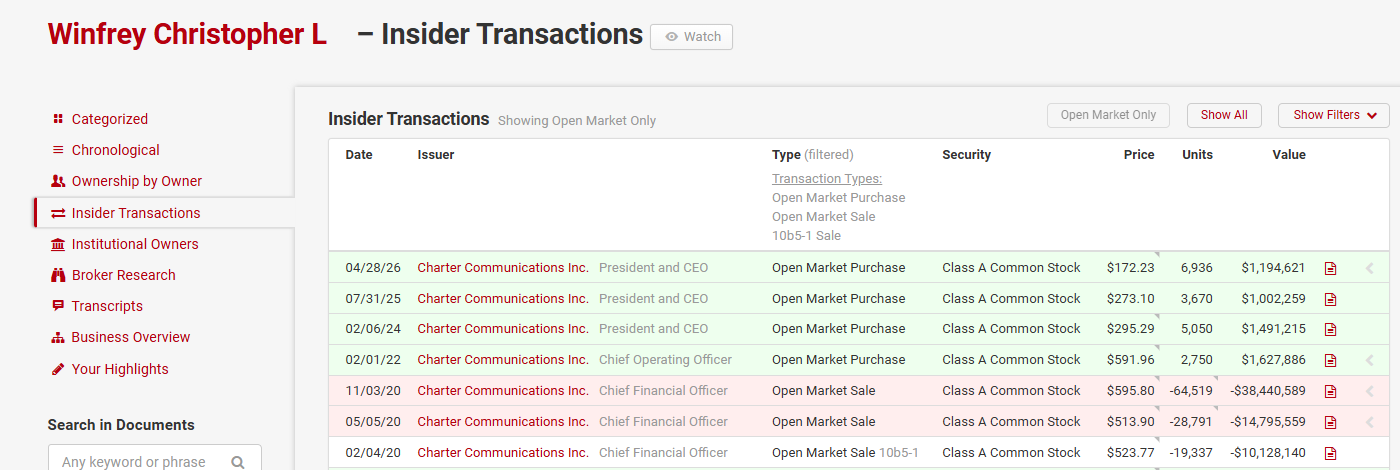

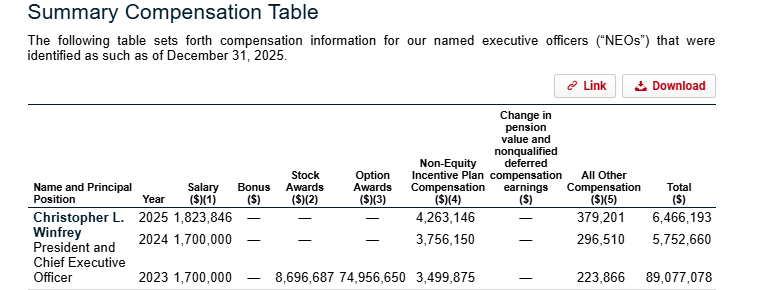

Well, CHTR’s CEO sold ~$60m in stock in 2020…

And he makes ~$6m/year despite taking multiple years of stock and options awards upfront back in 20233!

Note that 2023 massive payout was a bullish signal that failed hard; given that history, it’s even harder for me to think a $1m insider buy is some type of big signal once you factor in that history and the $60m+ in historical sales.

