Five Weird Market Situations Worth Watching ($BRR $CAR $PAR $SSII $VELO)

It’s kind of trite to say “markets are volatile right now.” Honestly, when are markets ever not volatile? There’s always some big worry / concern in the marketplace….. that said, between bombing Iran and the SaaSpocalypse, markets feel particularly volatile right now.

One fun thing about volatile markets is that they tend to throw off a lot of weird / quirky situations. Again, there are always weird situations out there, but volatile markets tend to spur more weird situations on both the upside and downside. Why? On the upside, volatility can turn assets that were formerly worthless into very valuable gems1, and a company might be tempted to do some type of creative transaction to quickly monetize or realize that windfall. On the downside, volatile markets can create stress and push companies to the brink, and they may be tempted to turn to creative structures or events to stave off bankruptcy or to protect at least some value for equity holders.

With those volatile markets in mind, I’ve got five situations that popped in the past few weeks that made me go “hmmm…. that’s interesting.” No position in any of them currently, but I figured I’d throw them out there with a note: if you’re following any of these situations, or have seen any other deals worth tracking, don’t hesitate to drop them in the comments or shoot me a note. Heck, if enough people reach out with interesting situations, maybe I’ll do a follow up highlighting some of them.

The five situations are (in alphabetical order)

BRR’s questionable merger / activism

CAR’s aggressive insider buying

PAR’s strange use of proceeds

SSII’s wild stock raise

VELO’s refinancing and insider confidence

Let’s dive in

BRR’s merger / activism

BRR is a BTC digital treasury company. They were formed from a SPAC at the height of the digital treasury boom, though I’d note that the way the deal was structured was particularly unfair to minority SPAC shareholders IMO2. I do not say that lightly; both SPACs and digital treasury companies have made a habit of offering plum deals to private capital / taking advantage of outside shareholders, so for me to say this deal was “particularly unfair” speaks to just how one sided I believe the structure was.

Like most digital treasury companies (disclosure: I’m a long time digital treasury skeptic, so feel free to note my bias when talking about these), BRR’s goal was to trade for a premium to their digital assets so they could do the perpetual motion machine of issuing shares at a premium to NAV, buying more “digital treasury”, perhaps seeing their buys push the price of digital asset up, having the combo of issuing stock at a premium + pushing the digital treasury up increase their NAV, and so on. That dream has not happened; BRR has consistently traded for a large discount to NAV since deSPACing. BRR has responded to that discount by repurchasing shares at a discount to NAV, which is very good capital allocation. However, BRR clearly wants to be a meme stock and knows they need to appeal to a retail base to get there, so for a while they were PR’ing their buybacks daily with headlines like, “ProCap Financial’s Feeding Frenzy Continues with Additional Share Repurchases” and “ProCap Financial Continues to Gobble up Shares at a Discount to NAV.”

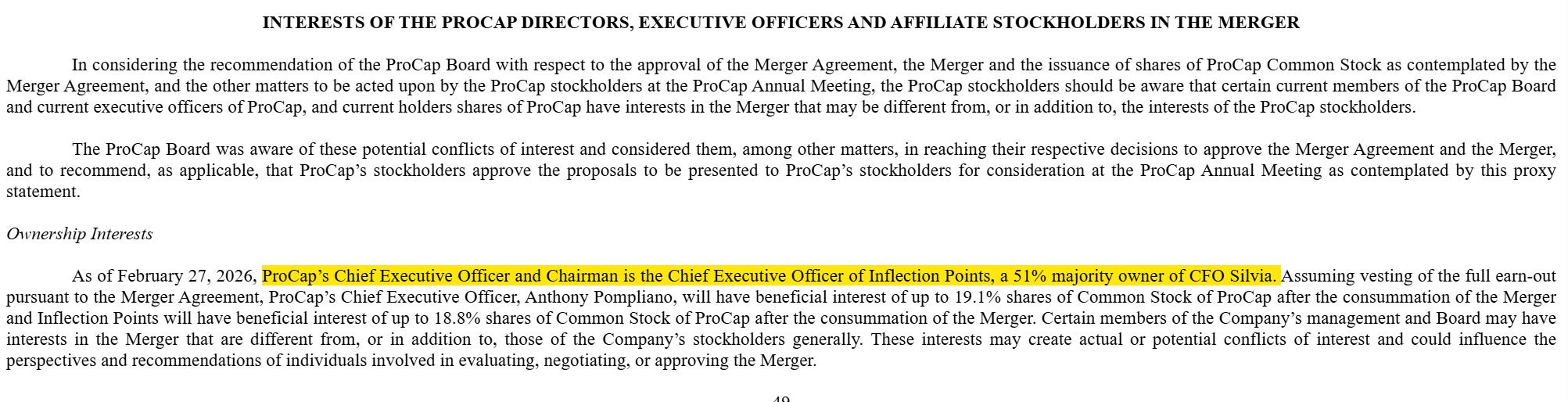

Anyway, I think that background is all helpful here, but none of it relates to the weird situation here. The weird situation is that in early February, BRR announced a deal to acquire CFO Silvia in an all stock transaction.

