What is $GOOG seeing in AI? Part 1: history's biggest, weirdest equity raise

I was shocked by Google’s big capital raise (and the rumors of META’s big potential raise that ended the week1).

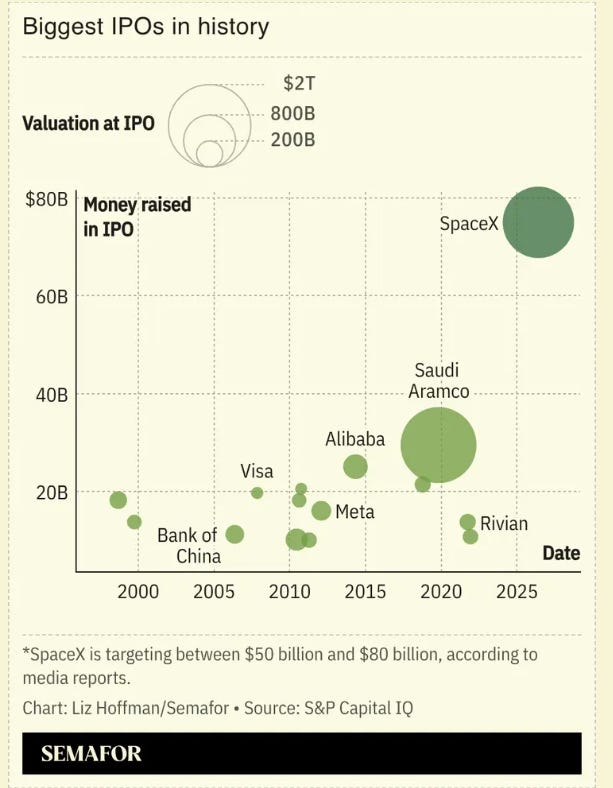

Ok, I’m not exactly breaking new ground with that statement. Depending on the day, Google’s EV is ~$4.5 trillion, making them tied with Apple for the second largest company in the world (NVDA is the largest at around $5 trillion). On top of their sheer size, the Google equity raise is the largest public equity raise in history2…. even larger than the pending SpaceX IPO.

Plus, to add a little bit more spice to the story, Berkshire Hathaway took down a huge slug of the raise, so the raise has a bit of a “Buffett blessing” piece to it3.

Put all of those pieces together, and the Google equity raise was well covered. Bloomberg had background on the Berkshire investment within 24 hours of the deal, basically every major publication (Reuters, WSJ, FT, CNBC) had some type of coverage, and you could find plenty of quick takes on what the raise meant (for example, Stratechery).

Still, I’ve been thinking a lot about the GOOG raise…. and, despite all of that coverage, I think there are a few interesting angles that haven’t been picked up, so I wanted to put some pen to paper on the topic. I’ll cover six topics in this series; they are:

A quick clarification on the mechanics of the raise

How unique this financing structure is

How Google broke from their own corporate history (and recent financial market history) in marketing this deal

Google’s capital allocation flip

What is Google seeing to raise like this?

The bear case

Today’s post covers the first four topics; part 2 (tomorrow) digs into what Google is seeing, and part 3 wraps the series with the bear case.

First, a clarification on the raise mechanics that will be important later. While the headline number here is “Google raises $85B in equity”, it’s actually split into two tranches: they raised ~$45B this week, and they’ll raise the other $40B through an at-the-market (ATM) offering that will start in Q3.

Second, let’s dive into just how unusual that structure is. Google is raising $45B now and $40B through an ATM later this year. ATM programs are by no means rare; they’re actually very common among capital heavy companies. Almost every large utility (NEE, SO, D, AEP, XEL) and REIT (O, PSA, DLR) has an active ATM program or has used one in the recent past. ATM programs are also very popular among smaller companies, particularly ones on the “meme” side of the coin (AMC and MSTR4 have been frequent users, and BBBY desperately tried to hit an ATM when they meme’d a few weeks before filing). ATMs have also historically been popular among companies in distress that need a lot of capital (the cruises and airlines were popular ATM issuers in and around COVID).

So ATMs are not rare…. but they are extraordinarily rare for a company with Google’s size and with Google’s cash flow and asset value.

How rare?

