Buying reputations, weird tenders, and big insider buys: $TTD and $WIX

Obviously, the world is awash in news right now…. but it’s not just an interesting time for the world at large; the past 24 hours have been filled with interesting news in my very narrow interest circle of big insider buys / the SaaSpocalypse / curious repurchases.

While there has been some other news in this area, the two headliners here are the ones that I find really titillating. They are:

Alongside their earnings report, WIX announced a $250m investment from Durable Partners; they followed that up by announcing a $1.75b tender offer the next day.

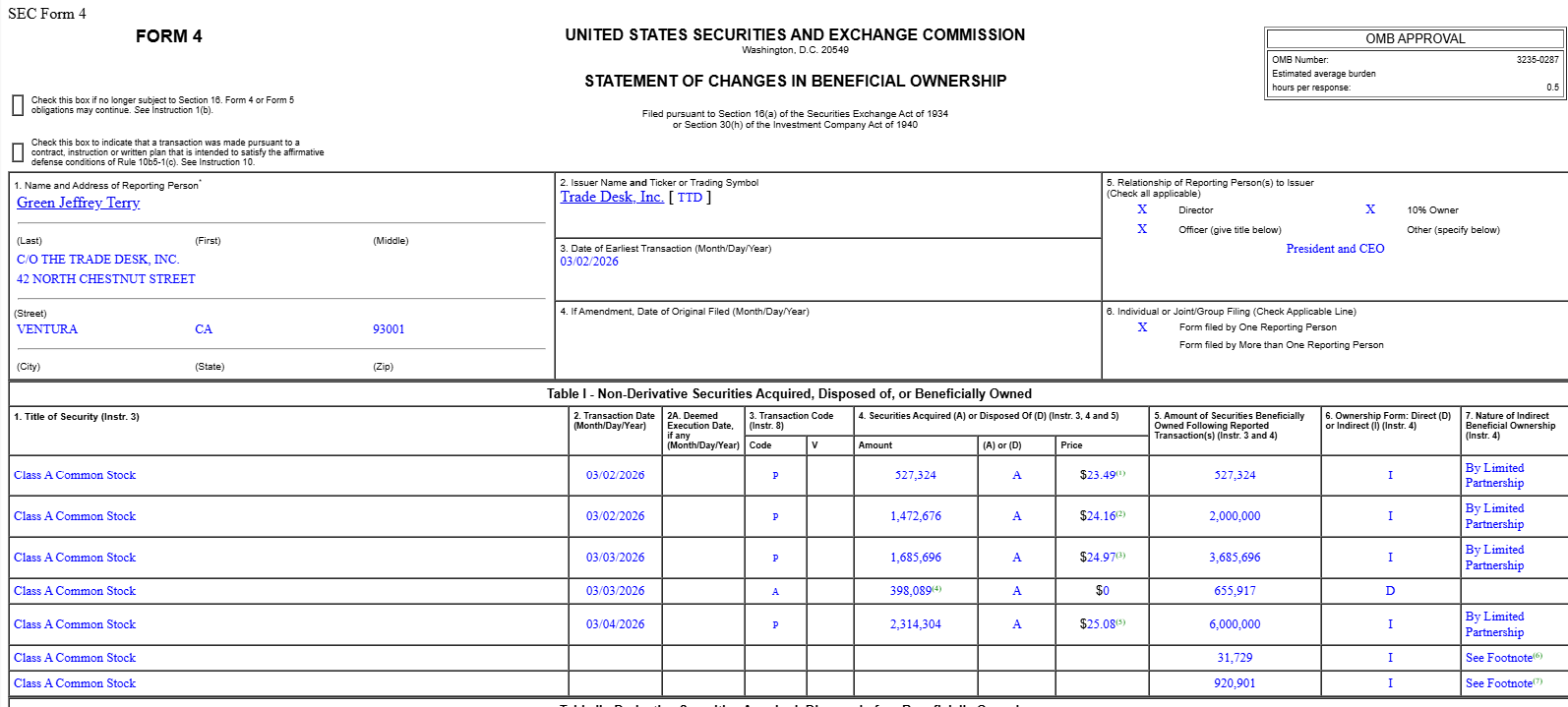

TTD’s CEO bought just shy of $150m of stock on the open market over the course of three days at the start of March:

I find both of those transactions fascinating and, to be blunt, somewhat questionable. Let’s dive in.

