Digital Asset Treasury companies and mNAV premiums (part 1: overview + bull thesis)

It’s been a while since a post received as much feedback as last weekend’s post (mNAV premiums, market multiples, and relative value). There were three major pieces of feedback:

I started the piece by noting that, given the recent strong run for equity markets, returns going forward were likely to be lower than normal. I will be honest: I recently read the Snowball (and did a book club on it!), and I think I had Buffett’s infamous Sun Valley warning (which Snowball kicks off with) on the top of my head. I had several people note that my warning might be right in the shorter term, but that it was almost certainly likely to be wrong in the longer term, as even a pretty strong run of recent stock performance doesn’t really change the long term calculus for long term returns. I’m honestly unsure; we’ve rarely seen multiples this stretched, and we’ve already gotten a lot of tailwinds (we’ve had enormous tailwinds on tax rates, interest rates, and fiscal support over the past ~40 years; I feel like we have headwinds from all over the next 40)…. but history suggests that my caution is misplaced long term. Markets have annualized at >8% since Buffett’s infamous warning!

I contended “I personally think it’s crazy that crypto-treasury companies trade for a premium to NAV”; I had lots of people email me asking to back that claim up / dive further into why a crypto treasury company shouldn’t trade for a premium.

Similarly, I had lots of people who responded to that claim by telling me why they think crypto-treasury stocks should trade at a premium to NAV.

Given the volume of inbounds, I was tempted to do a write up discussing Digital Asset Treasury Companies (DATs) and why I don’t think they should trade at a premium… but doing a write up would take a lot of effort, and to be honest I can be a little lazy and I wasn’t sure I wanted to sink that much effort into a post. So I was leaning towards no….. until I read the MSTR Q2’25 earnings call. I always find the MSTR earnings calls insanely interesting, but one particular line on the call got me so titillated that I couldn’t help but put some thoughts on paper. The line?

On the one hand, we're capitalized on the most innovative technology and capital assets in the history of mankind. In the other hand, we're possibly the most misunderstood and undervalued stock in the U.S. and potentially in the world.

