Is insider buying a signal if the insiders are always wrong? $LILAK

Look, I’ll admit it: I’m an excitable guy. There are lots of areas and things about the stock market that I find fascinating and that can get my gears spinning.

But of all the things I love about the stock market, perhaps my three favorite things are insider incentives (so much so that I just finished a whole 12-part series on the corporate dark arts insiders can use to enrich themselves when their stock is cheap!), quirky situations, and the Liberty complex.

So, try as I might, I just couldn’t hold off on writing about the current quirky situation that’s happening over at LILAK. It’s just too fascinating not to! The setup involves an abandoned related party deal, a distribution of preferred stock, some massive insider buying.... and an eerie rhyme with a Malone deal that just ended in bankruptcy court. On top of the fascinating setup, I think the LILAK situation raises some interesting questions. Namely, if insiders have been consistently bullish and wrong for years, is there ever a time you can trust their bullish signals?

But I’m getting ahead of myself with that question. Let’s rewind and set the stage for the situation.

The LILAK story itself dates back years. It’s one of the greatest widow makers / fund killers of small cap value and event investors over the past two decades. I know it seems crazy to say now given what the stocks have done over the past five years, but investors used to like both the cable business model and John Malone. LILAK offered investors a pure play on emerging markets telecom in a John Malone vehicle with a long growth runway. On top of all that…. LILAK was a spinoff! Toss all of that together and it seemed like a no-brainer idea at the time; instead, it’s been a complete death trap.

But I’ll refer you to some past writing for more background. For the purposes of this post, the story starts in early May. That’s when GCI Liberty (another Malone vehicle!) announced plans to buy >$100m in LILAK stock (~6% of the company) from Searchlight for $8.63/share. In addition, GCI was in “good faith” discussions to exchange Malone’s LILAK shares (including the super voting class B shares Malone owned) for GCI common stock.

This was an insane transaction on a host of levels. To start, let me just show you a map:

Who looks at that map and thinks a merger is a good idea (even ignoring the cross border complexities)?

But, on top of the obvious lack of geographic fit, the deal itself carried several issues. First, GCI was buying a huge slug of stock from Searchlight for $8.63/share. The (potential) transaction was announced on May 6th, when LILAK’s stock was trading ~$8/share. Generally, a seller with a block that big of non-voting stock would need to take a big discount to unload it. Why was GCI instead paying a premium to buy out a block of non-voting (or low vote) shares from Searchlight?

Then there was the Malone factor of the whole thing. Malone controls both LILAK and GCI; I’m not sure how shareholders could look at GCI paying a premium to take out Searchlight, see Malone negotiating directly with GCI to swap stock, and think that GCI would get the better side of whatever deal was struck. It’s worth noting that one of the original sins of LILAK was buying CWC at a big multiple in 2016; Malone was on both sides of that transaction too, and it’d result in LILAK taking hundreds of millions of impairments on the acquired assets over the next few years.

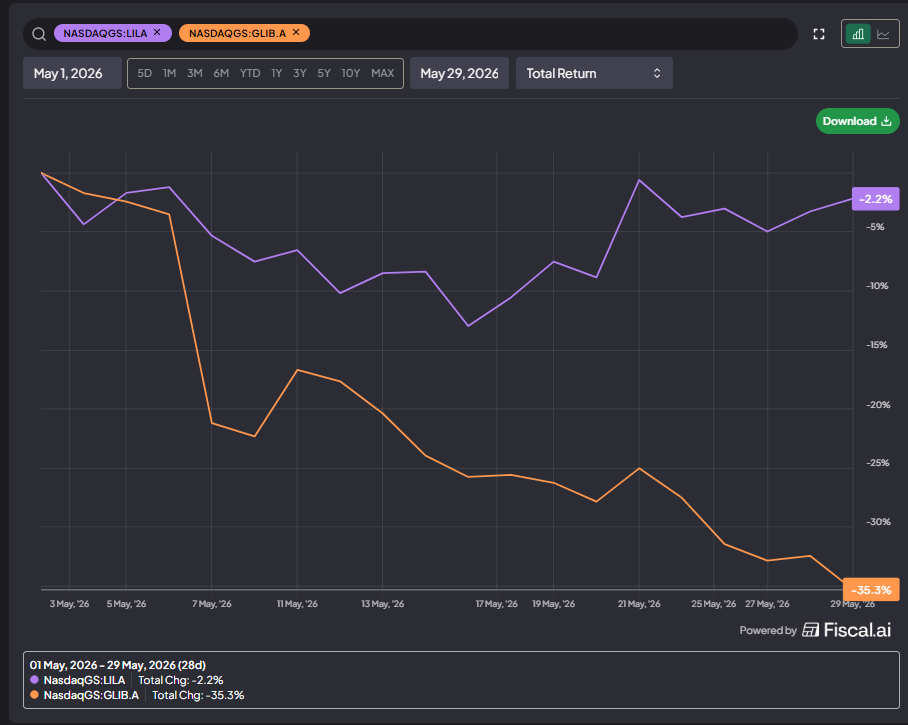

There were some other issues with the deal, but those were the major ones. And the market instantly hated the deal; GCI stock was down ~35% on the month… and that’s despite GCI cancelling the whole transaction a few days later.

