A Sinister Raise, a Bitter Press Release, and Five Other Weird SEC Filings

Earlier this month, I posted “Five Weird Market Situations Worth Watching ($BRR $CAR $PAR $SSII $VELO).” The response to that article was really fun; I had excellent conversations with knowledgeable shareholders on several of those companies.

I spend most of my day trolling through SEC filings anyway, so given the response to that post (and the resulting steady stream of idea flow) I’m going to turn it into a monthly series. The goal isn’t necessarily to cover the absolute weirdest filings I see; it’s to cover the ones that are interesting, thought-provoking, and (ideally) at least a little weird.

So here are the seven filings that made me stop and think this month (and, as always, my DMs are open if there’s a filing that you think is interesting and would fit well into this series! Quality inbounds help make this series better!):

EMPD’s wild (and sinister!) raise

BNTX backs its founders

You’re probably not grinding hard enough (SMCI’s new compliance officer)

UWMC’s a bitter loser:

WATT is here to dilute shareholders and take names

Some big buys in SaaS-land

Across the board insider buying at BDCs (including one BDC where almost literally every insider (but one) bought stock on the open market)

Let’s dive in:

EMPD’s wild (and sinister!) raise

Last year, I wrote about a very creative financing from IONQ. The company’s volatility was off the charts, and they found a way to monetize that volatility by selling stock in a private placement at a ~20% premium to market prices. Why would anyone buy stock at a premium to market prices? Because IONQ gave the buyer massive warrant coverage, and those warrants had huge value thanks to IONQ’s huge volatility.

That trade has probably worked out well for both sides1: IONQ managed to raise a slug of capital at an attractive price while their stock was still flying high (it’s down ~50% over the past six months since the raise), and given IONQ’s vol and trading volume I would be shocked if the buyers of that private placement didn’t turn a massive profit.

This month, EMPD did a similar raise to IONQ…. but EMPD’s was much more sinister.

EMPD is a digital treasury company focused on Bitcoin. Like most digital treasury companies, they’ve traded for a discount to NAV basically this entire year; for most of the past month, they’ve been trading around 80-90% of NAV (you can see a real time NAV calc here).

Towards the end of March, the company announced a $25m equity raise. The raise was priced at a premium to both NAV (it priced at 103% of NAV) and the market price (again, the company trades for <90% of NAV); on top of that premium raise, the company noted they’d continued to buy back stock at a discount to NAV. Read that sentence again: a company trading at a discount is buying back shares and somehow raising capital at a premium to NAV? Nirvana for shareholders, right!?!?!

Au contraire, mon frère!

EMPD didn’t just issue stock in the equity raise; for every share they issued, they gave the buyer a four year warrant struck at $6.27/share (~20% above NAV). Those warrants have enormous value; BTC currently trades with ~50 vol. EMPD is a levered BTC treasury company, so it should have even more volatility than BTC (EMPD’s option chain is extremely thin but points to volatility well over 100). ChatGPT tells me that a four year warrant that’s 40% out of the money with 100 vol is worth ~65% of the spot price…. for EMPD, that means each warrant was worth ~$2.90/share. So, yes, the headline number EMPD raised at was $5.39/share, but if you adjust for the value of the warrant EMPD raised money at an effective price of ~$2.50/share while the stock was trading at ~$4.50/share. An absolutely awful trade2.

Why would EMPD raise money like this? Well, I’m not in the board room, so I can’t tell you with absolutely certainty…. but I’d suggest it’s likely a board entrenchment maneuver. EMPD is currently in a rarely seen double proxy fight where two separate shareholder groups3 are trying to replace the board with a more shareholder friendly group4. EMPD’s press release announcing the raise notes the raise was bought by a “current institutional investor” in EMPD; my guess is EMPD went to a big shareholder and said “hey, agree to keep the current board in place, and we’ll give you a big slug of stock to vote and toss in a ton of warrants to make the whole thing worth your while.” And, if you think EMPD (or any corporate board) is above shenanigans like that to keep themselves entrenched, I’d note that EMPD already appears to be pulling out all the stops to keep the activists from running.

