What is $GOOG seeing in AI? Part 3: the real bear case

This is my third and final post in my mini-series on Google’s big equity raise.

Part 1 (which you can find here) explained how unique Google’s equity raise and structure was. Part 2 (which you can find here) built on that piece; once you understood how unique the Google raise was, it isn’t a long throw to see how massive their capex spend is about to get.

I ended part 2 noting that it doesn’t seem like consensus has caught up to just how much capex the big AI companies are about to spend. Based on just their commentary and equity raises, it seems pretty clear that META and GOOG are going to blow away estimates for capex spending. Given there are rumors AMZN and MSFT are thinking about raising equity, I’d guess their consensus capex numbers are low too.

Remember that these capex numbers are enormous, so small misses can be pretty meaningful. Street estimates call for Google to go from ~$180B in capex this year to ~$240B in 2027. I believe their equity raise suggests Google will blow through that number; that belief means estimates are short by tens of billions of dollars. If META, AMZN, and MSFT capex estimates are off by similar amounts…. well, semiconductors and all things AI have been on a massive run so far this year, but if consensus estimates are that far off there’s a decent chance that the run has a long way to go.

It’s enough to make an investor want to throw caution to the wind and yolo into a basket of AI bottleneck plays. Sure, they’ve all melted up, but you’re talking about basically all of the world’s largest companies in an arms race to spend capex. Even after the melt up, it’s not hard to imagine that the market is underestimating the bullwhip effect that race to spend is going to have on near-term profits up and down the supply chain.

Given how bullish the implications of that capex boom are, I did want to try to throw some cold water on the first two posts with some of the bear points that are bouncing around my mind. I’ll run through the standard bear arguments (and why I’m skeptical of them) in a second…. but I’ll tell you upfront: the bear case that actually worries me comes from an old market saying: “I’ve seen gluts that haven’t led to shortages, but I’ve never seen a shortage that hasn’t led to a glut.”

The three most frequent bear points I hear are somewhat connected, and they’re the typical arguments you’ll hear against a speculative boom. They are:

AI is a circular business. Brilliantly captured by the meme below, a simplified example will show this best: NVDA invests in a hyperscaler who takes the money and invests it right back into NVDA chips. Thus, the demand and profits are somewhat self-perpetuating while the cycle is hot and every AI company can raise near unlimited amounts of money at ever increasing valuations. Eventually, that type of perpetual motion machine ends, and when it does you realize there wasn’t any real underlying demand. This concern has some callbacks to the dotcom bubble, when Yahoo would invest into a startup who would then spend the cash buying banner ads on Yahoo.

Demand is way overstated: Ever been to a concert that’s a little out of the way and needed a ride home? It’s a true free for all; everyone at the concert is requesting a car, prices are surging, and there are no cars available. You know what happens? Every person pulls out their phone and makes a request on both Lyft and Uber, and then they start cancelling the requests in favor of whatever will get there fastest. Imagine you’re there with your wife and best friend. The three of you will request six cars in total (three Lyfts and three Ubers), and then you’ll start cancelling the worst matches until a car finally gets there (i.e. if you get matched to an Uber 15 mins away and your wife gets matched to one 25 mins away, you’ll cancel hers). So Uber and Lyft each see way, way more demand than actually exists (in that example, they see a demand for 6 cars total even though real demand is 1 car!). Bears will tell you something similar is happening in a lot of the AI bottleneck areas; there’s a shortage in so many places that companies are placing orders with every supplier and then will start cancelling orders when they actually can find supply. There are parallels to this from the dotcom bubble; infrastructure (particularly fiber) was in huge shortage, so fiber companies would say that they were matching their capex to demand only to see most of that demand vanish when their capex came online.

Demand is subsidized and will fall off without the subsidies: Remember the height of the post-Covid boom when you had a ton of VC backed online companies that got funding at insane valuations and were using all that cash to acquire consumers with discounts and promotions? I live in NYC; for a while, if I was craving ice cream, it was cheaper (and sometimes faster!) for me to have it delivered to me than it was for me to actually walk out of my apartment and go buy it from the corner store a block away. Ubers and Lyfts were so subsidized for a while that, on the right route, they were actually cheaper than taking public transit. Bears would argue you’re seeing something similar with AI right now; the AI companies are so desperate for growth that they’re heavily subsidizing usage. So the demand you’re seeing for AI right now is AI demand at a heavily subsidized number…. but, in the same way I won’t get ice cream delivered to my apartment once a week without a massive subsidy when I could walk two minutes to the corner store to buy a pint, AI companies are going to realize a lot of this demand evaporates when it’s priced rationally.