Here’s where things get interesting; again, the market hated the GCI / LILAK deal, so a few days later GCI reverses it completely by selling the LILAK shares they purchased from Searchlight to Malone at the same price they paid for them. No harm, no foul I suppose (other than the fact GCI investors now aren’t sure if they can trust the company and the stock is down more than a third!).

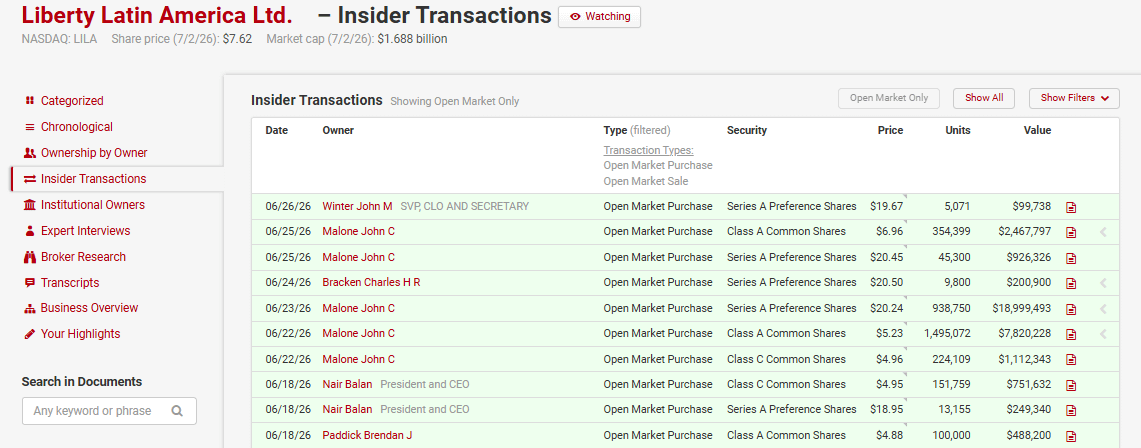

Now, alongside the announcement of the GCI deal (and their Q1 earnings), LILAK had announced an intention to distribute a set of preferred stock to shareholders. A week after the GCI deal was reversed, LILAK confirmed they were dividending out pref shares and noted that all of their key execs (Malone, Exec Chair Mike Fries, CEO Balan Nair) intended to be long term shareholders of the preferred stock. The prefs were officially paid out on June 17th.