I cannot find a single S&P 500 company that is not a REIT or a utility that has an active ATM program. Google is a one of the five largest companies in the world and (as I’ll detail in a second), absolutely gushes free cash flow, haven’t done a secondary offering in over 20 years, and was buying back stock as recently as Q4’25. It is wild that they’d feel the need to establish an ATM.

Third, I think it’s really notable how Google broke from both their own corporate history and financial market history in marketing this deal. Alongside the raise, Google did a webinar with their CEO and CFO explaining the rationale behind the raise and provided a slide deck:

Google is aiming to raise $85B through this secondary / ATM; that’s an enormous amount of money in the absolute…. but Google is a ~$4.5 trillion market cap company, so the raise is actually a drop in the bucket relative to their size (<2% of their market cap in total, and ~1% if you’re just talking about what they’re raising this week). I see companies do secondaries all of the time; it’s pretty rare for them to have a public management call alongside the raise, and it’s even rarer for them to do a corporate deck. To give you an idea of how big a break from history this was: the largest previous follow on raise I can find was Boeing’s ~$24B raise in 2024; Boeing was a ~$100B market cap company at the time, so they were raising a much bigger percentage of their market cap…. yet they did their big raise without hosting a special call or producing a slide deck5.

Just on that history, Google’s current raise is already a major break from market precedent…. but it’s even starker when you consider Google’s own history. Google rarely produces public slides or investor communication with their top brass. Historically, they didn’t even do earnings slides; they only started providing slide decks with their earnings in 2025:

Alongside those earnings slides, they provided a deck when they bought Wiz in early 2025:

Outside of those few examples, I can’t find a single example of Google producing a financial deck in the modern era6.

Bottom line: Google did not need to produce a deck alongside this raise. Both Google’s own history and the history of similar raises suggest that Google could have done this without a deck…. but the fact Google decided to break so strongly with that precedent shows you just how important this raise and capital build out is to them (at least IMO!).

Fourth (and speaking of breaking with financial history), it is worth briefly noting Google’s capital allocation flip. Google has been a frequent repurchaser of their own stock. They bought back $62B in 2024 (at ~$165/share) and $45B in 2025 (at ~$190/share), and in April 2025 they had reupped their repurchase authorization by $70B.

A quarter by quarter look at their buybacks is really interesting: Google buys back ~$60B of stock in 2024. They keep up a similar pace to start 2025, buying ~$15B of stock in both Q1 and Q2. That slows to $10B in Q3 and $5B in Q4. They then don’t buy back any stock in Q1’26, and in Q2’26 they make the largest equity issuance in history.

Which would bring us nicely to the last question (and the one that will keep me as an investor up at night): what was Google seeing to do a raise this large???…. But this post is running really long. So we’ll have to hold off on that natural transition until we dive into part 2 tomorrow. See you then! (And if you haven’t yet, don’t forget to subscribe so parts 2 and 3 land straight in your inbox.)

