The market is pricing $MSTR distress everywhere... except the stock

Most great stories follow the hero’s journey. Part of the hero’s journey is often “tests”, and one of the tests is sometimes a test of faith where no one believes the hero. Think no one believing Noah that the storms are coming (and thus he needs to build an Ark), or no one believing Harry Potter that Voldemort was back in the Order of the Phoenix. There are endless examples1 of this motif, but it’s particularly common in investment storytelling. It’s really hard to tell a good story about investing, so the way you generally build tension is you have the protagonist “know” they’re right but be pulling their hair out and wondering if they’re crazy as the world ignores what they know. Think of how all of the investors short mortgage securities talk about the 2006/2007 time frame (made famous in The Big Short); they were all wondering if they were crazy and how the market could be this complacent as it continued to go up… right up until the market cracked.

I kind of feel that way about Strategy (MSTR; disclosure: I have a small MSTR short, but am long several of their preferreds as well as IBIT against it). It seems clear to me that the entire capital structure is, to put it politely, royally screwed, and that the stock is broken…. yet the company continues to defy gravity and trade above NAV. I recently wrote a post about things that will be “obvious” in a few years; it seems “obvious” to me that in a few years MSTR will trade at a large discount to NAV and we’ll all wonder why it traded at a premium when it had so clearly already broken.

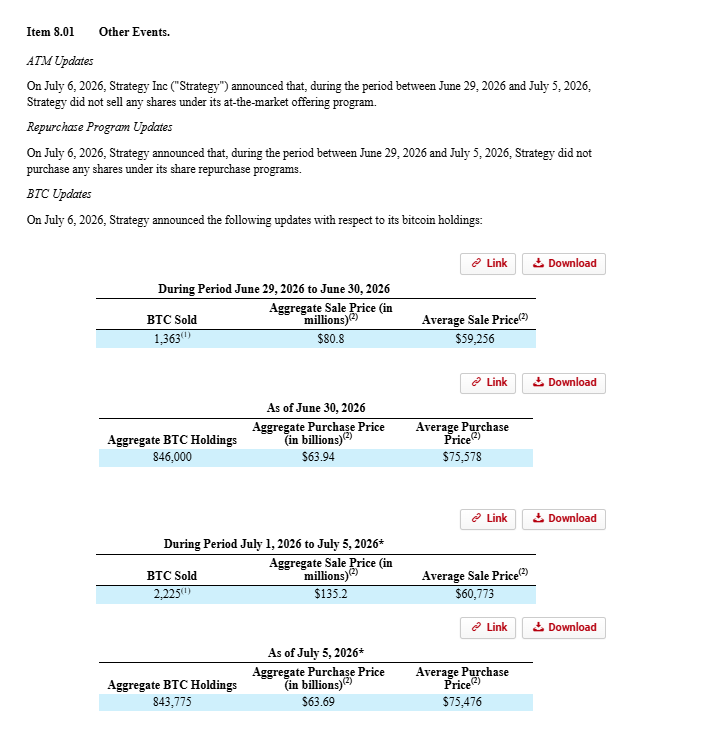

Let me start with the proximate reason for this post; on Monday, MSTR filed an 8-K noting they’d sold ~$216m in BTC over the past ~10 days.

Now, that’s a small amount of selling versus MSTR’s holdings of ~$64B in BTC, so you might be wondering what the big deal is.

