When is "obvious" actually alpha?

What separates something obvious and priced in from actionable insight?

Imagine someone comes to you and says “there’s a publicly traded financial instrument; it has a strange quirk that can generate free alpha if you short it (or buy it).” What would you think?

In general, I’d be pretty damn skeptical. I’d think they were missing something; in fact, I remember a few years back a bunch of (largely retail) traders thought they’d found a free alpha hack by shorting the VIX or buying inverse VIX products (e.g., XIV)…. but they were dealing with incredibly complex products that eventually led to massive blowups.

So I’d be skeptical of the “free alpha” idea…. yet that’s exactly the thought process that led to my “free alpha” 2x levered short idea last week.

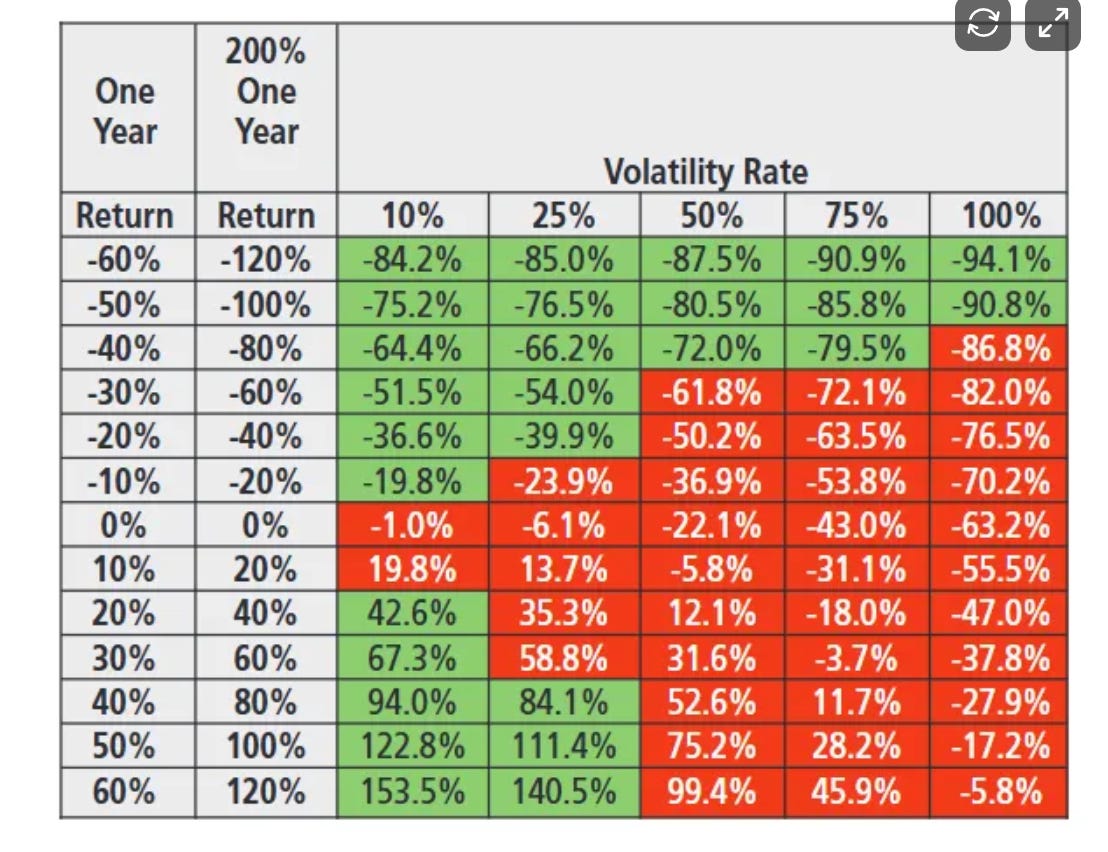

Quick refresher if you missed it: the table below is in the prospectus for every 2x levered ETF. Given how awfully the 2x levered product does (when the underlying is up 50%, it’s down 17% if vol is 100%), I thought there was “free alpha” in shorting a 2x levered ETF.

I was wrong. Some work with Claude suggested that the “structural decay” alpha I thought I was getting was actually just me picking up pennies in front of a steamroller: if the stock went parabolic, the 2x levered ETF would substantially outperform the underlying. (You can read last week’s piece for all my thinking on the trade, and why it was wrong.)