WIX’s “brand halo” investment and subsequent tender

We’ll start with WIX. WIX is a company I’ve thought about a lot over the past few months; they seem squarely at the center of the current SaaS / AI fears, and I recently used their base44 product to make an app (actually, at this point I’ve made several!). But, as mentioned above, the reason I’m writing about them is because, alongside their earnings report, WIX announced a $250m investment from Durable Partners, and they followed that investment up by announcing a $1.75b tender offer the next day.

I can’t tell you how crazy that series of events is. To me, it’s an enormous red flag and kind of appalling to be honest. Perhaps I’m missing something here, but when I saw that sequence, I actually wrote down “I will never buy this company” in my internal WIX notes.

Why do I find the sequence so appalling / questionable?

Per the 6-k, the Durable investment is structured as a unit. Durable buys WIX shares at a 5% discount to the market price; in addition, for every four shares Durable buys, they are given one warrant to buy WIX stock with a strike price 25% above WIX’s market price.

This type of “buy stock at a discount; get some warrants free” structured investment is an absolute gift for the buyer. If you’re ever offered those terms, you should probably take them in as large of a size as you possibly can (while, of course, remembering this is not investment advice and probably asking yourself “why is the company offering me specifically this deal”?). Why take that deal? Because it’s free money! There are generally some restrictions to doing this, but Durable could have immediately sold all of their stock for a small profit1 and created an enormously valuable warrant position for free. I’m sure they didn’t do this, but I highlight that “more than free warrant” trade just to show how good the investment was for the buyers.

Why would a company give so much value away to a buyer? In general, companies do these type of deals with buyers who have a really good reputation. In effect, the company “buying reputation” and paying the buyer for the use of their reputation; the company knows that by bringing a high profile investor into the fold, other investors will feel more comfortable buying the stock and the company will thus lower their own cost of capital. The most famous of these deals is probably Buffett’s investment into Goldman at the height of the financial crisis (which he later basically replicated with Bank of America). It’s a truly perfect reputational buying deal; Buffett made a fortune off the Goldman investment, but Goldman got a great deal too because Buffett’s presence gave investors faith Goldman would make it through the crisis and lowered Goldman’s cost of capital on a whole host of levels.

But comparing Buffett’s investment in the banks to Durable’s investment in WIX shows why WIX is on my “no go” list now. Banks have this well known problem where they are exposed to bank runs; getting Buffett in the cap structure significantly reduced the risk of a bank run and reduced the rate that the banks could tap other sources of capital. Thus, while the banks gave Buffett “free” money, the banks in turn had significant financial benefits from the Buffett brand.

In contrast, WIX is not a bank. They are not subject to bank runs. Yes, bringing Durable in gave them a brand halo that likely made other investors more confident in WIX’s future and probably raised the stock price….. but why did WIX need a brand halo for their stock price? In fact, given they were about to announce a massive tender offer, why did they want their stock price up? Wouldn’t shareholders have been better served with WIX having some more doubters and a lower stock price, so that the current tender could vacuum up more shares?

If you're about to run a $1.75b tender offer, shouldn’t you want your stock price to be lower?

It’s an absolutely wonderful investment for Durable…. but it’s a baffling display of incompetence by WIX in my opinion.

TTD’s massive insider buys (and MNPI questions)

I’m certainly far from the only one to note this, but TTD’s CEO bought just shy of $150m of stock on the open market over the course of three days at the start of March:

It sounds crazy to say this about a ~$150m buy…. but I think that filing is actually even more bullish than it appears at first blush. Why? Two reasons:

Size: Yes, we all know $150m is a big insider buy…. but I don’t think you realize just how big this buy is until you put it into perspective. Last summer, I went looking for big insider buys. The biggest of all time is Elon’s $1b Tesla buy, and the second largest of all time was Harold Hamm’s ~$200m purchase of CLR in the COVID doldrums. TTD’s $150m insider buy is thus the third largest insider buy in history (or at least that I can find)…. and it’s worth noting that the largest and second largest have been absolutely home runs, with one of them (CLR) being done during an effective crisis (I’d argue TTD / SaaS in general is in an AI driven crisis right now!). I’d suggest the base rate on TTD post this buy is it works out pretty damn well.