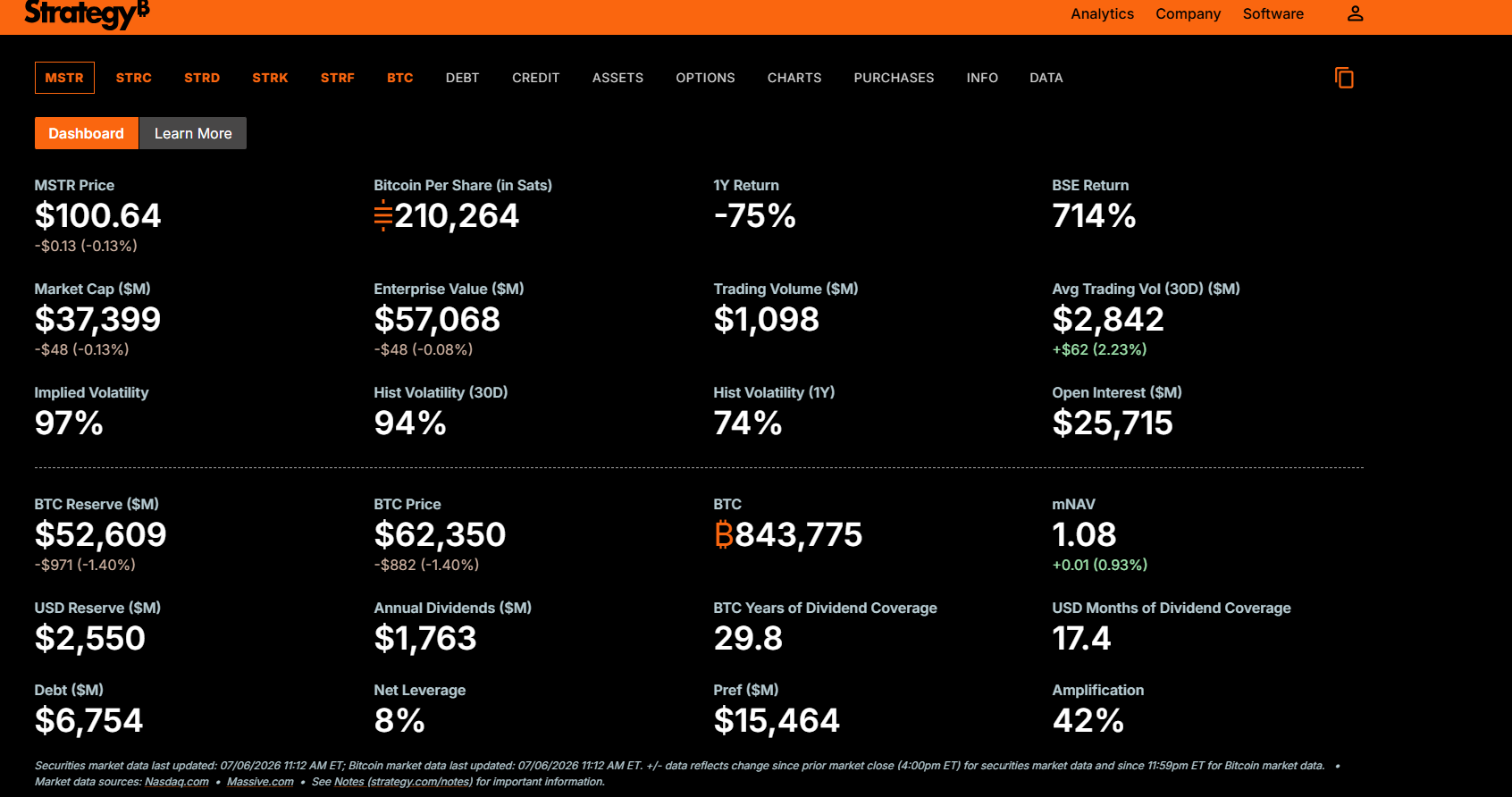

Well, MSTR took that money and parked it on their balance sheet; they now have ~$2.55B in a “USD reserve”. That USD reserve is intended to support MSTR’s prefs and debt. There’s ~$22B of prefs + debt outstanding, so MSTR is supporting their prefs + debt with >10% cash coverage.

I have done distressed investing before. When a company needs to keep 10% of their debt on the balance sheet as cash, it is not a good thing. That’s a sign lenders really don’t trust the company. And you can see that in the price of MSTR’s preferreds: STRD (MSTR’s most junior preferreds) trade for ~60% of face value.

So, on the one hand, you have the preferred market that’s massively skeptical of MSTR. On the other hand, you have MSTR still trading for a premium to NAV.

Now, MSTR is only trading at an ~8% premium to NAV. You might wonder why a mere 8% premium to NAV gets me fired up enough to write a full blog post comparing myself to a prophet on the hero’s journey.

The answer is (aside from me admittedly being a little excitable in general) that it just seems insane to me. Every rationale for owning MSTR seems dead at this point.

Did you own MSTR to get bitcoin exposure? A few years ago, that made some sense as it wasn’t easy to buy bitcoin. Today, that argument is insane; you can buy bitcoin in a few seconds with basically any brokerage account, or you can buy a bitcoin ETF like IBIT.