I completely understand those arguments, and I’m sure there’s some truth to all of them…. but I think they’re misguided here. Why? Most of the companies that are racing to increase their AI spending (AMZN, MSFT, META, GOOG, etc.) aren’t just selling AI to customers…. they’re huge users of AI in their core business. And all of them are telling you that the ROI for the AI they’re deploying in the business is massive (remember Google led their capital raise call by noting AI is “lighting up every part of our business, driving an expansionary moment in Search, turbocharging Cloud and much more”). So this spending is being driven in large part by these companies seeing the tangible results of what AI is doing for them and thinking that is where the puck is going for other companies as well.

On the “demand is subsidized” point specifically, I’d also note that the history of all compute is everything getting drastically cheaper over time. Say it takes X tokens to replace a software engineer making $250k/year, and today X tokens cost $500k but the AI companies are subsidizing them down to $50k. Sure, that demand would collapse if the subsidies went away tomorrow…. but in a few years X tokens will actually cost $50k, and at that point the demand is real!

So I’m a little skeptical of many of the traditional bear arguments… but there is one bear area that I don’t hear about a lot that I think is worth exploring.

Let’s get back to that old “glut and shortage” saying. Right now, there’s an incredible amount of stuff in shortage: memory, power, etc. As discussed above, I think the demand for the stuff is real, so I don’t think the demand side leads to a glut…. but I’d be shocked if the supply side doesn’t lead to a glut. I mean that in two ways.

First, just on general AI infrastructure, in part 1 I shared this quote below from Google all the way back in Q2’24. I think it’s really instructive:

Google’s commentary on AI spend has evolved over time. Q2’24 is actually the last time they really defended increasing their AI spend; they’d soon just note that all their increases in capex were justified by “strong demand” or “healthy ROI on our investments.”

So I have no doubt that Google is seeing positive ROI on the investment that they’re putting into AI…. but they have also made clear that they will lean towards overspending rather than underspending. That’s actually a very rational wager; history is littered with companies that missed big shifts and saw their franchise evaporate. If you’re a multi-trillion dollar company like Google and the downside to overspending on AI capex is you waste a few tens of billions at subpar returns, but the downside to underspending is you miss the AI shift and your multi-trillion dollar franchise melts away, it’s pretty rational to lean heavily to overspending. It’s pretty clear that every other AI company of note is attacking AI in a similar “this is existential” way; it’s simply impossible to have an industry where every company is committed to overspending and not have some type of glut / excess. Even if they’re underestimating the near term demand, that simply means they’ll course correct and overspend once they’ve realized they underestimated near term demand. Eventually, you’ll get an overbuild one way or another.

But the more pressing concern for investors is in the bottleneck industries. Google has been telling you for years that they “obsess” around every dollar of capex they spend and that they have a “relentless focus on ROIC.” They’re prepared to spend hundreds of billions of dollars in capex. If you’re investing in a company that is currently experiencing a super cycle of profits thanks to shortage, you have to ask yourself not just how long that super cycle lasts and if the industry can maintain discipline around bringing supply online….. but you also have to wonder at what point does Google (or META, or AMZN, or MSFT) just build a competitor to you to end the supply shortage if your industry maintains supply discipline?