Off-cycle grant snuck in? If you look at the bottom of that form 4, it discloses that the company also gave him 920k options alongside those buys. I believe that option grant is quite off-cycle, as his options were granted in April 2025. I’ll leave further sleuthing on option timing for TTD to someone else, but I will just note that a CEO buying $150m of stock and getting almost 1m options granted at the same time is about as much of a “call your bottom” trade as I can imagine.

There are two other interesting pieces to the TTD buy that I did want to note.

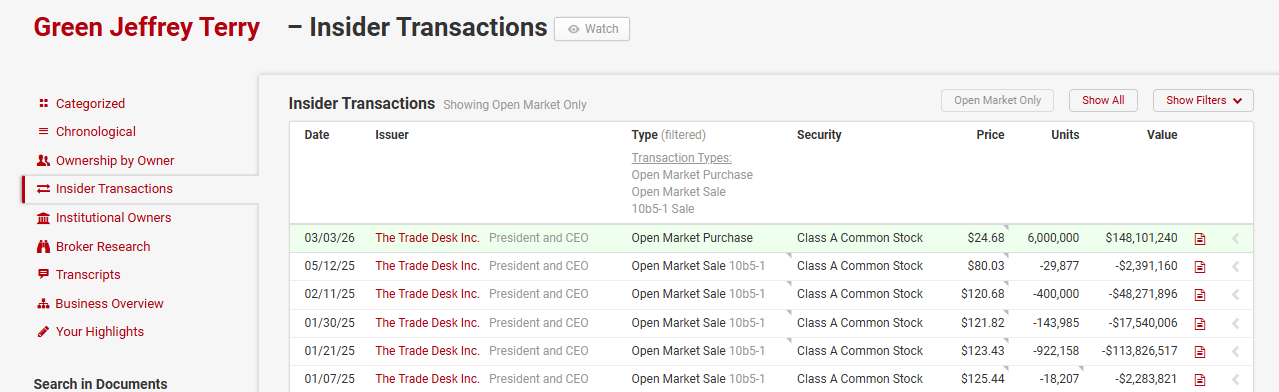

First, while a buy this size is unabashedly bullish, it is perhaps worth noting that TTD’s CEO did sell >$180m of stock across a handful of transactions in early 2025 when the stock was trading for ~$120/share.

Honestly, I’m not even mad, I’m impressed! The fact that he sold so much when the shares were flying might give even more signal value to the current buys.

Second, TTD’s stock is screaming higher (>+25%) as I write this article. That’s probably largely driven by the huge insider buy… but I’d suggest it’s also partly driven by The Information reporting that OpenAI reached out to TTD about selling ads.

Here’s my question: if TTD’s stock has been melting down because of AI fears, and the CEO knows that an AI company has reached out about an ad partnership….. how is that reach out not MNPI that would put the company into a blackout window?

Perhaps the answer is the reach out is too early stage to mean anything. Perhaps it’s not a big partnership. Perhaps the article isn’t even real. I have no idea. And I’m sure an insider buy this big was run by a lot of internal compliance before they blessed the trade.

But the timing of getting literally the third largest insider buy of all time done right before leaks of this massive partnership that addresses a lot of the current bear case on the company comes out seems strange to me.

Note they don’t have to sell the stock. A clever bank could have designed some derivative trade that basically did the same thing.

I was looking into TTD in early February but got hung up with the CEO offloading a substantial chunk of stock all the way up until the day before the company was set to announce that they missed revenue projections for the first time ever. The stock subsequently declined over 30% and a class action lawsuit was filed on 2/19/25. The suit is still pending a motion to dismiss from TTD last I checked. There’s also the bizarre circumstances surrounding the ongoing CFO turnover saga, which maybe isn’t a big deal alone but combined with the fortuitously timed stock sale raises a red flag for me. Went back and forth on this a lot though because if there’s no there there then the stock is definitely undervalued.

A month later...TTD's stock price is down ~27%. Insider buying may not always be great signals. One could argue that TTD is a deep value play. Since it's a SaaS business --- I don't know personally since I've never looked at TTD --- it has all deferred revenues that are really positive cash flows when calculating its valuation, it has XYZ value that is unlocked. I don't know what the deferred revenue-adjusted free cash flow looks like, but it still may not be cheap at this point.