"Markets in turmoil": tariffs edition and rebalancing your portfolio

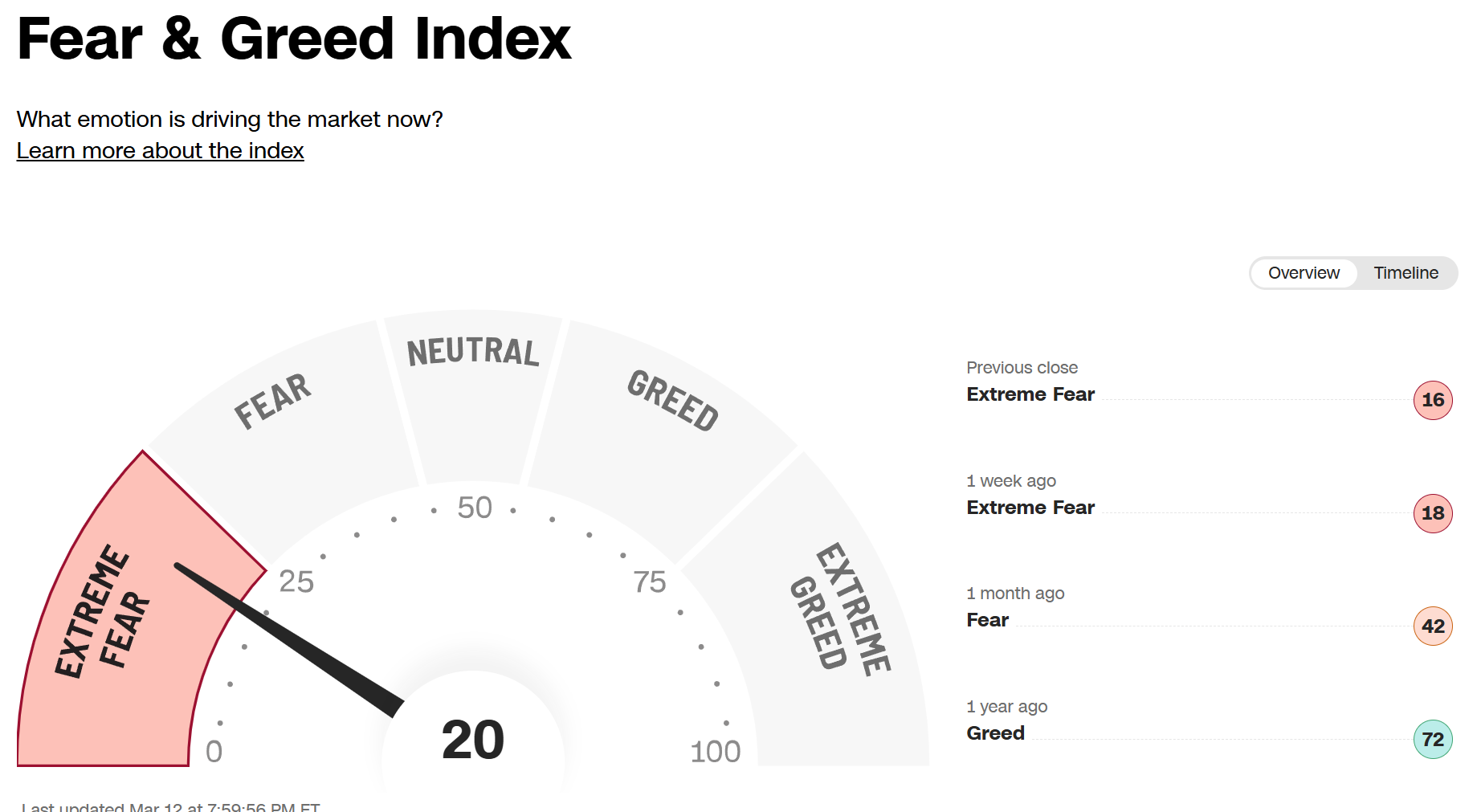

Every month, I like to use CNN’s fear and greed index to gauge Mr. Market’s emotions. After a brutal few weeks, the gauge now sits solidly in “extreme fear”.

I like to use the Fear and Greed Index because it’s a really fast short hand that anyone can understand. If I called my mom and said “man, markets are brutal right now, the VIX just hit 40”, she would think I was smoking something…. but if I showed her that image above and said “markets are in extreme fear”, she’d understand in a second.