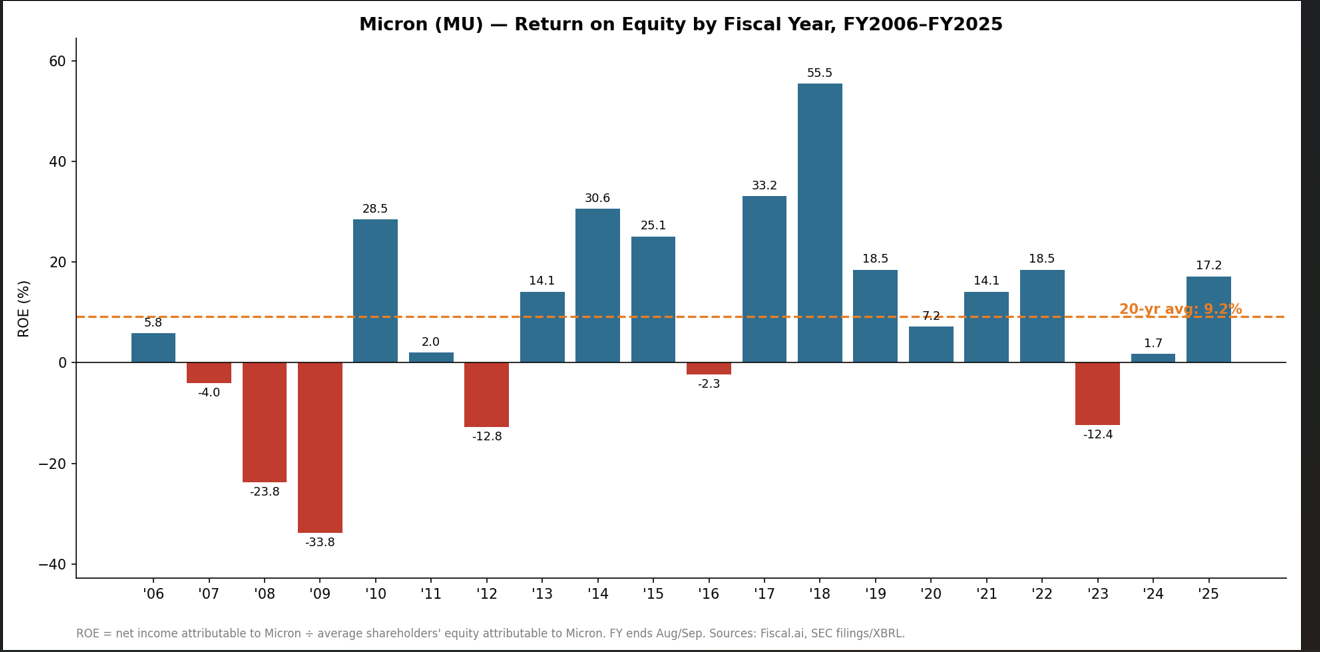

Consider Micron. Their book value is ~$65/share. If you strip out intangibles and excess cash, it’s probably closer to $50/share. They guided to ~$19/share in net income in Q3’26 alone, and I’m seeing consensus says they’ll do ~$100/share in EPS in FY27. I don’t think it’s crazy to say they’re doing >100% ROE right now.

Historically, memory is a very cyclical commodity business. Micron’s 20 year average ROE is ~9.2%:

That 9.2% ROE is somewhat dragged down by the GFC; if you want to cherry pick that out their 10 year ROE is closer to 15%.

Now, bulls will tell you that memory companies are an oligopoly that have gotten religion on avoiding oversupply. Perhaps that is true. And perhaps cheap Chinese competitors won’t emerge…. but, even if you believe all of that, Google is about to spend $200B/year in capex with a relentless focus on ROI (their words, not mine!). Micron has spent <$100B in capex cumulatively over the past ten years. How long is Google (or AMZN, or META) going to let memory companies make >100% ROEs and serve as a bottleneck in the AI supply chain before they just start building memory plants themselves?

MU (and memory plays like it) are going to earn a fortune in the near term….. but there will be a supply response at some point. And, given this spike is currently the mother of all shortages, I’d be shocked if it wasn’t met with the mother of all gluts on the backend. MU has done ~10-15% ROEs historically; I wouldn’t be surprised if the supply response from the current shock was large enough to push them well under that average for multiple years when the shock ends, and I think there are plenty of industries that are in shortage now that will face similar gluts. One way or another, the capital is coming….

I’ll wrap the series with a confession: part of the reason Google’s raise grabbed me so hard is that I’ve been thinking about (and working with) AI nonstop this year (if you missed it, my series on using AI as an investor starts here). The tools and possibilities for investors are improving just as fast as the capex is growing… and, in the same way GOOG and the big tech companies are leaning towards overspending because the downside of underspending is existential, I’m leaning towards “over-experimenting” with AI because the downside of not playing with it is somewhat existential….. so I’m always happy to swap notes on AI capex, using AI tools as an investor, or anything else!

PS- Might as well end by noting I’m taping a free webinar with AlphaSense next week completely focused on using AI as an investor; if you’re interested in learning more, you can sign up here.

Well said. Your thoughts echo my concerns with names like Nebius. How can Nebius maintain excess profits when it’s selling to the hyper scalers? Nebius profits are hyper scaler expenses. Why don’t they just finance a competitor? I appreciate that Nebius has an assembled workforce that gives it some human capital moatiness. But how long does that last with AI replacing human developers?

Great summary. What’s the conclusion?