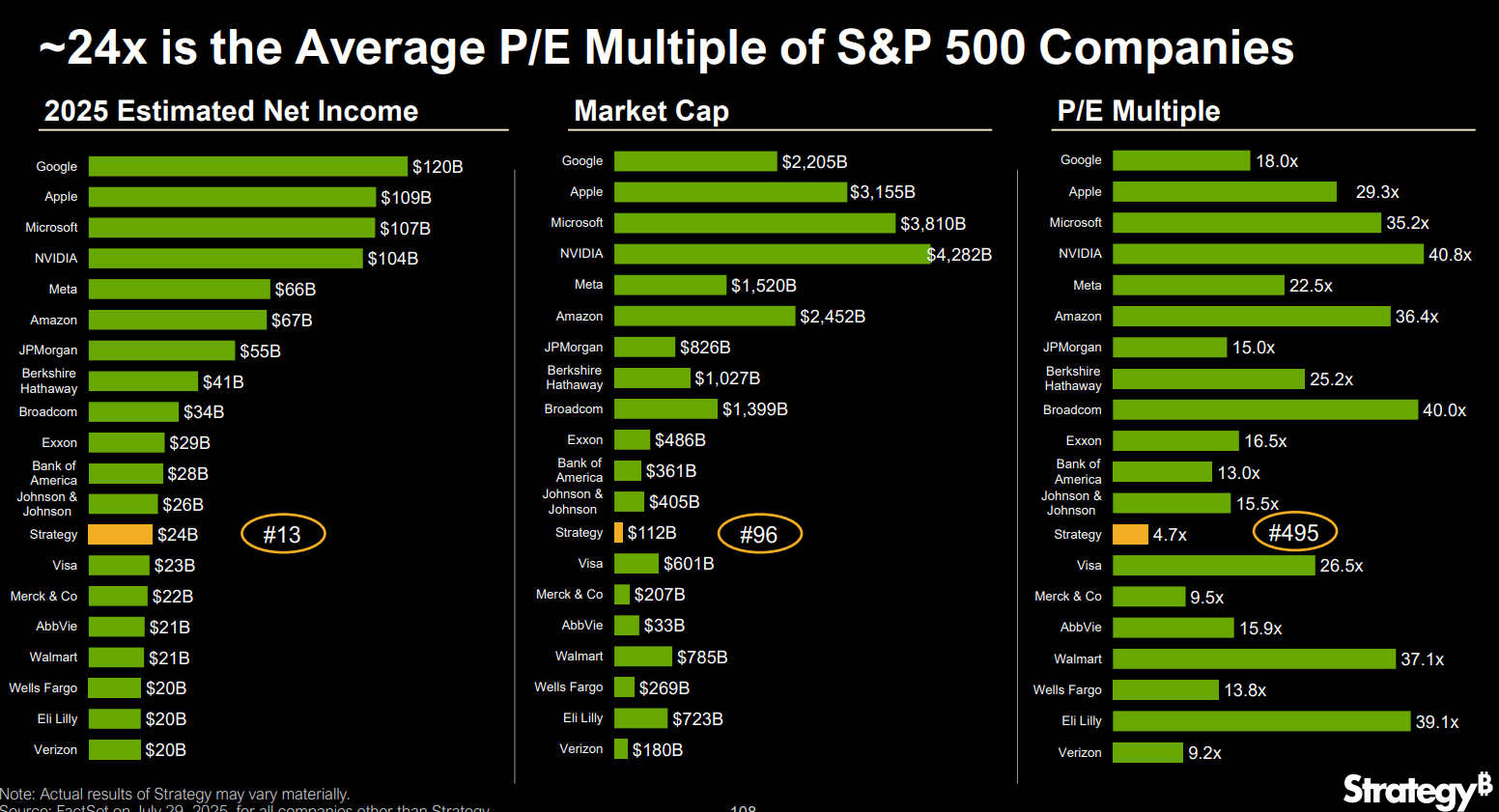

I don’t drink or do drugs or anything…. but honestly, I’d find it difficult to believe there’s an illicit substance out there that could get me more high than that line, and the cherry on top is they gave that line right after presenting the incredible slide below that argued MSTR was cheaper than all but a handful of S&P 500 companies:

Given how captured I was by that argument / slide, I wanted to spend a little more time breaking down crypto treasury companies and why I don’t think they should trade at a premium to NAV. (Editor’s note: this post ran crazy long, so I’m breaking it into two parts. This post is part 1 and covers background, definitions, and the bull arguments. Part 2 covering the bear arguments against DATs trading at a premium as well as the “number go up” and “stock price bro” arguments for DATs will publish later this week.).

Let’s start with a definition: a crypto treasury company is what I call a Digital Asset Treasury company (DATs). At its simplest, these are companies that have decided to hold digital assets on their balance sheet instead of cash. Theoretically, any company could do this; Google tomorrow could announce they were going to hold fartcoin instead of cash on their balance sheet and become a DAT. Google has ~$100B of cash on their balance sheet, so they’d immediately be the largest DAT…. however, their core business is currently valued at ~$2T, so their decision to become a DAT wouldn’t really move the needle on the stock price or give investors a clean play on a digital asset. In practice, most DATs generally don’t have much of an operating business attached; they become a DAT and basically turn themselves into a pure play on DATs / whatever crypto they’re buying. Most (but not all) DATs tend to lever up, generally issuing convertible debt (taking advantage of their high volatility to issue low or no cash interest debt) to buy more crypto and turning themselves into a levered bet on the digital asset (which is part of their appeal).

The most famous DAT is, of course, Strategy (FKA as MicroStrategy, MSTR1). They effectively created the DAT model, and they are not shy about letting you know that their stock has been perhaps the best performing asset in the world since they went all in on the DAT strategy (slide below from MSTR’s Q2 deck).