So if I already wrote up that trade and how wrong it was, why am I writing about it again now? Because I’ve been thinking a lot about the psychology of that trade.

On the podcast, I try to lead most conversations off by asking for an overview of the company we’re going to talk about. Then my second question is generally “the market is a competitive place; what are you seeing that the market is missing that makes this a risk adjusted opportunity?” And the whole “free alpha in a structural decay / prospectus” thing has me thinking: how deep does your knowledge / insight need to be to generate alpha?

Is it just enough to be right? I distinctly remember my first day at a consulting firm ~15 years ago talking to a guy who was in my incoming class. He had just gotten his PhD in computer science, and he told me he’d put 100% of his portfolio in Apple because their smartphone was so much better than the competition. I was already pretty interested in stocks, and I thought that was a silly thesis. The thesis seemed too obvious, and history suggested tech leads got squandered quickly (Apple became the king by killing BlackBerry / Nokia).

Well, my colleague’s “obvious” thesis resulted in a >21x over the next 15 years, slaughtering the indices. I hope he held on the whole time!

Saying “the iPhone is better than peers” back then was probably an easier / more simple observation than reading the 2x levered prospectus and looking for decay is today. Benefit of hindsight, it worked…. but was that just an n=1? Was it real, sustainable alpha? Does having real world observations generate alpha in a way that reading prospectuses does not?

If you’re saying reading prospectuses does not have alpha, aren’t you basically saying reading SEC filings doesn’t have alpha? If that’s the case, how are we as investors supposed to generate edge? I’m not saying reading SEC filings is that only way to generate edge, but most investors I know spend a substantial amount of time in SEC filings. Is that just wasted time if it can’t generate alpha?

If you’re saying that the structural decay component / mechanical nature of the 2x levered trade doesn’t have alpha, perhaps that is correct…. but there’s apparently tons of alpha to be made on polymarket by reading and interpreting the rules correctly (as mentioned in my June ramblings). How do you explain that alpha? Is it just prediction markets are immature and that will get arbed away over time?

I will be honest: I don’t have firm takeaways or anything. I’m just always pushing myself to think about edge and the type of edge that will get rewarded, and the structural levered decay piece has been a jumping off point for me to think about it a little harder. I have come up with a few “obvious” trades that could fit the bucket, and I’m planning on writing them up in the near future…. but if you have any obvious ones, I’d love to swap notes (particularly if they’re going to be a multiyear 20-bagger a la Apple!).

Hi Andrew,

I think you’ll enjoy this read:

https://content.rwbaird.com/RWB/Content/PDF/Insights/Whitepapers/Truth-About-Top-Performing-Money-Managers.pdf

To understand alpha, one must first ask whether alpha exists at all. In my view, the concept only really matters if you start from the efficient market hypothesis.

One good example of where alpha can exist is long-term investing as a possible source of alpha, with emphasis on “possible.” As shown in that study, top-performing money managers who outperformed over the long term also experienced long periods of underperformance versus peers and benchmarks.

That might lead us to believe there is an edge in long-term investing, combined with the ability to remain confident in your investments even when they lag the index. This does not mean that funds with drawdowns will necessarily outperform, but rather that those who do outperform often have to endure meaningful drawdowns along the way.

Classic short-term pain for long-term gain. Seems like Nike’s slogan might be the key to outperformance.

This is just one piece of the puzzle. You could argue that those funds that outperformed may not have done so on a risk-adjusted basis, given how much they lagged the market at times. My response would be: how are we defining risk? Is it the possibility of permanent loss, or is it volatility?

You could argue that, in this example, there is no time/risk/reward-adjusted outperformance, and that might be true. But we could add further variables to the mix: illiquidity, forced selling, ESG-restricted buyers, and so on.

My objective is to find areas of the market where I can achieve high returns because of variables the market classifies as risks and therefore demands higher returns for, but that matter very little to me.

For example: I can buy illiquid companies, in industries ruled out by many funds by prospectus, with a 10-year time horizon.

Open to discussing further.

I do think shorting levered ETFs is a form of alpha. Shorting anything has right tail risk, so I understand the compounding risk. But these products are essentially an expensive form of leverage that appeals to short term traders, retail investors who don’t / can’t use margin, and IRAs. You are being compensated - in my view, more 5an fairly - for providing that.