What’s so weird about that?

Well, to start, I’d encourage you to read the press release. I probably read 1,000 merger press releases a year; I’d venture the BRR / CFO Silvia merger PR is the strangest I’ve ever read. It reads like an advertisement for the CFO Silvia product, and while it mentions that BRR and CFO Silvia are merging, it does not give the terms of the merger! It doesn’t say the valuation of CFO Silvia, it doesn’t say what their financials look like, and it doesn’t even give the specific amount of shares that CFO Silvia is getting in the deal!

It’s also just a strange deal in general. BRR is a digital treasury company trading at a discount to NAV; why should they be issuing stock to buy an AI play?

But what’s even stranger is that the merger proxy reveals that BRR’s CEO is the majority stock holder in CFO Silvia, and that information wasn’t even disclosed in the deal announcement. Seems kind of pertinent, no?

There’s actually a ton of other crazy stuff in this merger. The one that jumped out to me looking through the proxy was the fairness opinion; I really wanted to look and see the projections for both sides of the deal, but the fairness opinion basically reads “the vibes of this deal seem fine; go get it my dudes” and skips out on all basic analysis. ATG is pushing back against the deal and published a PR highlighting that issue and plenty of others; I’ll refer you to their PR if you want more on how wild this deal is.

CAR’s aggressive insider buying

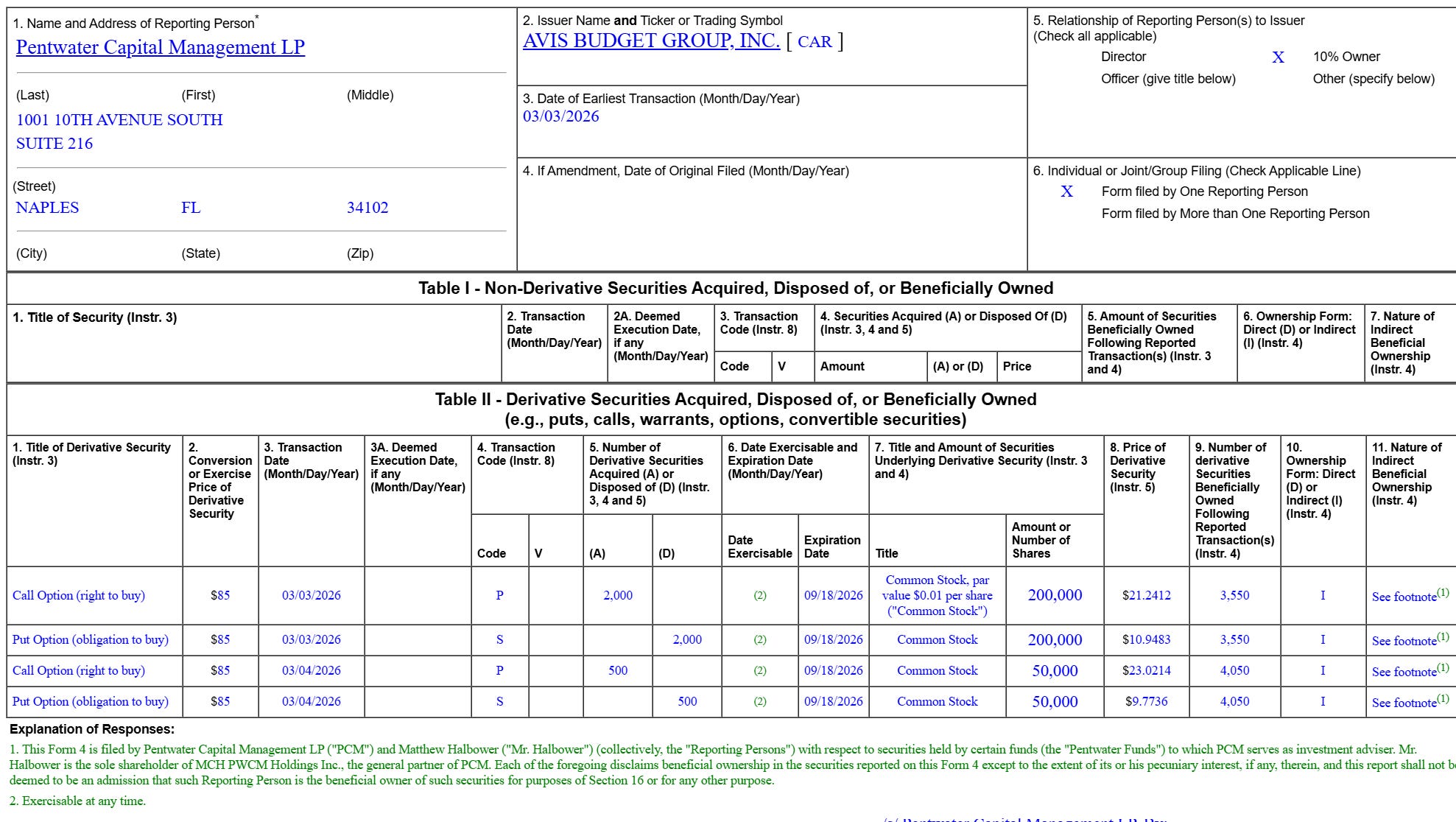

Full disclosure here: I do not know Pentwater, but I have a ton of respect for them. Every time I’ve been in a position that overlaps with them, I’ve been impressed with the depth of their work and thought process when I’ve heard them speak about it. So I like to follow their 13-Fs / buying.

Recently, Pentwater has been aggressively buying Avis (CAR). But it’s not the buying itself that’s interesting; it’s how they’re doing it. Consider this form 4:

CAR’s stock has been trading for ~$95/share for most of this month. For some reason, Pentwater has decided a synthetic long (buying a call and selling a put at the same strike) is a better way to increase exposure than simply buying the stock. I’m sure Pentwater is a lot smarter than me and there’s a reason they chose that specific structure to increase their exposure to the stock…. but I’d be remiss if I didn’t note that CAR is a very tightly held stock as SRS and Pentwater now hold >60% of the stock between them.

