$MGI and the opportunity set in rumored deals

Yesterday, MoneyGram (MGI) announced a deal to be acquired for $11/share, a nifty little premium to the prior day’s closing price of ~$9/share and a rather large ~50% premium to the “unaffected” share price of just over $7/share from December 14 (before Reuters broke the story the company had a bidder).

That’s pretty typical stuff in the world of M&A. But something about this particular fact pattern struck me as curious.

Reuters reported that MGI had a bidder at $10.50/share back in December. Then, in January, Reuters confirmed MGI had run a process and gotten three bids. Now, I’m not an investment banker, but it seems pretty obvious if a major news outlet reports a bid and includes the price (as Reuters did in December) and the company then runs a process that attracts multiple bidders, the new bidders aren’t going to be coming in at a price under the original bid. If they decide the company is worth less than the original bid or their DD unearths something they don’t like, they’re probably more likely to just pass than go through all the effort of raising financing and putting in a bid that’s clearly inferior.

So MGI closed Monday at $9/share. If you believe the above (that any new bids would need to come in at or above the $10.50/share Reuters reported in December) and that MGI would fall to its pre-rumor price of just over $7/share if they decided not to sell, the market was putting in basically 50/50 odds that MGI would take a deal (~$1.50 up if they took a deal at $10.50, ~$1.50 down if they rejected and fell to pre-deal levels). That’s rough math; it’s possible that the market looked at three PE players making rumored bids for MGI and says “maybe we were too pessimistic at ~$7/share before the rumors started and fundamental value is actually higher.” And it’s possible that the winning bid came in materially higher than $10.50/share (i.e. we get a bidding war and a strategic comes in and pays $15/share or something). So, again, rough, simplified math; if you adjust for those odds, the market was probably saying less than 50/50 shot of MGI taking a deal.

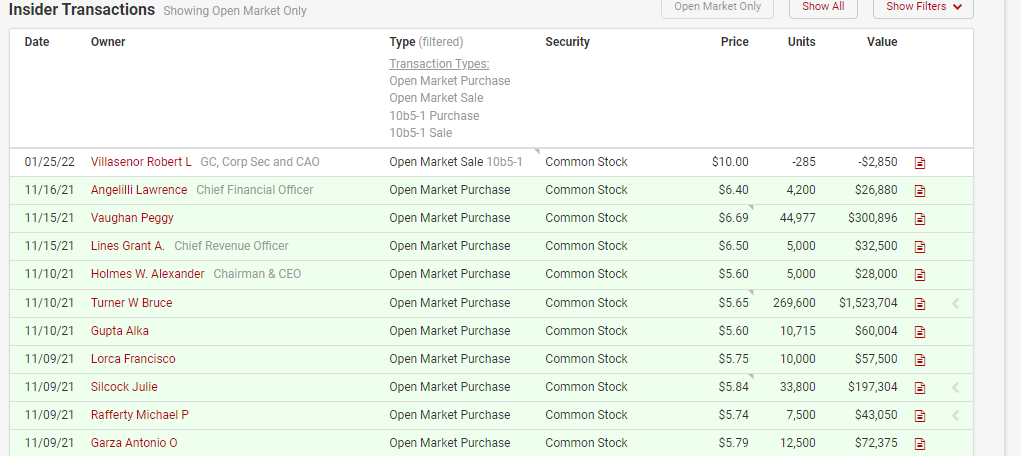

Which just feels wrong to me. Again, you had a very reputable news outlet (Reuters) reporting a bid at a big premium and that multiple bidders were involved after the company had run a process. Insiders seemed reasonably aligned here; the company had tried to sell themselves a few years ago (that deal was blocked on national security concerns), suggesting the board was open to a sale, and insiders across the board had just bought a decent amount of stock on the open market in November.

So it all seems really obvious / easy in hindsight. In real time, it certainly wasn’t quite so easy; I had a very small position that probably should have been 10x bigger. I just kept looking at the gap between the market price (~$9/share) and the reported initial offer ($10.50/share) and saying to myself, “I have to be missing something, right? It can’t be this easy / obvious.”

Maybe MGI is unique…. but it feels to me that there are a lot of situations right now with lots of similarities to MGI that are trading at pretty large discounts that seem to imply pretty solid risk / reward in event driven names that shouldn’t have crazy market correlations.

I’ll give a few sample situations in a second, but with any opportunity set it’s worth asking “Why have the market gods presented me with this ‘gift’?” In the case of these event set ups, I think there are two possibilities:

I’m just a crazy person and completely missing something

Markets have been absolutely brutal recently, and funds aren’t willing to deploy serious risk capital after having their heads beat in for the past ~9 months.