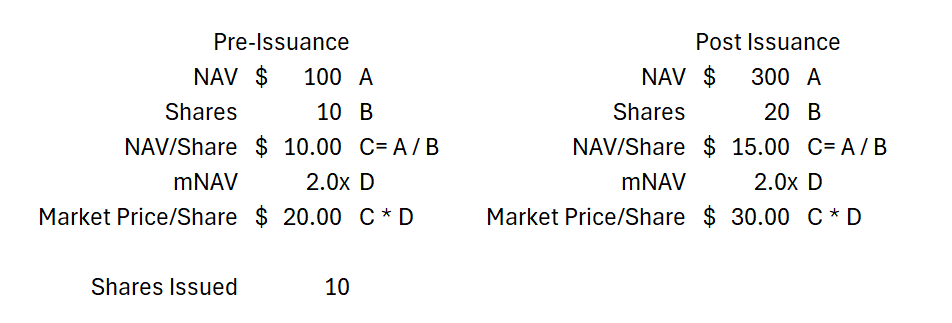

The DAT strategy / pitch has a lot of layers to it, but at its simplest the pitch is that a DAT company should trade at an mNAV2 over 1, or a premium to its NAV. An illustration might make this easiest: if a company has $100 worth of digital asset and no other assets or liabilities, their NAV is $100. A DAT might argue they should trade for 2.0x mNAV, or $200. If they do so, then they can issue stock and use the proceeds to buy digital assets. Because they are issuing stock at a premium, every time they do this their digital assets per share goes up. Pretend the company we just discussed had ten shares outstanding, so they’re trading at $20/share with an NAV of $10/share and a mNAV of 2.0x. If they doubled their share count by issuing 10 shares at market prices ($20/share) and used the proceeds to buy a digital assets, suddenly they have $300 of NAV and 20 shares outstanding, driving NAV to $15/share. If the company maintains the same mNAV multiple, the stock will go from $20 to $30/share. Everyone wins! (Table below that lays out the math simply).

It’s a simple argument, and it rests on one key assumption: that a DAT should trade at a premium to NAV. Bulls (including Microstrategy) would argue there are a lot of somewhat interconnected reasons a digital treasury company should trade at a premium to NAV, including (but not limited to):

Increasing amounts of crypto exposure per share (“amplified Bitcoin”): this would be the number one argument for most DAT bulls. Through the use of leverage and perhaps issuing shares above NAV, a DAT can increase the amount of crypto each share holds over time, and this deserves a premium. Saylor refers to this concept as MSTR representing “amplified Bitcoin” and explains it well on MSTR’s Q2 earnings call:

I want to explain how we amplify Bitcoin, okay? So we start with 199,000 Satoshis a share. And if we have no leverage, if we have no credit strategy, we couldn't issue credit, then 10 years from now, we've got 199,000 Satoshis a share. That's like an ETF. That's a BTC factor of 1. But if we issue preferred that's equal to 10% of our Bitcoin assets, that's 10% leverage, it turns out that we have 267,000 Satoshis a share at the end of the period because we're not diluting the common stock as rapidly as we're building the Bitcoin. And if we go to 20% leverage, you see you end up with 376,000 Satoshis a share. And now let's go to 30% leverage.

So you can see at 30% leverage, we would have 555,000 Satoshis per share. The green bars you see, that is the work that the treasury operation is doing. When people wonder what's the value added of a Bitcoin Treasury Company, it's the ability to create the green bar over the orange bar, and that's a 2.8 BTC factor. That means that -- what does it mean? It means, in essence, you would think that the floor for mNAV for a company that's got this sort of performance is 2.8, right? It's not the mNAV, but it's at least the floor. The mNAV of the company should be higher than 2.8

Ease of buying a DAT versus traditional crypto: you can buy MSTR with the push of a button on eTrade; buying Bitcoin directly is slightly more complicated

Wider variety of buyers: many traditional brokerages or retirement accounts won’t let you buy BTC or other cryptos directly; a DAT could be your only play if you want to have crypto exposure in those and thus should trade at a premium

Non-recourse leverage at the company level: if you’re an individual investor and you want leveraged exposure to bitcoin, you need to take on margin debt, which is obviously quite risky and exposes you to margin calls. Most DATs run with leverage, so by buying them you can get levered exposure to the crypto without the risk of a margin call.

