What is $GOOG seeing in AI? Part 2: Google's telling you the returns are real

I ended yesterday’s post on a mini-cliffhanger: what was Google seeing to do that equity raise?

That’s the question that kind of keeps me up at night right now, as the answer to that question has enormous implications for pretty much any area of the economy that is touched by AI (which, at this point, is basically every area of the economy).

Yesterday’s post focused on all of the ways Google’s big raise broke with precedent: the sheer size, the ATM program, the capital allocation U-turn (from share repurchaser to share issuer), and the way they marketed the deal.

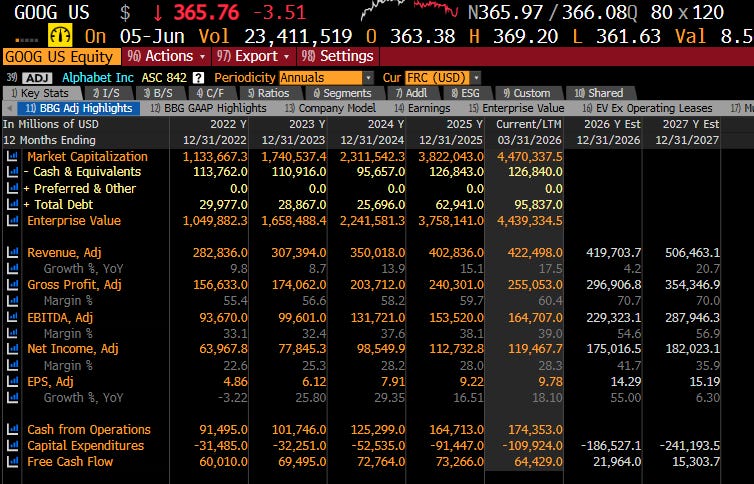

But I left one thing out: the thing that makes Google’s raise shocking. Google is gushing cash flow (they’ll do ~$200B of operating cash in the next twelve months), and while free cash flow is coming down as AI capex spikes, they are still decidedly free cash flow positive (~$10B of free cash flow in Q1’26 alone, and they will be solidly free cash flow positive in 2026). On top of all that cash flow, they have ~$50B of net cash on their balance sheet (plus another $100B of non-marketable securities that will get liquid real fast after the SpaceX IPO!).

It’s borderline insane for a company with Google’s financial profile to look at their business and outlook and think “we better raise some equity capital.” And it’s even crazier once you factor in their (recent) corporate history and how dedicated to returning capital to shareholders they had been. If any other company had this much net cash and cash flow and put out a press release saying they were cancelling their capital returns in favor of raising equity, the stock would have been down 20% and investors would have assigned the company a permanent “capital misallocation” discount while begging for an activist to get involved.

So that big equity raise marks a sudden U-turn; why did they suddenly change their tune?

If you’re a bear or an AI skeptic, perhaps the answer is simply looking at Google’s chart and thinking “hot damn, these guys are good traders! They bought back loads of stock when it was cheap in the $160s in 2024 and the $190s in 2025 only to issue it back when it was overvalued in the mid-$300s in 2026. Get these guys a hedge fund!”

But I don’t think that’s right. If Google was trying to just time their stock, I think they do a lot of stuff differently. For one, if they’re trying to just blast out overvalued stock, they do the whole issuance now instead of saving ~half for the ATM program that starts in Q3. They probably don’t do the whole CEO/CFO presentation showing what an opportunity AI is; that’s too out of line with their history. They just call their banks up and say “we want to print $85B of stock” and have it done in a few days.

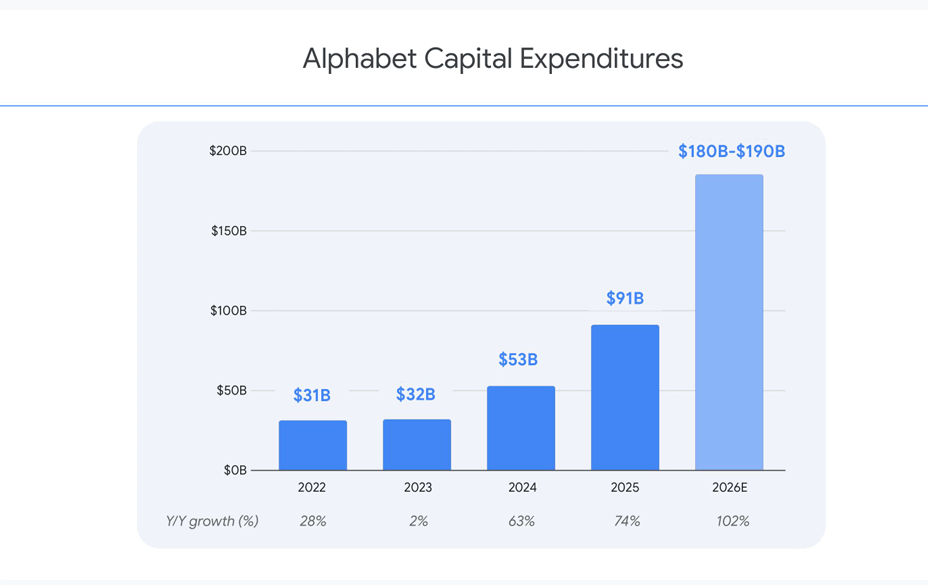

My read is that they really believe what they’re saying when they come out and say “AI is the most profound platform shift of our lifetimes. It’s lighting up every part of our business.” And they’re backing that talk up with their actions / capital allocation dollars; just under $200B in capex in 2026 and “significantly” more in 2027.