Did you own MSTR because DATs (digital asset treasury companies) are the future? A year ago, there were a ton of DATs getting raised, and all traded at big premiums to NAV. I was hyper skeptical, and I think that skepticism has proven accurate: today, basically all of the DATs trade at a discount; MSTR is pretty much the only one I’m aware of that trades above NAV.

Did you own MSTR for the “amplification” (leverage)? MSTR has frequently made the argument that you should own them because they provide bitcoin amplification. Basically, because they raise debt and prefs to buy bitcoin, they provide investors with amplified returns. I’ve always thought this argument fails because investors can leverage bitcoin on their own if they choose, but I think this argument is dead now too…. MSTR just sold down bitcoin to raise cash. Amplification (and bitcoin per share) is coming down!

Did you own MSTR for their trading acumen? Saylor was crazy early in spotting the opportunity in bitcoin; perhaps you owned MSTR because you wanted them to trade bitcoin (kind of like buying into a macro fund2). MSTR’s cost basis in bitcoin is >$75k, and they took out leverage to buy bitcoin up there. They’re currently selling bitcoin at ~$60k. That’s buy high / sell low if I’ve ever seen it; not exactly the stuff trading legends are made of.

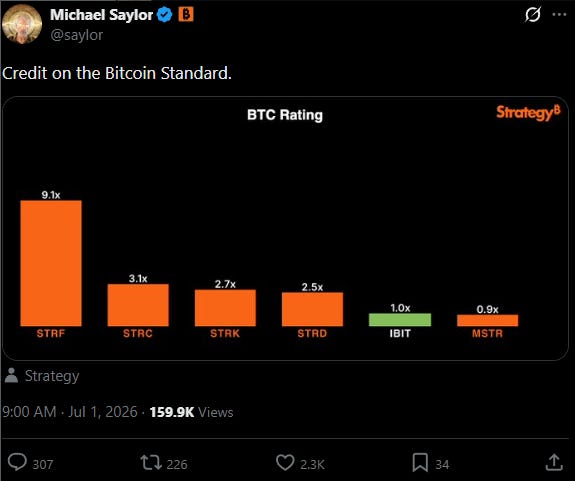

Did you own MSTR for their brilliant investor decks? Honestly, this one is still alive. MSTR’s decks are only rivaled by SoftBank’s for their sheer audacity and creativity. It’s hard for me to call out just one of their tweets3 / slides as particularly awesome, but there is something about comparing the BTC behind all of their different prefs (which often trade well below par!) to the BTC behind IBIT that strikes me as just particularly creative / audacious.

Altogether, it just seems kind of crazy to me. If I told you that there was a pile of liquid assets sitting around in a controlled company (Saylor has close to effective control of MSTR through super voting stock) with a management team that had a history of pro-cyclical trading (buying and levering up as the asset went up; selling and delevering as the asset went down) and with a bungled capital structure where some pieces of it were yielding >15% (again, STRD is trading just over 60% of face and with a >16% current yield), what would you guess it traded at?

I’d probably guess 70% of NAV, but I could go as low as 50% or as high as 90%.

There’s no world where I could see that company trading for a premium. Heck, unless the company had suggested they were open to liquidation, there’s no way I could see them trading around NAV.

Yet that’s where we are with MSTR4.

Is it just me, or has the world gone crazy5?

Given the Odyssey movie is about to come out, Cassandra is a very relevant one here…. particularly apt since Michael Burry uses it now!

MSTR’s CEO recently tweeted about them evolving to active capital management, so this is basically what MSTR is pitching themselves as going forward

Some of the ads they run for STRC are so audacious that I’ve started screenshotting them in case they ever get taken down…. and that’s before we dive into the “why do they need to advertise a preferred security yielding double digits” question.

I know there has been some debate about MSTR’s mNAV as it uses the face value of prefs and debt, not market value. It’s an interesting argument, but I think it’s irrelevant. If your bull case is that MSTR common trades at a slight discount to NAV because the prefs are trading at 70% of par….. well, good luck buying something at 95% of NAV because more senior securities trade at 70% and you’re “capturing” that discount!

Speaking of crazy, if you want to hear me ramble on about MSTR a little bit more, I went on my friend Travis’s podcast to talk MSTR last week.