Intelligent leverage: not only does a DAT give you non-recourse leverage to crypto, DATs would argue that they give “intelligent leverage” that will let them significantly outperform the underlying asset. As Saylor says on the Q2 call, “can we actually generate 2, 3, 4, 5, 6x Bitcoin performance with intelligent leverage? Yes, we can.”

Volatility monetization- DATs tend to have very active options chains, which allows investors to take advantage of them (either by buying or selling options) and the company to take advantage of them (largely by using high implied volatility to sell cheap convertible notes)

“Refinement”- Very much related to the volatility monetization argument, the refinement argument is perhaps my favorite argument for why a DAT should traded for a premium. I’ve included the full argument from Saylor on MSTR’s Q2 earnings call below, but simply put the argument is that a DAT can sell off different securities to different investors who want different return profiles and then keep the excess risk for themselves.

so what we're doing is refining and we're harnessing the power of the Bitcoin asset. And we're able to actually refine it into low volatility, low leverage, less risky financial products and then higher volatility, higher leverage financial products. So just like you might refine a barrel of crude oil into kerosene, which would be very, very pure and asphalt, which is not so much, we're basically providing a function that, say, an ETF cannot provide. You can see IBIT, the most famous example here in this chart. It basically wraps Bitcoin and it serves up a security flavor of raw Bitcoin to the investment community.

We, on the other hand, are offering stepped-down elements, convertible bonds, convertible preferred stock, senior fixed stock, junior high yield, preferred stock and of course, this treasury preferred stock in the form of Stretch. We're offering those. And those, in essence, we're stripping and modifying the duration of the asset. And we're also stepping down the volatility of the asset, and we're actually extracting the yield from the asset, which is Bitcoin, and we're serving it to each of these fixed income investors. But the excess yield, excess volatility, excess performance that does not go in those fixed income instruments goes into the MSTR common stock. And then, of course, that feeds to the MSTR-based ETFs and the MSTR options. So all of these are different instruments. They're all targeted at a different type of investor.