Bloomberg tells me almost 50% of CAR’s free float is sold short; could Pentwater’s synthetic long create some fireworks (read: short squeeze) once they take delivery? And, on a fundamental level, it’s been a rough few years for rental cars…. is Pentwater seeing something in the data that suggests the capital cycle is about to turn? The combo of tightly held + lots of short interest + trough-ish cycle + a history of aggressive capital return from CAR could cause things to get spicy very quickly….

PAR’s strange use of proceeds

PAR is a favorite of a lot of GARP-y investors, and I have a lot of friends who I respect who are long the stock and I think have done really good field work on it. It has not been a great year for the stock; it’s down ~75%.

Some of that drawdown is clearly macro / market related (PAR is a payments / SaaS company, which is about as close to in the crosshairs of the SaaSpocalypse as you can get), but PAR really hasn’t done themselves any favors over the past year. That was capped off last week when PAR announced a convert deal with the stock hovering near all-time lows.

The convert deal itself was obviously ill-timed / not great for shareholders3, but the real kick in the teeth is the use of proceeds. PAR disclosed they’d “agreed to repurchase approximately 2.09 million shares of common stock from purchasers of Notes in privately negotiated transactions effected with or through one or more affiliates of the initial purchasers, at a purchase price per share equal to the last reported sale price of $15.85 per share.”

That’s an insane use of proceeds for three reasons. First, it’s a gift to the selling shareholders at the expense of everyone else. The stock fell from $15.85 to <$13 overnight on the convert announcement (before bouncing back to close at just under $15/share); buying back stock at $15.85 helps hand picked shareholders avoid a loss and swap into a better security. Why give those shareholders a special deal?

Second, it’s just kind of a strange deal to raise ~$250m of converts and say “hey, we’re using ~15% of this deal to buyback stock from selected shareholders who will then buy the converts.”

Finally, a big part of the bull argument was basically that PAR’s CEO was an outsider. He was on Invest Like the Best as “the Berkshire of Software,” and most bulls would talk about him being “thoughtful about capital allocation” (from this trata interview)4 and as one of the reasons to be bullish the stock. It’s hard to look at him in a very positive light now: his largest shareholder published a letter suggesting the company should go private, and he responded a week later with a convert deal (which would make a take private deal much more expensive) with a large piece of the proceeds going to buyout select shareholders. Woof.