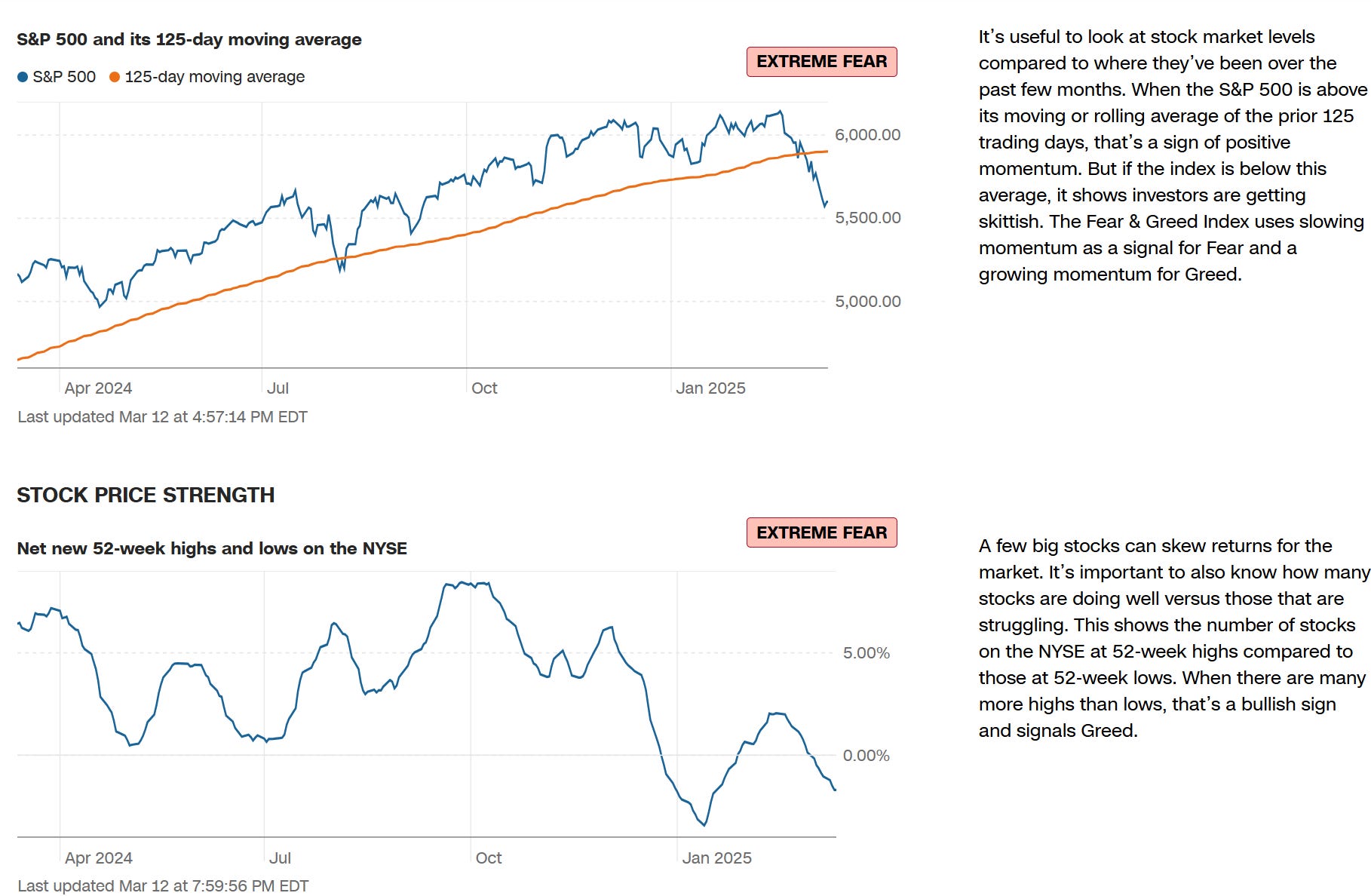

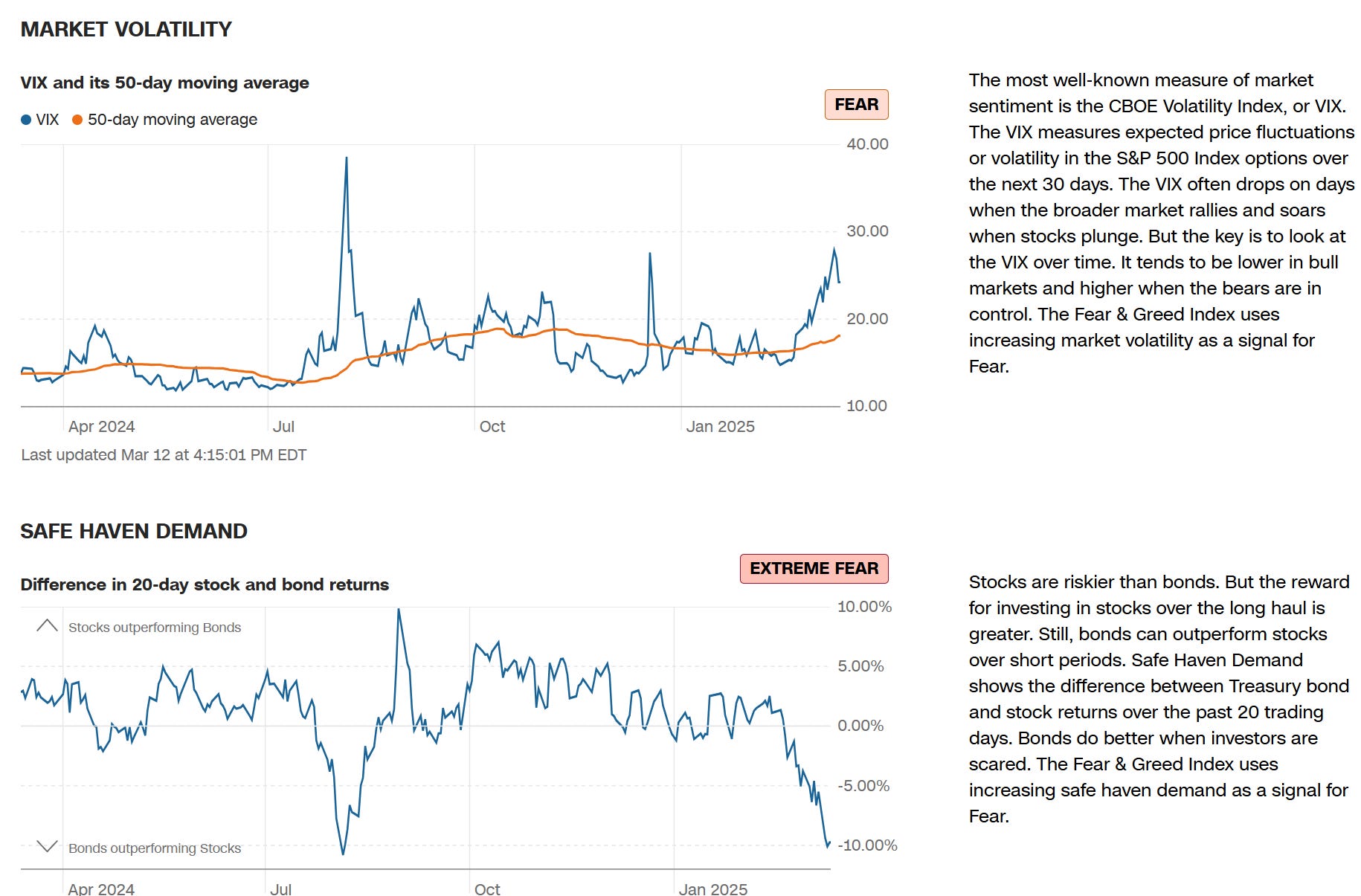

So it’s a nice short hand, but it’s obviously not perfect. Some of the underlying indicators are a little silly, and a small change in price can quickly flip one indicator from greed to fear or vice versa…. in particular, the 125 day moving average can hit “fear” or “extreme fear” territory pretty quickly even when markets are chopping around all time highs. That said, right now pretty much every indicator is hard into the “extreme fear” category (which doesn’t happen often!).

I wanted to mention the fear and greed index now for three reasons.

A reminder- When the fear index is high, that’s the time to buy, not sell. You’ll always hear about someone’s parents or grandparents who had all of their money in the market, panic sold at the bottom, stuffed it all under their mattress, and cost themselves a mini-fortune as they missed out on the market rebound and then compounded the mistake by never getting back into the market. Don’t be that person1.