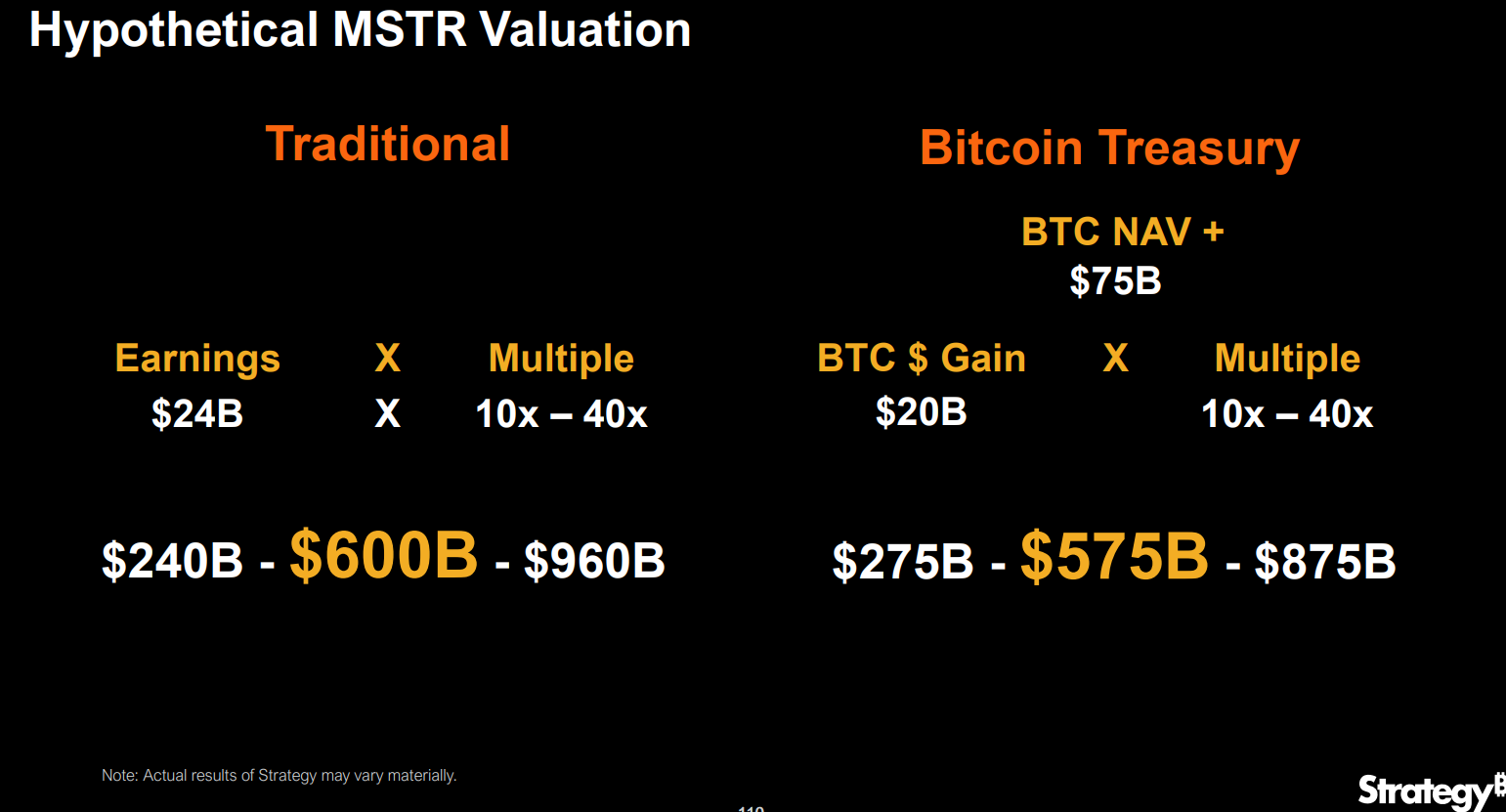

Investment gains: a DAT can’t just be valued on their NAV, because they will generate gains on the digital asset. Those gains could come from the digital asset going up, or they could come from issuing stock at a premium to buy the digital asset (see “increasing amounts of crypto” bullet above). Perhaps both! Those gains should be capitalized with a multiple, and if you properly capitalize those gains the company should trade for a premium to NAV.

There are several other arguments that I’m sure DATs would make for why they should trade at a premium; if you’re interested I’d really encourage you to go check out the MSTR Q2 deck / earnings call because I think they do a really fascinating job of laying out the logic of why DATs in general and MSTR in particular should trade for a premium.