Perhaps there’s some magic rainbow at the end of the PAR tunnel. I actually am travelling to New Orleans right now and just bought a smoothie and noticed the payment app was a PAR terminal, so there is a real business here. But everything about this convert deal does not look pretty from the outside looking in…

SSII’s wild stock raise

SSII had one of the most interesting raises I’ve ever seen earlier this month. They raised $18.6m from two different sets of investors:

Three insiders (the Chair / CEO, Vice Chair, and a director) bought ~$5.2m of stock at $4/share

External investors bought $13.4m of stock at $3/share.

However, the external investors could be further segmented, as one of the investors who invested ~$2.5m was brought in by a “FINRA member”, and SSII paid the FINRA member a 7% commission ($175k) plus issued them ~42k 5 year warrants to buy SSI stock at $3.45/share. In 2024, SSI assumed ~25% volatility for their stock options; that seems low to me, but if we use that on the warrants SSII issued they’re worth another ~$100k. So I think you could argue SSII paid ~$275k all in for that $2.5m investment, and thus the net price to them was closer to $2.60/share.

So you’ve got one raise that has three wildly different prices:

SSII got $4/share from insiders

SSII got $3/share from most outsiders

SSII got ~$2.60/share from outsiders brought in by the FINRA firm after you account for fees.

In one transaction, SSII’s stock was worth >50% more from one set of buyers than from another. Crazy!

VELO’s refinancing and insider confidence

VELO has had a rough go of it. They announced a SPAC merger right at the height of the SPAC bubble in early 2021 projecting half a billion in revenue in 2025. Revenues for the first nine months of 2025 were ~$36m; I suppose it’s possible they had a massive Q4 and hit those projections, but I think it’s safe to say the company hasn’t exactly lived up to its SPAC promise.

However, just because a company has been a disappointment in the past does not mean the stock can’t do well going forward (at least that’s what I tell myself about at least half of my portfolio), and VELO’s insiders certainly seem somewhat bullish. VELO’s recently retired most of their debt by converting it to equity. A debt to equity conversion is not abnormal; what is abnormal is that Velo did the conversion with insiders and did it at two different prices. One director owned ~$10m of notes and converted at $10.50/share (roughly the market price of the stock), while the CEO went out at bought $5m of notes and then converted it to equity at $16.38/share.

That is a fascinating transaction; I’d be really curious how the CEO came up with the $16.38/share number. Whatever the reason, you have to think the CEO is bullish on the company’s stock to make that switch at that premium (and the CEO would be happy to tell you he’s bullish; as part of the PR he noted, “My decision to acquire and convert this debt at a significant premium to market reflects my belief in the long-term value of Velo3D,").

One last note on VELO: in February, the CEO got a stock option grant that doesn’t kick in on the low end until the company hits a $1B valuation and, on the high end, until the company hits a $10B valuation.

A cynic might note that hitting a valuation target isn’t necessarily hard if a company issues enough stock or goes ham on stock-for-stock acquisitions…. but that’s a story for another post. What’s important for this post is that a director converting debt to equity is already bullish…. but a CEO then buying debt and converting it to equity at a massive premium is so wildly bullish you wonder if it’s setting something else up…..

Wrapping it up

None of these situations are necessarily investable yet…. but most of them show some signs of the potential for a rapid rerating / interesting catalyst in the near term, so I think these are exactly the types of set ups that are worth monitoring, as they could get interesting in a hurry.

PS- Will once again note: if you’re tracking any weird deals or odd financings lately, send them my way (either in comments or email). If I get enough interesting ones, I’ll do a follow-up post highlighting the best ones.

An example might show this best: consider an oil producer with some debt and a breakeven cost of ~$70/barrel. A month ago, oil was trading <$70, so they company was probably worthless. Today, with oil touching $100 and the whole curve rising, that company suddenly finds themselves very in the money.

Ok, that might be a little unfair. Just because a stock is down doesn’t mean that a convert issuance or stock issuance is bad for shareholders; if the use of proceeds creates value, even a stock down 99% can issue shares and be value accrettive. I guess I’m more suggesting that given how rapidly the stock has fallen, you could certainly forgive shareholders for wondering why the company chose this specific moment to issue a convert.

Obviously I’m biased as I’m a big fan of trata, but it is really interesting to see bulls and bears talking about their thesis and go kind of spot check it with the benefit of hindsight!

Thank you for a well researched article

Andrew what do you think of Sieya Lu’s work on PAR?