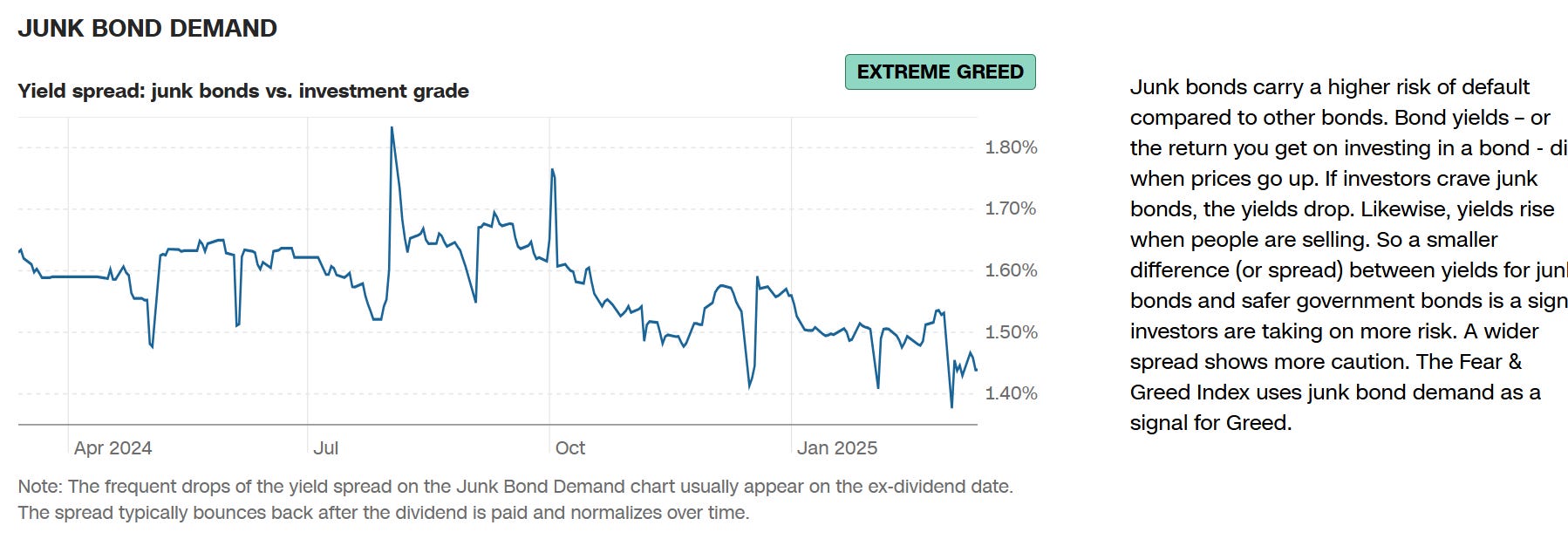

A trading thought: I can’t believe junk bonds / high yield spreads haven’t blown out a little more. Some of the companies I follow are priced for imminent distress or a really apocalyptic macro environment; not sure why that wouldn’t hit bonds too. I wonder if there’s something in the index that is keeping spreads tight / I wonder if it’s an opportunity…..

A psychology thought- I talk to a variety of investors; I’m not sure if I’ve ever felt / seen investors feel more divergent depending on what they focus on. For example: for my friends who have been investing in Europe, I’d say this is the best they’ve felt in a while as Europe has finally caught a bid. For a lot of my other friends who invest in smaller / more cyclical / more domestic stuff, I’d say this is the most despondent I’ve ever seen them. Even more despondent than COVID- I think COVID happened so fast and was so wide spread that a lot of people didn’t have time to adjust, and there were so many external fears that maybe the markets cratering wasn’t fully registering. This time is hitting a bit harder for a lot of them for some reason.

So markets are really scary right now. That’s probably an opportunity….. but I wanted to write this article because there’s one aspect to big draw downs / market sell offs that I find very difficult / that I’m trying to improve at, and I thought writing it down might kill two birds with one stone (help me get better at it and help my readers with portfolio management!).

That aspect? Selling companies that you know well in a drawdown to take advantage of better opportunities.