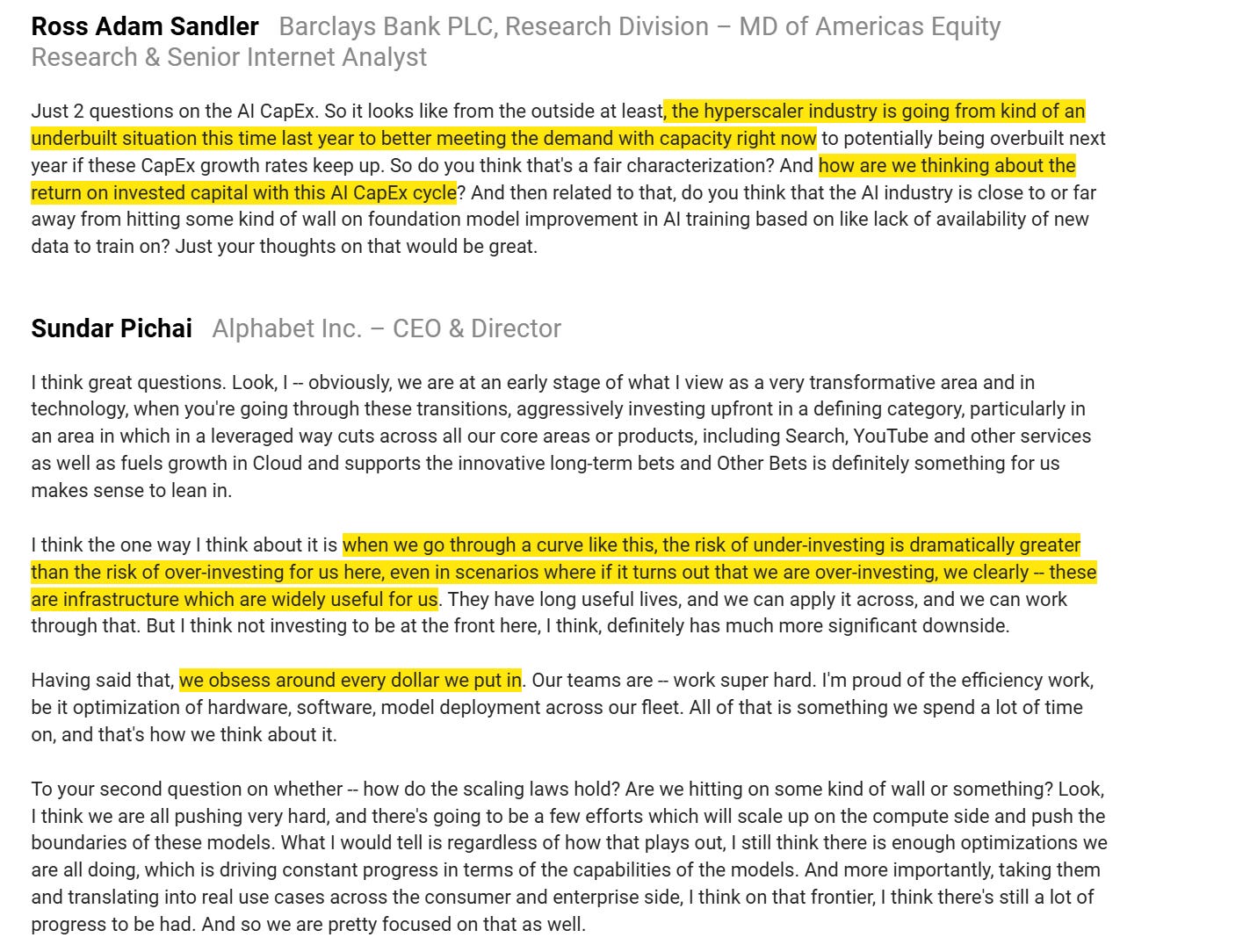

PS- at the risk of spoiling future pieces of this series, Sundar was asked about the risk of overinvesting in AI capex all the way back in 2024. His answer is really instructive on where this whole thing is going:

I wrote most of this article Friday morning…. before the META raise rumors came out. I think the rumors make everything in this article even more pertinent / interesting because you now have two mega-cap techs following the same pattern.

The previous largest I can find are Petrobras’s $70B raise in 2010, Saudi Aramco’s ~$30B IPO in 2019, and Alibaba’s $25B IPO in 2014. The previous largest straight follow on was Boeing’s ~$24B raise in 2024.

Yes, Buffett is no longer in charge of Berkshire, but he works there five days a week and Berkshire bought Google in 2025 when Buffett was still running the show. Combine the two, and it’s impossible to think he wasn’t at least advising on the decision to invest here.

Disclosure: I have a small MSTR short

At least none that I can find!

I asked Claude, and it suggested this is the first non-earnings deck Google has provided since hosting an analyst day in 2006.

Great deck observation - I wouldn't have guessed this would be the topic to trigger Google's first non-earnings deck since their 2006 analyst day. I think it really highlights how proactive Google is being about their capital allocation strategy. Instead of ignoring the elephant in the room, they decided to get ahead of the conversation and address investor concerns directly. Really enjoying this series…reading through them in order right now, ha

I guess they can see the looming concrete wall after three years of a market pumped by data centre buildout and hype, and not yet the actual ROI of that spend (extremely uncertain and likely non existent, at least in the medium term).

You can of course presume more optimistic scenarios, like AGI being invented next week or this being a simple case of GOOGL front running the avalanche of issuance. But I'm not sure either of those are bullish for the stock market either.