Sinister…. but, heck, I’m not even mad. That’s amazing.

BNTX backs its founders

Biontech shareholders are no strangers to volatility. After IPO’ing in late 2019 for ~$15/ADS, BNTX became Pfizer’s partner on the COVID vaccine and saw their stock price peak over $400/share in late 2021. The stock quickly retreated from there; by mid 2022, it was trading for ~$125/ADS, and it’s generally chopped around that price in the years since (it opened the year at ~$105/share).

Today, BNTX has just shy of $20B in net cash, and while the COVID franchise is obviously dwindling the company has a ton of promising other drugs / readouts coming over the next few years….

Perhaps those readouts work, perhaps they don’t. I have no idea! But it’s a pretty promising set up…. which is why it’s so wild that BNTX announced that their co-Founders / top executives were leaving BNTX to start a “next-generation mRNA innovations” company. What’s even crazier is that BNTX will be contributing their mRNA assets to the new company!

Why is this so crazy? It’s absolutely ripe for conflicts of interest! BNTX could have spun out the mRNA assets to all their shareholders and put their founders / exec team in control of the new company. That would have been a fair and equitable way to do a start up. Instead, it seems BNTX will contribute the mRNA assets to the new company in exchange for a piece of that company. How are the mRNA assets going to get valued in that transaction? Given the founders / CEOs are going to the new company, it’s not hard to see how they might want to give the new company a boost by paying BNTX far under market value for the mRNA assets.

I’m sure the transaction will be heavily scrutinized by a host of lawyers and valuation experts…. but it’s just wild to me a company would choose to do a convoluted structured like this one instead of a simple (and fair) structure like a spin. In general, I’ve found when a company opts for a convoluted structure, it’s because someone is pulling a fast one… and that normally means management is benefitting at the expense of everyone else.

I’m not the only one who thought this was strange; BNTX is down ~20% over the past month, with the majority of the drop coming as the market reacted negatively to the management surprise.

You’re probably not grinding hard enough (SMCI’s new compliance officer)

SMCI hired a new compliance officer this month; I hope the compliance officer negotiated a big pay package, because they have their work cut out for them! Concurrently with the compliance officer getting hired, SMCI announced their co-founder had resigned from the board after being charged with smuggling billions in GPUs to China.

I don’t have crazy thoughts on this, but I did want to note two things:

It should come as a surprise to no one that SMCI is embroiled in some scandal. Remember, this is the company a few years ago that spurred the incredible WSJ headline “is anyone crazy enough to audit super micro computer”, and it doesn’t exactly take a forensic accountant to dig through their 10-K and find some very curious related party transactions….

This may be the funniest tweet of all time.

UWMC’s a bitter loser:

UWMC and TWO announced an all stock merger late last year. TWO shareholders would get 2.3328 shares of UWMC’s stock for each TWO share; at the time of announcement, that valued TWO at $11.94/share. TWO ended 2025 with a book value of $11.13/share, so the deal was priced at a slight premium to TWO’s book value.

UWMC’s stock has been in a meltdown of the past few months; it was trading >$5/share when the deal was announced in late December, but by mid-March it was <$4/share. Given UWMC’s stock move, the offer had gone from valuing TWO at a premium to book to a discount.

If you read TWO’s proxy, you could have seen that there was a lot of interest in buying TWO for just above book. If you were a TWO shareholder, you had to ask why you would vote for a deal with UWMC that was now selling TWO below book value when plenty of other parties seemed interested in buying TWO???

