Weekend Thoughts: Sports Rights Tail Risks

A few weeks ago I put up a post on quirky tail risk bets. I got lots of ideas, both macro and sector specific, about tail risk bets on the heels of that post. While many are interesting, none of them have really “clicked” with me / I haven’t figured out a really advantaged trade to put any of them, so I haven’t really traded around any of them.

Still, the tail risks bets got me thinking, and given my permanent interest in sports teams and sports rights, I wanted to share my current favorite tail risk: what happens if we start seeing down rounds in sports rights? To be upfront, I’m not sure if there’s anything “actionable” in the public markets on this risk (though you could paint up some short scenarios for publicly traded sports teams or national TV networks), but it’s a tail risk that is really interesting to think about and could have big sports / business implications, so I figured I’d write it up.

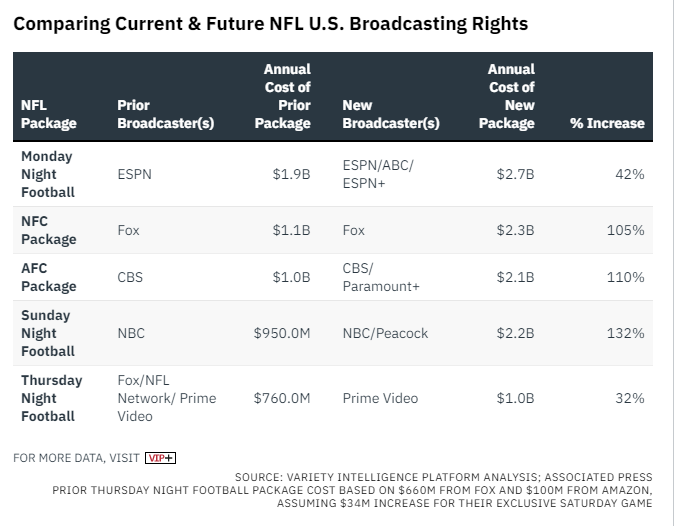

Anyway, right now, a possible national TV decline seems unthinkable. Every time a national contract comes up for renewal, we’re seeing massive, massive bumps versus the prior deals. To pull just two leagues, the NBA is expecting their rights double when they come up in the near future, and the NFL’s most recent deal saw every contract jump in value by ~50-100%.

Given the trend and competitive intensity in bidding, it seems crazy to imagine that “sports rights” will ever take a dip.

But nothing can increase at the pace that sports rights have been increasing at forever, and I think if you look under the hood you could see some potentially worrying signs for the future.

First, just consider ratings for sports. I’m a basketball fan, so let’s just use the NBA. Ratings are at best flat and likely declining (look at the NBA finals ratings over time; it’s pretty clear that the ratings trend is down). The World Series ratings for baseball might indicate the trend even better: this year’s World Series between the Astros and the Phillies (two reasonably large big market teams!) got 6.1m viewers, similar to what last year’s World Series did; if we rewound 10 years, game 1s were consistently getting in excess of 8m viewers. So ratings have dropped ~25% over 10 years, and I’d guess regular season ratings have dropped even further.

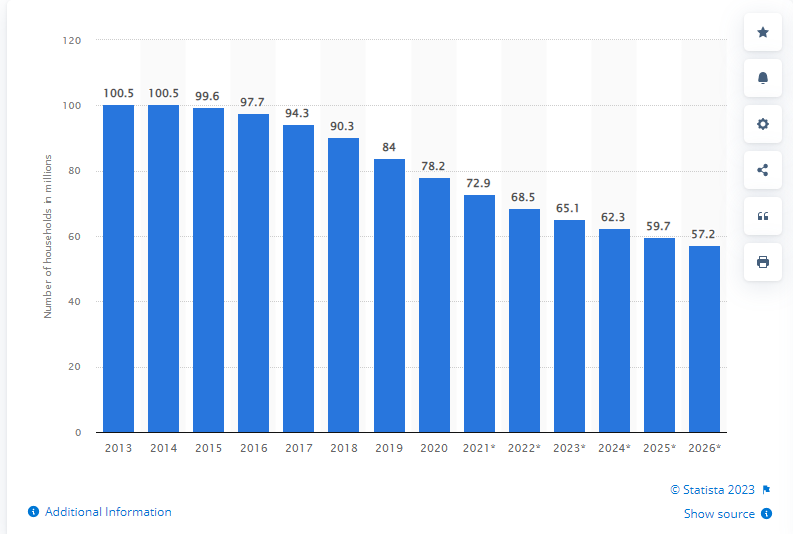

That decline in ratings somewhat mirrors the decline in pay TV households in the U.S.

You simply can’t have rights rising forever as viewership continues to, at best, stall out, and most likely continues to decline. Eventually, rights fees are going to have to reflect viewership levels.

The interesting thing is we’ve already seen how quickly the fixed leverage of rights fees can destroy companies this year. Diamond, the largest RSN, and Warner’s RSNs have both filed for bankruptcy (or are on the verge of bankruptcy / some type of default), and the sports leagues / teams will likely need to take a huge hit on whatever the successor companies will pay for regional rights.