I think the best way to show this is just to give a hypothetical. Say that you buy XYZ for $100/share, and you think it’s worth $150. The market just completely tanks and goes down by 50%, and XYZ goes down with it from $100/share to $80/share. So yes, the stock price has moved, but XYZ is a phenomenal business with literally no macro concerns, and you are 100% convinced its fair value remains $150. You should, at worst, hold the stock, and most likely buy more, right?

Maybe not! The opportunity cost of holding XYZ has increased quite a bit. Maybe company ABC is worth $100 and was trading for $100 when you bought XYZ, but with the market down 50% maybe ABC has gone down even more and is now trading for $20. XYZ is trading for just over half of fair value right now, but ABC is trading for 20% of fair value! Even though XYZ is more undervalued today than when you bought it, you should sell XYZ and buy ABC!

Now that is a very simplified example for a ton of reasons, but it’s the type of trade-off / thinking that investors need to be making right now. There is a lot of dislocation in the market, and there’s a decent chance that your best opportunities from last month are no longer your best opportunities if you’re following a reasonable number of stocks. I personally find it difficult to sell companies that I know well that are down to buy other companies, even if I know those other companies well too and those companies are down more. That’s a hesitancy I’m trying to break.

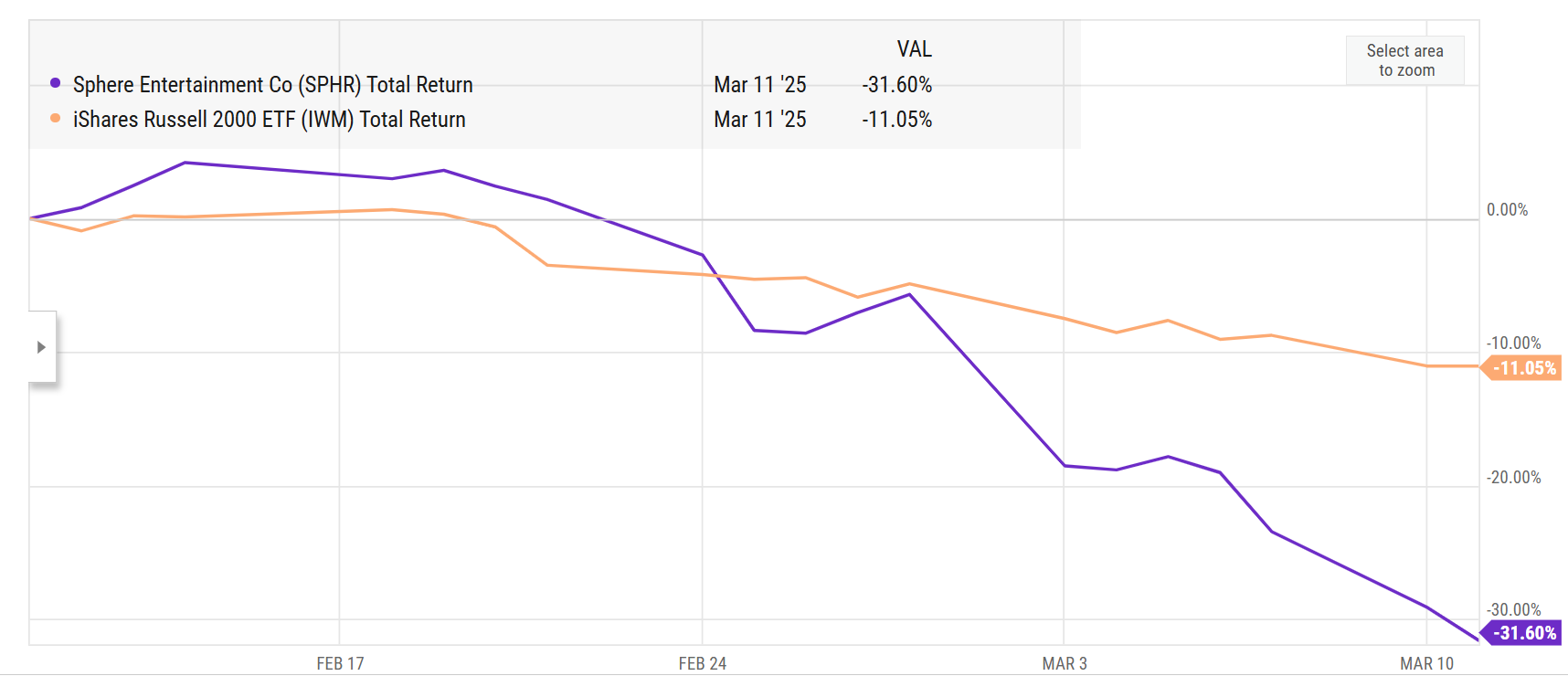

Let me just give you an example of a potential opportunity. Consider the Sphere (SPHR); it’s a name I know well despite having no position in it. The Sphere is down ~30% over the past month, while the Russell 2000 is down ~12%. The Sphere is a giant metal ball sitting just off the strip in Las Vegas; it’s really hard for me to imagine any short term macro concerns or tariff worries or whatever have caused the long term value of that asset to fall by 30% (from >$45/share to ~$30/share).2

Now, I’m not saying the Sphere is an opportunity here (though I’m also not not saying that!); I’m just using it as an example. It’s down quite a bit and more than the market; you have to look at everything in your portfolio against the opportunity cost of buying things that have been beaten down. To bring this back to my opportunity cost thing, let’s say you followed the Sphere closely and thought it was worth $60/share. However, you weren’t long the Sphere last month because it was trading for $45/share and, in this hypothetical world, there’s a company called the Cube that you also follow closely that is also worth $60/share but was trading for $40/share. So you instead own the Cube as it’s cheaper. Then the current market selloff happens, and the Cube trades from $40/share to $35/share. Guess what? It’s time to sell the Cube and rotate into the Sphere…. yes, the Cube is cheaper today than it was last month, but the Sphere is now trading for ~$30/share, so it’s trading for a bigger discount to fair value than the Cube! Swap into the better opportunity!