Sure enough, in mid-March, TWO had to delay their meeting as they didn’t have the votes to get it over the finish line. A few days later, they announced they’d gotten a superior proposal to buy the company for $10.70/share in cash. A few days after that, they deemed the first proposal superior and announced another proposal from a different buyer to buy TWO for $10.75/share. The bidding war eventually culminated with TWO breaking the UWMC deal to sell to CrossCountry for $10.80/share.

It’s a fascinating story (and illustrates one of my favorite set ups; all stock deals where the buyer’s stock falls precipitously and the seller is an in-demand strategic target. The combination often opens the doors for superior bids and/or the buyer topping up their offer. Kicking myself I missed this one).…. but none of that is why I’m writing TWO up!

I’m writing TWO up because, after learning they lost, UWMC published a fabulously bitter press release. I’ll quote the release in full.

The actions by TWO’s management and board do not reflect the best interests of their shareholders. The same team that had to settle a $375 million lawsuit this past summer is at it again. TWO’s decision appears to be driven more by ego, than by sound judgment. The deal for us was a strategy to acquire their servicing book, not their operations, as ultimately there are no operational efficiencies to gain — UWMs operations are best in class. Unlike TWO’s business, which is effectively a melting ice cube, we are in growth mode and will continue to be the market leader for the wholesale channel in support of our broker clients and team members.

Ten out of ten, no notes. That press release definitely does not make me think UWMC’s a bunch of whiny losers who I’d never want to invest with. The quote that TWO is a “melting ice cube” also does not make me wonder why UWMC was so eager to issue a bunch of stock to acquire it.