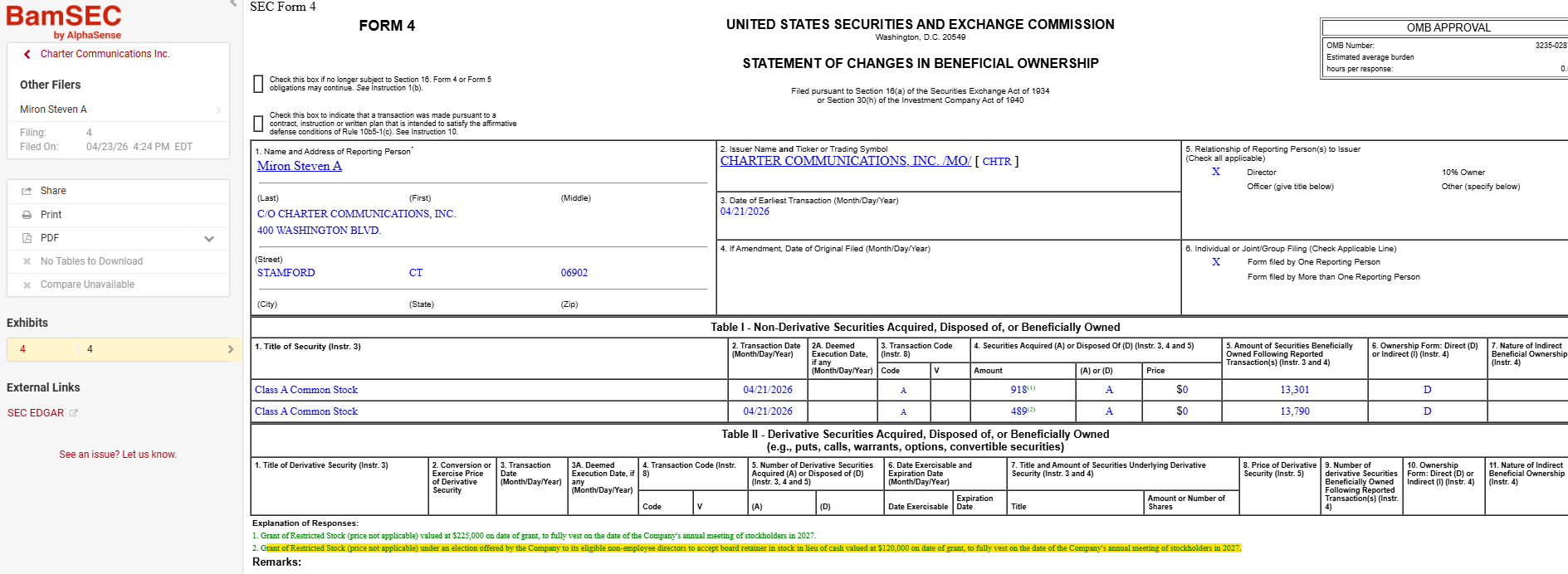

PS- maybe I’m being too harsh on Charter. Worth noting that, alongside this cluster buy, multiple directors chose to take their board fees in stock, not cash, in late April4:

BXP’s big extension

In December, BXP extended their CEO’s contract through 2029. The press release announcing the extension notes that the extension was “intended to more closely align the term of his employment with the multi-year, strategic action plan introduced at BXP’s Investor Day on September 8, 2025.”

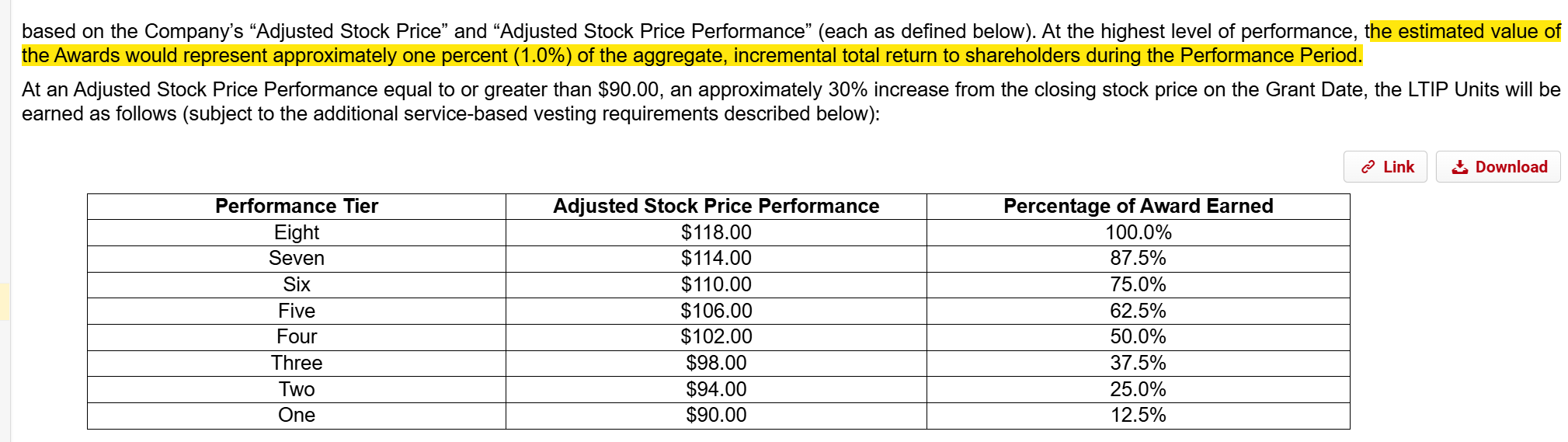

As part of the extension, BXP gave basically every top executive stock price driven PSUs:

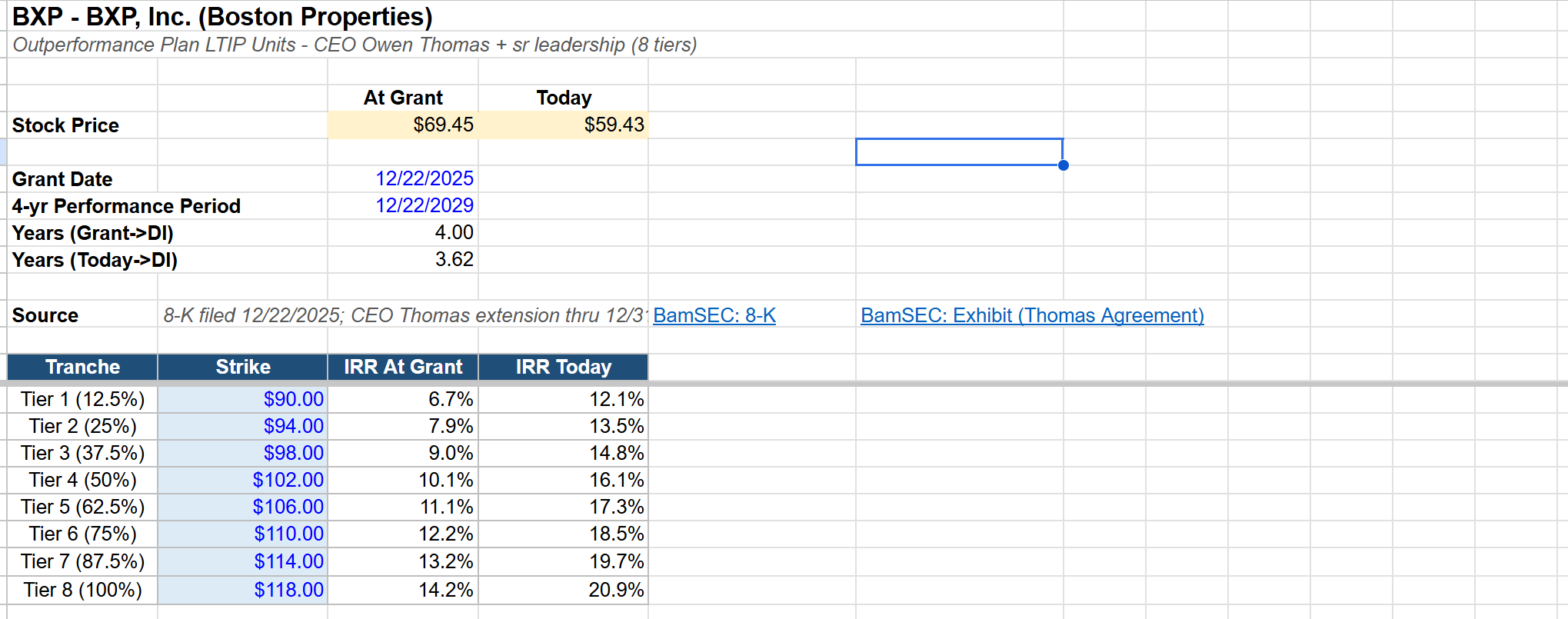

At the time of the grant, these PSUs weren’t insanely aggressive. The low end required the stock to do <7%/year, while the high end required 14% annualized. These aren’t “lay up” vests like VCTR, but I wouldn’t say they’re the most upside torqued. However, BXP’s stock has drifted down a decent bit in the six months since the grants were made…

And that means on a go forward basis the stock would have to perform pretty darn well for even the low end to kick in:

I’d note that the REIT industry overall hasn’t exactly shown skill in granting special awards; BXP is obviously quite down on those awards, and at the end of 2024, SLG gave their CEO a special grant that required the stock to hit $100/share by the end of 2029 to vest. Given the price performance since then, the stock has a long way to go….

So are the BXP awards interesting? Sure! But combine an industry that hasn’t exactly shown skill in timing awards with a bunch of executives that are very richly paid regardless of whether their special awards vest or not (BXP’s CEO makes ~$12m/year; the max payout on his special award is $25m. Yes, that’d be a nice windfall, but tough to argue he’s in the poorhouse without it!), and I don’t feel like these awards have as much signaling value as some prior entries in this series.

/Fin

There you have it: five stock motivated situations that look bullish but aren’t very high quality signals (at least IMO). Hopefully, today’s post helps set you up for post 12 in this series (which will serve as the series finale…. at least for now!).

Previous posts include RELY + OPEN’s pay package, META’s YOLO options, incentives gone awry, an analysis of LION + STRZ new packages, five more dark arts ideas, dark arts clues $SOX was about to go parabolic, the ACHC case study + premium dark arts basket, the incentives driving moves at VAC/GME/EKSO/RPD, and this premium writeup on my favorite current dark arts setup.

Disclosure: Shamefully, I’ve been a long time cable bull that has just had his head beat in repeatedly. I’m still long a (now very small) amount of CHTR.

That was a bullish signal that has not worked out; perhaps a writeup for another day!

I will further note that many directors have been taking fees in stock, not cash, for years, so it’s a nice way to align with shareholders but I think the immediate signal value is minimal

Is there any price where taking a flyer on CHTR makes sense to you?