Risking a zero: tail risk, disruption, and Malone

I’ve found myself thinking a lot about the online gaming companies (Draftkings, Fanduel, etc.) this year.

In part, that’s out of personal interest. I’m a sports fan, and gaming companies sponsor basically every sports podcast I listen to…. so it’s hard to avoid them! On top of my fandom, I’m also a user; I don’t gamble much, but if I’m going to watch a game I’ll generally throw ten bucks on it just to be a little more invested, and I’ll also make use of the sports apps’ various promos when they pop up (I’ve got a lot of nostalgia for the mania of the NYC launches!)!

But, outside of my personal interest, I’m interested in the businesses because they are facing interesting types of competition. Prediction markets and even traditional brokers have started offering futures / event contracts on sports outcomes, and the prediction markets dominate the sports books in two ways: they are significantly cheaper than sports books, and they may have significant tax advantages. That combination has resulted in some rapid growth; one analyst estimates Robinhood is already run rating $200m in revenue from prediction markets (and Robinhood’s CEO has been happy to brag about that!). To put that size in perspective, Draftkings will do ~$6B in revenue this year, so Robinhood isn’t quite Draftking’s sized yet but given HOOD launched the business just this year the growth is absolutely wild and at this rate it’s not crazy to think HOOD’ll be a top 5 sports book in the near to medium term.

Now, I personally think the risk to online gaming companies from prediction markets is probably overblown for a variety of reasons (in particular, the real money for sportsbooks comes from parlays and exotic bets, and I don’t think prediction markets could ever offer a deep parlay market… I also suspect if prediction markets grow much bigger there will be a significant regulatory crack down for a host of reasons), but I’m absolutely not 100% confident in that prediction (pun unintentional!)…. and, given I don’t have a position in the gaming companies, I don’t have to be confident in the prediction! I can just bust out the popcorn and enjoy the business evolution from the sideline (while making the occasional wager!).

But the rise of prediction markets / event contracts and their threat to gaming companies is a tidy example of something I’ve been thinking about a lot: assessing tail risk in investments and, more importantly, making sure you’re getting paid for it when you make an investment.

Why have I been thinking about tail risk? A bunch of reasons, including that it’s always a really interesting topic to think about! But one of the major reasons I’ve been thinking about tail risk is John Malone’s memoirs came out this month (and we’re reading them for book club!). The memoirs are a really fascinating read, but a consistent theme of the book is these absolute titans of media and industry going to all-out war against each other to make enormous acquisitions of companies that would become zeros within a few years. Just off the top of my head, the list of disastrous acquisitions includes:

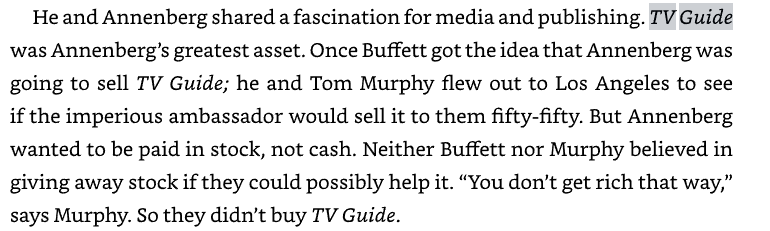

All the machinations around TV Guide (bought for $3B in 1988, valued around that price in a merger in 1998, sold again in 2007, probably a zero today?)

It’s easy to forget now, but pre-internet Buffett loved the TV Guide business and had tried to buy it; from Snowball:

Redstone / Viacom buying Blockbuster to be a cash cow in the early 90s

A list of internet deals so long that I can’t list them all here, but headliners would include AOL, excite@home, etc.