That’s the type of trade / swap I’m thinking about a lot right now. Of course, it’s very difficult to do. In my example, we were comparing two identical assets (the Sphere and the Cube); in the real world, you’re comparing across asset classes and industries (i.e. these defense companies I follow are great business and very stable and they’re down 20%; does that make them better or worse risk adjusted values than the energy companies I follow that are down 50%?), and their intrinsic value is moving a bit with different news (I assumed the Sphere’s value was static at $60/share in my example, but many companies will have their intrinsic value reduced by tariffs, or they may have some leverage concerns that create added risk as the macro grows worse, etc., so you need to update your fair values as new news comes out!).

But your job as a portfolio manager is to look at all the information you have right now and dispassionately apply it to your portfolio. If I’m being honest with myself, the best opportunities I’m seeing today are not the best opportunities I was seeing last month, and taking advantage of the best opportunities now often means selling some companies I know well at a loss to take advantage of bigger opportunities.

And look- sometimes that can mean selling companies at a big loss. It’s entirely possible you’re long XYZ and it’s down 30%…. but their earnings were a disaster and the current macro is clearly going to hurt them. In that world, company ABC that is only down 10% might actually be a much better value. Ignore your cost basis, rip off the band aid, and swap into the better opportunity!

Anyway, bottom line- it’s not easy, but the best way to invest is to constantly look at your portfolio dispassionately and swap into the best opportunities. That’s always true, but it’s particularly true during big sell offs when things can get dislocated and some opportunity sets can pop up that are extremely lucrative. It’s what I’m trying to do now; personally, I’m finding the best opportunities in beaten down biopharms, and when I really dispassionately hold the mirror up to my portfolio a lot of my long time holdings simply don’t have the same risk reward as those…. so the long time holdings need to go. Not easy, but I think in the long run that decision will get rewarded.

PS- Completely unrelated to the above, but my friend Alex Morris came on the podcast last week, and I completely forgot to mention that he has a free expert panel on Nike / Digital Transformation coming up. Alex and I have talked a bit about Nike / Digital, and I know he’s done a ton of work in the space (plus he’s got some great experts), so I’m excited to check it out (you can sign up here if you are too).

I think all of this is just generally best practices when dealing with the market, but I will pause here to remind that nothing on here is investing advice, consult a financial advisor, see our legal disclaimer, etc.

Note that there’s no particular reason for why I chose the SPHR; I could point you to twenty other stocks that are down 25% or more over the past month that are probably interesting. I just chose the Sphere because it’s an interesting asset that I follow and have discussed before!

Great insight

Thanks for the shout out Andrew!