Some might argue the RSNs are a completely different beast than the national contracts. Worse inventory (basically no playoff or marque games), lower scale, etc. I completely hear that, but the overall trends (declining interest as seen in lower ratings and less pay TV households) are still the same.

So I’m wondering what would happen if a national TV contract ever got far enough underwater to “break”. You could see that happening in two ways.

This is the most unlikely, but national contract is effectively debt. If you had a complete collapse in the Pay-TV bundle and ratings, you could imagine a scenario where a large network filed for bankruptcy to get out of their national contracts. Again, extremely unlikely…. but we did just see this happen at the RSNs! Why couldn’t what happen to the RSNs happen to, say, ESPN if the unwinding happened fast enough?

The networks are investment grade companies, so they can probably stomach a few years of being underwater on a national contract…. but the next round of contracts sees a significant down round.

#2 is the most interesting to me. Most sports leagues operate on some type of revenue share; for example, in the NBA the players get ~50% of revenue, and the owners get ~50% of revenue (which they then use to cover their other costs and eventually turn a profit). And most of that revenue money comes from the national TV deals.

These leagues just aren’t built for big down rounds at the national TV level. How are players going to feel if the salary cap comes down 10% because the national TV deals went down 20%? Are we suddenly going to see player strikes across the board?

Or consider sports franchise sales. Sports teams have seen a parabolic rise in value over the past few decades; I would guess they’ve been the best performing asset over the past ~20 years. In just the past year, we saw the record for the most expensive sports team ever sold (Chelsea for $5.3B in May). That was soon followed by the most expensive NFL deal (the Broncos for $4.65B) and then the most expensive NBA deal (the Suns for $4B). Not only were all of these deals records, but these deals were all selling out for huge premiums to prior deals. The Suns offer a great case study here: Robert Sarver bought them for ~$400m in 2004, and he sold them for $4B despite years of borderline incompetent management / ownership. That sale was a nice premium to the prior most expensive NBA deal ($3.3B for the Nets in 2019), which itself was a huge premium to the record deal before that ($2.2B for the Rockets in 2017). Heck, as I was writing this article, news broke that the Bucks were selling for $3.5B. Think of that: Milwaukee is great but a team based there just sold for more than a team based in freaking Brooklyn went for less than four years ago! The parabolic rise in valuations has been driven by record cash flows thanks to massive new TV deals and the continued desire for “live” events driving ticket prices higher and a scarcity premium as the world and particularly the super wealthy grow richer.

But what happens if we see a down round in sports rights? Do franchise valuation start going down to reflect that lower cash flow? Sports leagues have (wisely, IMO) limited the amount of debt an owner can put against their stake in a team, but if team valuations start coming down do we find some over-levered owners whose stakes are in trouble?

Or, perhaps more interestingly, if national rights start coming down and the salary caps start shrinking, do we see players look at the ~50% of revenue that owners keep and say, “owners are getting half the revenue and getting massive appreciation on their ownership stake, and we do all the work? Why not try to cut them out of the league completely, or at least demand some more equity in the league so we can enjoy its appreciation?” The history of player led leagues is pretty poor, but the PLL in lacrosse did recently outcompete the legacy league, so there is a recent path to a player league defeating an incumbent / owner league there. And it’s also worth noting that while the history of player led leagues is poor, we’ve never seen players this wealthy and business savvy before. After the next rights deal is signed, I’d guess the top NBA players will be making >$60m/season. That type of wealth will provide a lot of seed capital for competing with owners if push came to shove.

Anyway, all of this is probably too wonky and out there, but it is an interesting tail to think about that could effect a lot of different publicly traded companies and interesting business figures.

I’ve been a long time fan of publicly traded sports teams; I think it’s just so obvious that all of these are undervalued in the public markets. Sports teams are trophy assets where a lot of the value comes from things other than money. Yes, they can print money, but a lot of the value comes from relationships and soft power related to owning the team. Consider James Dolan, who controls the Knicks and Rangers. If he didn’t own the Knicks and Rangers, he’d be just some average billionaire who inherited his wealth and no one would really think about him. But, because he owns the Knicks and Rangers, every sports fan in New York City knows about him, and every politician in New York City has to deal with him. Now, given his stewardship of the Knicks, we could debate whether being “known” by all of NYC is a good or bad thing for him, but the fact remains that controlling the Knicks has brought him a level of power and control that nothing else would have brought him.

So I think sports teams tend to be undervalued in the public markets because their value does not solely come from cash flows. In fact, I’d go as far as to say owning a sports team in a public market is just flat out an inefficient way to own / control a sports team, and I think you can see that in the massive pops that sports teams generate when they are put up for sale (as detailed in this post).

But the sports teams do have some tail risk from this type of “rights down, league implodes?” scenario. Maybe they’re undervalued versus what private bidders would pay for them today, but if trends continue could you see big short cases based on looming rights cuts and work stoppages?

Interesting to watch / think about!

Great article . Perhaps another opinion. In the Uber capitalist economy that we live. Sports allows for focused advertising. The players don’t get paid for merely toting a ball, but in fact they are running billboards that eye balls actually focus on. Add in a bit of virtue signaling and people feel good about paying money for adds.

https://stratechery.com/2023/what-the-nba-can-learn-from-formula-1/