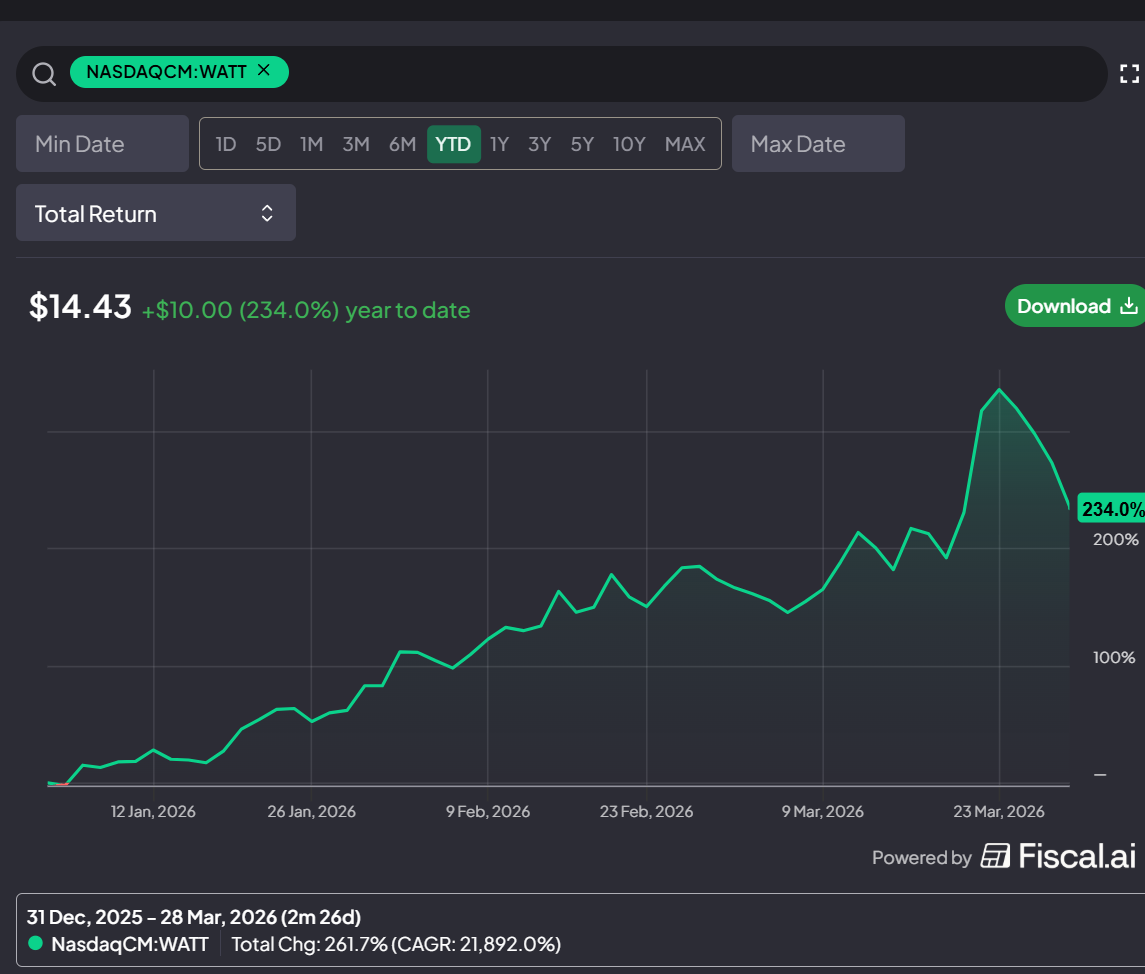

WATT is here to dilute shareholders and take names

WATT is a tiny little company that’s become an unexpected battleground stock. Some growth focused smaller cap investors did some sleuthing to uncover that the company likely had landed partnerships with Walmart and Amazon, and the potential sent the stock screaming higher so far this year.

The sudden rise attracted some short interest, who noted the company’s history of “broken promises” didn’t exactly scream world changing technology.

How it plays out is anyone’s guess and far beyond the scope of this post…. instead, my focus is on the dilution here. WATT filed their 10-K a few days ago, and I don’t think I’ve ever seen a company make such aggressive use of their ATM. In fact, I didn’t know that you could use an ATM this aggressively.

WATT ended 2025 with 2.2m shares outstanding. If you scroll down to their 10-K’s subsequent events, you’ll see the company issued ~3.3m shares through their ATM program YTD through March 23.

WATT diluted shareholders 150% inside of three months. Again, I didn’t even know that was possible with an ATM program!

Again, I don’t know how this turns out for shareholders, but a tip of a cap to the company for seizing the opportunity to raise cash when they needed it!

Some big buys in SaaS-land

I’ve written quite a bit about the SaaSpocalypse. To be honest, I haven’t really pulled the trigger on anything yet for two reasons:

I don’t think any of these are as cheap as the headline numbers suggest because the stock comp drag is both real and going to be a big issue to reset.

I don’t have a ton of confidence in the terminal value of these businesses. It’s crazy how quickly I’ve heard a shift in tones on calls with customers; people who three months ago were saying “there’s no way I’d ever trust AI to do that” are now saying “yeah, I’m 100% AI for that task.” When customers are changing their minds that quickly, how can you feel confident any company is safe?

Every company is putting on a brave face that they are an AI winner, but it’s not lost on me how fast CHGG got rug pulled and how over confident they were as it was happening (look at this quote from their Q3’23 earnings call, which they quickly followed up with a big accelerated buyback).

So I haven’t done anything in the space yet…. but one thing you really want to see to start building conviction that the space has bottomed / gotten oversold is insider buying and big share repurchases, and we are starting to see some of those (though they haven’t stemmed the bleeding so far!). The headliner here is probably Salesforce (CRM), which announced a $25B accelerated share repurchase (ASR). That’s the “largest-ever” ASR, and it “underscores leadership’s confidence in the company’s position in the Agentic Era” as well as retires just under 15% of the company’s shares. So that’s the headliner, but there are plenty of others. The most interesting one I’m following is probably Expensify (EXFY). The company bought back ~2% of their shares outstanding in November / December at prices >50% above the current share price….

Keep reading with a 7-day free trial

Subscribe to Yet Another Value Blog to keep reading this post and get 7 days of free access to the full post archives.