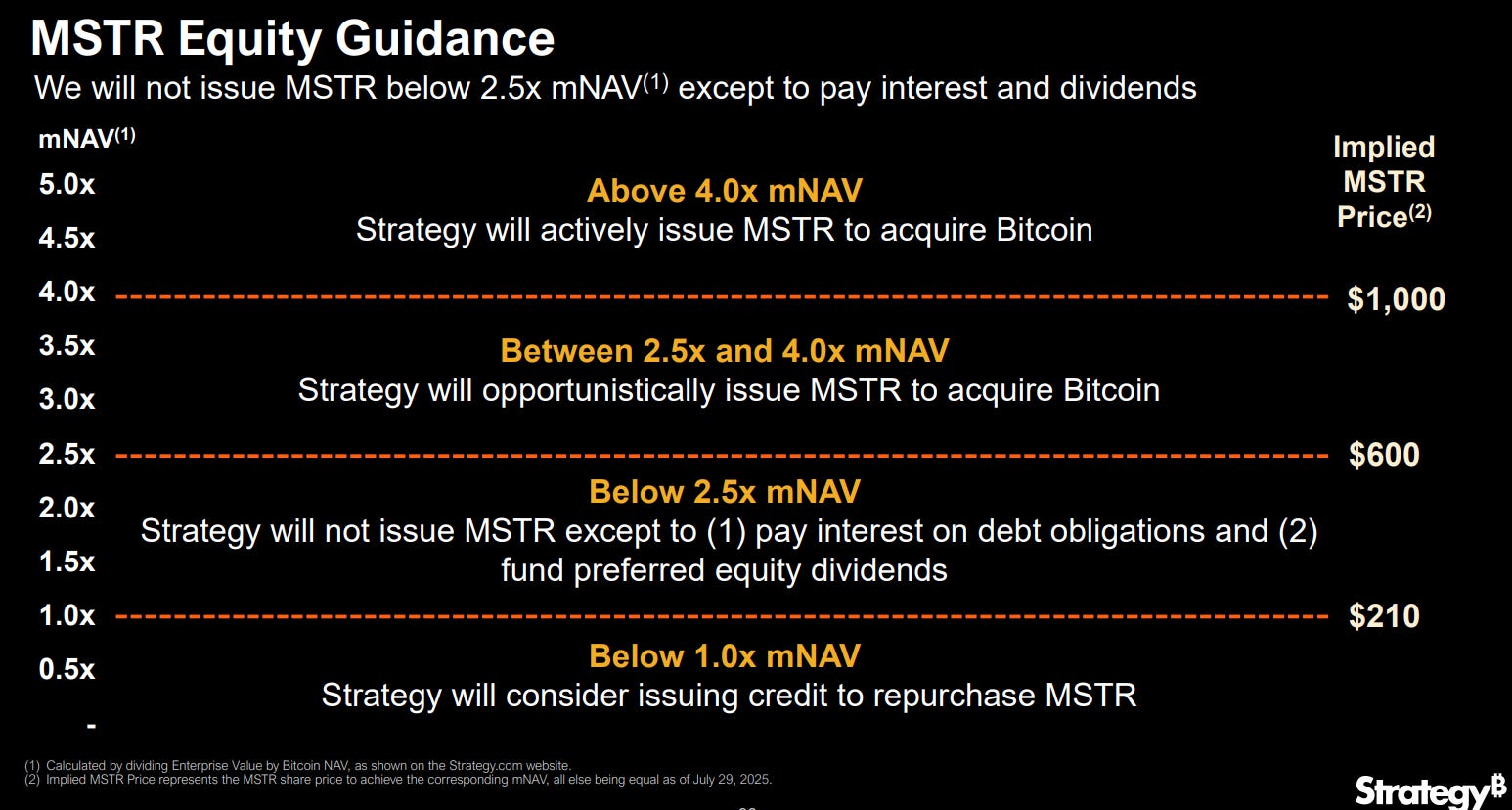

If you believe all of the DAT’s arguments, the question is what type of premium a DAT should trade for. Over at MSTR, they’d argue that, at minimum, they should trade for 4x mNAV3…. and MSTR is kind of backing that belief up with their actions by committing to only issues equity to pay dividends / interest if the stock is trading for below 2.5x mNAV4:

Ok, at this point I think I’ve nicely laid out what a DAT is and the bull points for why a DAT should trade at a premium to NAV. As you can probably guess given the opening of this article / tone, I’m pretty skeptical.

Why?

Well, I’ll save that for part 2 later this week. See you then.

I have a small short position in MSTR; remember, shorting is insanely risky. You should check out our legal disclaimer, but more than that you should heed the advice of a friend of mine “Dude, I had an irresponsible amount of money betting on pictures of digital apes, and shorting MicroStrategy is too risky even for me.”

Market capitalization to Net Asset Value, or NAV

“When we get above 4x mNAV above $1,000, which is our view, the minimum that our equity should really be traded at”

Of course, “only issue stock to pay preferred dividends and interest” is a pretty darn big caveat when you’re running a levered bet on an asset with no cash flows!

Saylor thinks he has discovered a perpetual-motion machine. I’m not sure exactly when reality will catch up with him, but it will… soon enough.

It reminds me of Wile E. Coyote, hovering in mid-air and only starting to fall once he realizes there’s nothing beneath him.

I think more ink should be spilled regarding how stupid mNAV is.