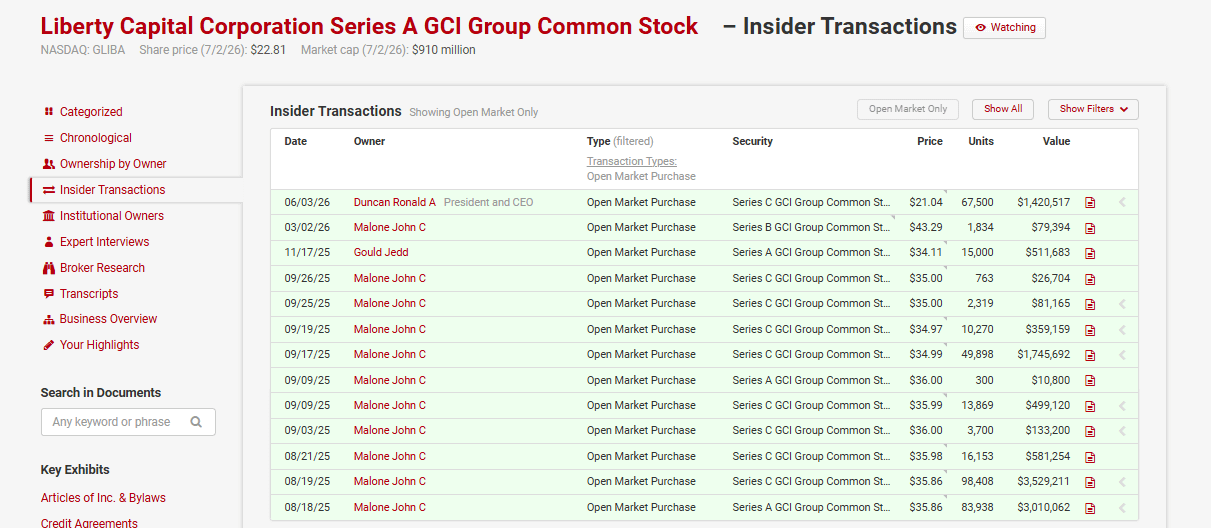

The next day, LILAK’s CEO spends ~$1m buying both common and preferred stock. A director joins him with a ~$500k buy. The next week, another director buys $200k of stock, and John Malone buys >$10m of common plus >$20m of preferred stock. The whole thing wraps up with the CLO buying ~$100k of prefs:

That is a wild amount of insider buying, and the excitement has driven LILAK’s stock much higher. LILAK closed yesterday at ~$7.62/share…. it closed at $7.79/share on June 16th, so the stock today is trading at basically the same price it was trading before it paid out $2.50/share in preferred stock. That’s a massive rerating in a few weeks. There’s been no fundamental news or anything; just a little financial engineering and some insider buying have sent the stock screaming higher.

Ok, that’s the setup. Now here’s what I think is interesting.

First, I’d note that Malone’s recent history of financial engineering is, to put it kindly, disastrous. I won’t detail all of the issues here, but I will call out one specific one: the LILAK deal today almost perfectly mirrors what QRTEA did in late 2020, right down to the quote in the PR from John Malone (and Greg Maffei) indicating “their intention to be long-term holders of the preferred.” Not only did that bit of financial engineering end poorly for QRTEA, but it carries a massive warning for the LILAK preferreds: QRTEA preferreds sued the bankruptcy estate for stripping them of assets almost the exact same day LILAK announced the preferred distribution. Caveat emptor indeed!

But what’s more interesting to note is the signaling here. The market is clearly rerating LILAK up because it sees the massive insider buying and thinks it’s a bullish signal. And that is probably correct; insiders only buy this much stock if they think it’s going up…. but I will note that the same insiders on this buying spree have an awful track record of insider buys over the past decade, and that this whole GCI / LILAK merger saga started because Searchlight (who had been an investor here for over a decade) had their founding partner resign from LILAK’s board and then sold all of their stock.

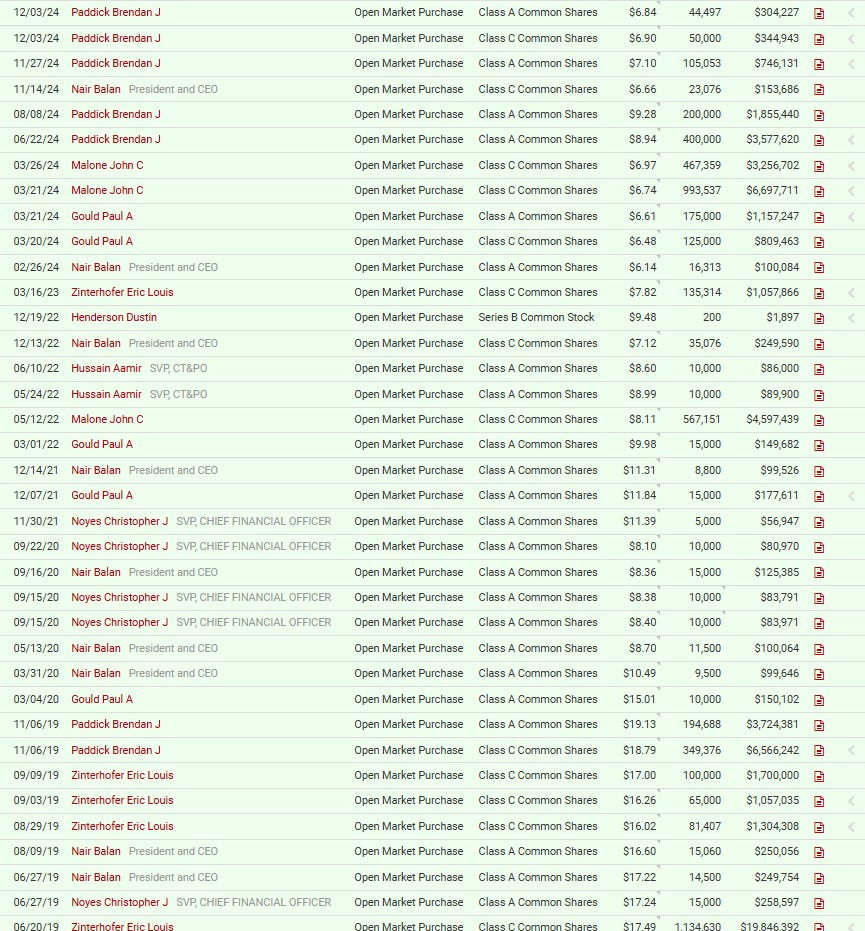

The Searchlight side probably speaks for itself, so let’s dive into the insider buying. Here is a non-exhaustive list of insider purchases at LILAK:

Again, that list is non-exhaustive. Insiders here have been consistently bullish on LILAK, and they have been consistently wrong. Just to single one out: Brendan Paddick bought ~$500k of LILAK shares after the pref distribution. He bought over $7m of stock in 2024 (average price >$9/share), and he swung for over $10m of stock in November 2019 (average price ~$19/share). All of those purchases were clearly misguided…. so is the third time really the charm here?

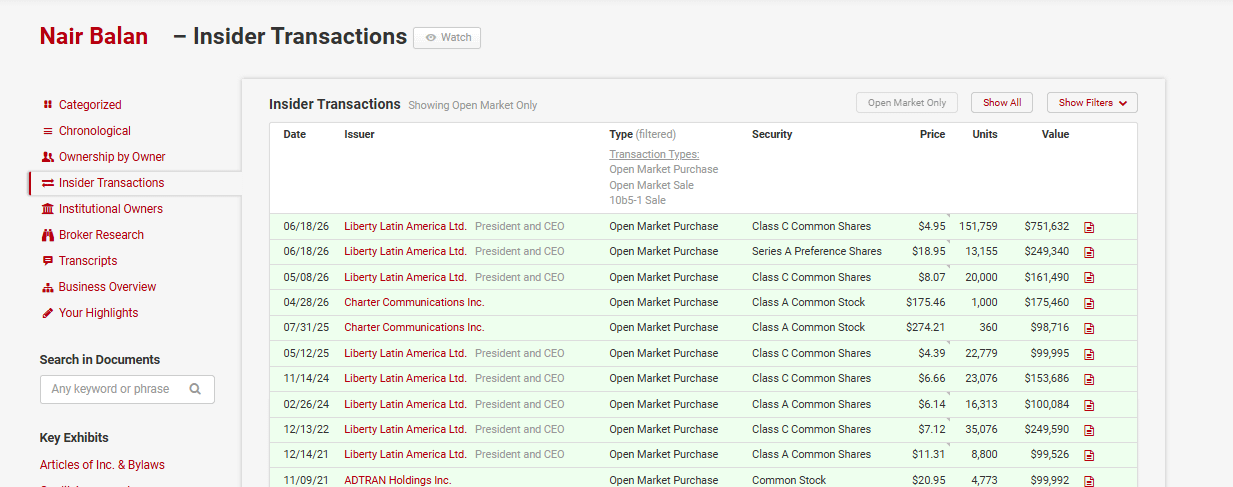

Here’s another interesting question: if we’re going to use the LILAK purchases as signaling, should that apply to other companies insiders here are involved in? Balan Nair (LILAK’s CEO) bought a bunch of LILAK recently….. he also bought a bunch of Charter (where he serves on the board and clearly has deep ties given the Malone and Searchlight relationships) recently. Does that Charter purchase have signal value? Or is Balan just a hopeless cable bull who is overvaluing the whole sector (and I say this as a beaten cable bull myself)?

Heck, it might be worth asking: is Balan someone we should even be following? Perhaps he’s a good operator (though his performance at LILAK suggests that might be a stretch), but he’s been filing Form 4s for almost 20 years thanks to his directorship at ADTN (here’s his first Form 4, a small open market purchase in June 2007). Incredibly, I count 24 open market purchases from Balan over the past ~20 years. He is underwater on all but a handful of them, and all of them have massively underperformed the stock market (for example, he’s up ~30% on this purchase of ADTN at $9.19 from November 2019, but given the S&P is up ~175% in total return over that time I think it’s fair to say that wasn’t a great purchase). It’s almost impressive how badly his open market purchases have performed.

Anyway, I have no real dog in this fight (though you can probably tell the shine has really come off Liberty and late stage Malone for me over the past few years!). But it’s a fascinating and strange situation (the exact type I love), and I do find it kind of incredible that the market is so quick to reward this financial engineering (which I view as extraordinarily low quality) and this aggressive insider buying (which is a real signal, but comes from people with an awful track record).

PS- speaking of misguided insider purchases, it’s probably worth noting that GCI (the company that was going to buy the Searchlight LILAK stake) has seen a spate of insider buying. Malone bought a ton, another insider joined him in November, and I believe they all participated in the rights offering at $27.20/share in late November. With GCI currently in the low $20s, all of those buys are underwater as well!