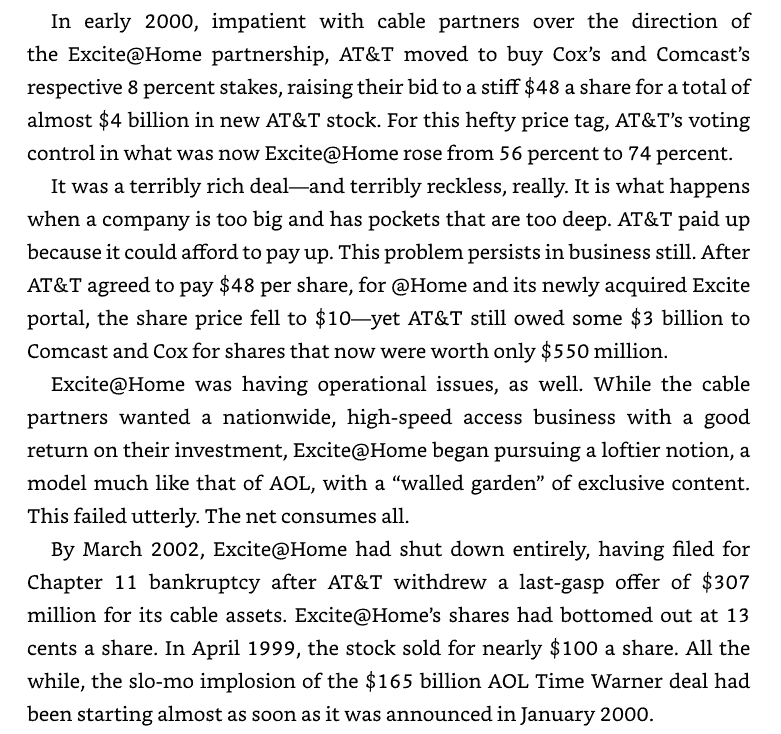

AOL obviously gets all the headlines, but excite@home is my favorite story. A multiple billion merger (one of the largest ever at the time) that peaks at a $35B market cap to a full bankruptcy in less than three years!

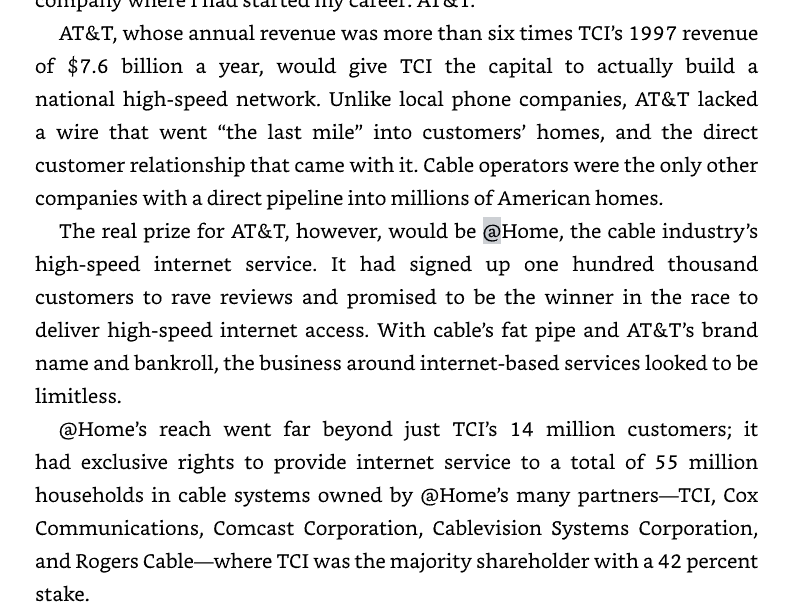

Basically every deal legacy AT&T made (it’s truly incredible to revisit how many disastrous deals AT&T did over the years!)…. again, the list is too long to recount (I did a mini-thread here, but I probably could have found ten more examples), but perhaps my favorite under the radar one is the AT&T consider Home the trophy asset in their TCI acquisition…. yes, the same Home that would liquidate a few years later! (clip below from the book)

Humorously, T would even bail many of their partners out of Excite@Home when the business was cratering:

Almost every deal related to satellite internet ends in tears (this is headlined by the T / DTV deal, but there are plenty of others that lead into it!)

The specifics of what happened to each business varies; some found their business model outdated as tech advanced, while others were just inflated by the dotcom bubble. But all of these deals were hotly contested when they happened; again, many of them were considered crown jewels when they were put up and eventually sold after heated bidding wars!

So I’ve been thinking about all of those blockbuster deals and bidding wars in the context of today’s markets and businesses. I’m not exactly breaking ground when I say that AI is here and changing the world, and it’s already decimated some businesses (hello Chegg!).

But reading Malone’s memoirs and just looking at the history of disruption, it strikes me that there are plenty of businesses that are getting priced like AI won’t impact them (or, perhaps, even as AI beneficiaries) that are going to get eaten alive by AI and the shifting landscape, and what I’ve been trying to do is think about is:

What businesses are currently getting priced like AI will have no impact on them, but have some type of terminal tail risk?

How do you model and price the risk of a business that has some “AI terminal risk”?

Anyway, work in progress, and something I’ll have more posts on in the near future… but, as always, if you have thoughts on the topic, I’m happy to swap notes in the comments / over email.

PS- This is part 2 in my loose series on tail risks and zeroes. You can find part 1 (Frauds, Ponzis, and BRK) here.

PPS- Speaking of “more posts on in the near future”, one area I’ve been thinking about around disruption is stablecoins, remittances, and payments. AlphaSense was kind enough to sponsor a free webinar with a payments expert (a Mastercard former) to discuss the subject; it was a really interesting conversation, and it goes live Tuesday (you can find an early peek at a discussion on stablecoins here). If you’re interested, you can sign up using this link