If you’re really online, you’ve probably seen someone say something like “GOOG is blasting out capex. They have better access to their roadmap and the bleeding edge models than you; what does that tell you that they’re seeing?” So I hate to repeat that point because it’s so overdone…. but the thing about that point is you don’t even need to infer it or play chess to reach that conclusion. On just that one capital raise call, Google is telling the whole world “our capital investments are informed by our view of ROIC.” Not only that, but they’re telling you that this capital raise (and the ROIC they’re projecting from it) is in large part informed by their customers’ backlog.

So Google isn’t just making up the AI demand and ROIC. They’re seeing it in their core business, and their customers are telling them about it and demanding more of it. Google is telling you that the return from investing in AI isn’t imaginary or speculative. They’re telling you it’s here, it’s real, and it’s happening now.

And the implications for investors are enormous. Google isn’t going to invest just this equity raise into AI. Google made clear on their equity raise call that they’re going to be financing their AI investments with everything they can: operating cash flow, the equity raise, and debt.

Remember, Google will generate ~$200B in operating cash flow over the next twelve months. They’ve got $50B of net cash on their balance sheet (plus another $100B in investments, largely from the SpaceX stake). They could easily take down $100B of extra debt. They looked at all of that and said “we need more equity capital, and we’re probably going to leverage that up.”

Bloomberg tells me consensus estimates for Google’s capex are ~$240B in 2027:

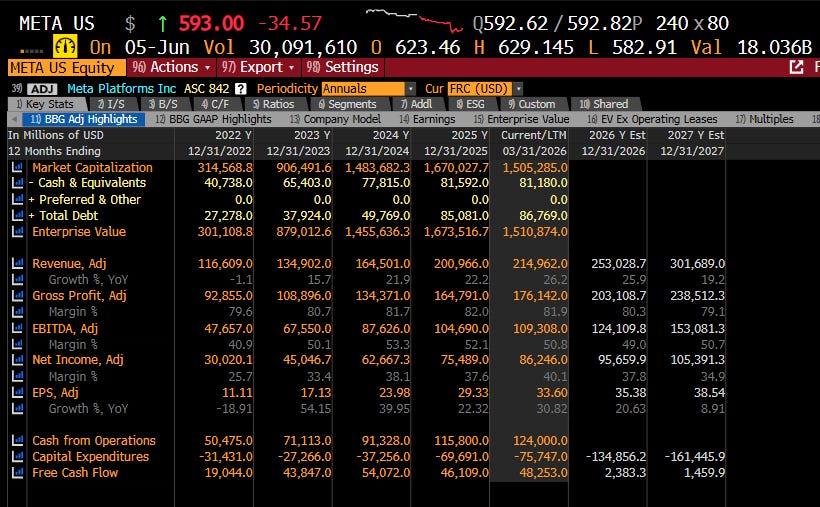

I don’t think Google’s raising $85B in equity capital thinking they’ll spend $240B next year. They could have paid that out of operating cash flow plus maybe dipping into their net cash balance a little! My guess is that the Google capex number blows away those estimates. Ditto Meta; consensus is for them to spend ~$160B in capex in FY27; I doubt they’re looking for “creative” ways to raise cash if their capex is going to be roughly in line with their operating cash flow!

Everything that touches AI (power, memory, semis, etc) has been in “melt up” mode over the past few weeks as demand gapped higher and prices went parabolic. My guess is that there’s more than a little euphoria in a lot of those stocks, but I will tell you this: it’s very hard to reconcile the Google equity raise with the consensus for Google’s capex in 2027. Google is going to blow through those projections. And, if the Google capex consensus is anywhere close to what the market is pricing in to all of the “AI suppliers,” then we could still have a long way to go before the market catches on to just how enormous the spend here is about to get.

But before you take that as a license to YOLO into a basket of AI bottleneck stocks, history has a warning about what happens when this much capital actually shows up to a shortage / price squeeze. I’ll talk about that bear case in part 3; see you tomorrow. (And if you’re not subscribed yet, sign up now so you don’t miss it!)

This quote in your part 2 really spoke to me - “So Google isn’t just making up the AI demand and ROIC. They’re seeing it in their core business, and their customers are telling them about it and demanding more of it. Google is telling you that the return from investing in AI isn’t imaginary or speculative.” This is the whole ballgame to me…Investors are correct to be skeptical and do their due diligence, of course. Never take what management says at face value…HOWEVER, you are right - we can’t just ignore that Google is telling us the demand is real…they are not bluffing. For me, this gives me some downside protection because it think earnings will be strong, and AI fears will eventually subside.

Why do you think markets seems to disapprove of hyperscaler (GOOGL, MSFT, AMZN, META) capex spend despite management teams saying on conference calls that they are getting high ROICs, accelerating growth profiles in their CSP arms (and Meta's FOA), and high (but declining ex GCP) margins on accelerating capital bases?

These businesses strike me as examples of Buffett's 'lots of capital at high returns' ideal, yet other investors seem scared off due to their increased use of OCF for reinvestment.

I vividly remember a time when investors were discounting big tech because they didn't have any use for the OCF other than buybacks (and were mad at some of them for their net cash balances - they wanted a dividend recap). Yet, now that they've found a new place to funnel OCF at internal ROICs (>20%) (rather than externally via buybacks / dividends at market returns), investors are angry/scared.

The whole reaction to reinvestment has been strange to me. I try to imagine that market reacting poorly to Costco reinvesting all of their OCF to open new stores, and can't. Yet, despite hyperscaler ROICs and margins being pretty well understood (approximately 20% and >30% respectively) increasing reinvestment in some of the best business models available (CSP/hyperscalers) is met with skepticism and fear.