I obviously lean towards #2, but #1 is a real possibility!

Anyway, just to highlight the opportunity set, here are two situations I’m currently looking at that strike me as interesting / somewhat similar to the MGI set up. I’ll emphasize these are just situations I’m following; I’m not saying either of these are the best set ups in the history of the world or anything. But they do seem like very solid set ups for deals that have a decent shot of happening and/or getting bumped from here and in companies that are probably fundamentally undervalued even in the absence of a takeover.

CNR just got a buyout offer from their largest shareholder at $24.65/share. As I write this, the stock trades at $21.80. That’s a very large discount for an initial offer from a financial bidder who knows the company well!

KSS has received one offer at $64/share, and we know both Sycamore and Leonard Green have expressed interest in them as well. An activist is looking to replace the board and pressure the company to sell. The stock trades at <$60/share, which is around the price the company was reasonably aggressively repurchasing shares last April (per their 10-Q)

Those are just two examples, but I chose them for very specific reasons. These are multi-billion dollar companies that trade millions of share per day, so you can’t argue “O, those are too small for real people to get involved (like you maybe could for MGI).” And these are companies with offers from financial, not strategic, buyers. Financial buyers buy for one reason: they think something is undervalued. They don’t buy because they think something is fairly valued but has material synergies with their operating business (like a strategic would do!); compare these bids to something like Cedar Fair (FUN), which rejected an offer from Sea World. That’s probably an interesting situation, but Sea World is clearly bidding with strategic / financial synergies in mind, which is much different than a financial acquirer coming in with no synergies and basically saying “this stock is too cheap.”

So I chose KSS and CNR for specific reasons, but I can list probably five to ten other stocks that fit into a similar bucket right now. The market just seems rich for this type of event investing right now. Happy hunting (and, of course, feel free to DM me if you see any other interesting situations!)

PS- One bonus MGI thought while I’m here. The merger includes a go-shop. MGI had already run a process (according to Reuters). It’s strange but not unheard of for a company to run a process and then include a go shop. What is strange is that, in the event of a topping bid, the go-shop calls for different payments to be made to the parent (the current buyer) depending on who the new buyer / bidder is (see the language from the merger agreement below; emphasis mine). I understand why they did that (the current buyer doesn’t want a bidder who just lost the process coming in over the top because they know the exact number to beat now), but I don’t think I’ve ever seen this term before. I increased my position a bit after reading the agreement; on the whole it just seems like the initial process was run for financial buyers and they set up a go-shop that allows for the possibility a strategic comes over the top (compound has a quick list of a few strategics and why they might want MGI). Obviously I could be wrong, but it seems like a pretty interesting risk / reward with limited downside (heads you get a topping bid; tails you probably break even given I don’t think the deal falls apart inside of the go shop!) so I figured I’d give in to my spidey-senses. Still a small position though!

The Merger Agreement also provides that, in certain circumstances, including the termination of the Merger Agreement by the Company to accept a Superior Proposal (as defined in the Merger Agreement), the termination of the Merger Agreement by Parent following a change in recommendation by the Company Board, and other customary circumstances, the Company would be required to pay Parent a termination fee of $32,800,000, except if the Merger Agreement is terminated by the Company to enter into a competing acquisition agreement during the Solicitation Period or within 20 days thereafter with a buyer solicited under the go-shop provisions in the Merger Agreement, in which case the Company would be required to pay Parent a termination fee of $16,400,000 (or $30,000,000 if such buyer was a certain type of prior bidder as specified in the Merger Agreement). The Merger Agreement also provides that, in certain circumstances involving termination of the Merger Agreement following a failure by Parent to consummate the Merger or a material breach by Parent or Merger Sub, or the failure to obtain required approvals with respect to money transmitter licenses (if such determination is final and non-appealable), Parent would be required to pay the Company a termination fee of $65,500,000, except if the Merger Agreement is terminated due to the failure of obtaining required approvals with respect to money transmitter licenses, in which case Parent would be required to pay the Company a termination fee of $30,000,000. Parent’s obligations to pay any reverse termination fee and certain other fees and expenses up to a cap are fully and unconditionally guaranteed by the Guarantors.

PPS- This post would normally be a “weekend thoughts” post, but I’m on vacation for the long weekend and this is semi-timely given MGI just announced their bid, so I figured I’d get it out now. Consider this an “almost the weekend thoughts” post, and I hope you enjoy the long weekend if I don’t post before then!

SHLX - cash offer, puts are overpriced, and rich history of takeunders by GPs in the energy space.

Eh. Hard to put any juice into KSS when Acacia pretty much established themselves as a (starboard backed?) saber rattler with CMTL like, moments before...