How much is a great manager worth? $QXO $BECN

Last week, I did a post on (bad) incentives and (poor) corporate governance. As I was writing that post, QXO was closing their deal to buy BECN (WSJ on deal close; FT on deal close). I think BECN / QXO is just a fascinating situation, so I wanted to put a few thoughts down on it.

Why do I think the situation is so interesting?

Because the market is betting that an ~average company run by ~average managers (which I think BECN roughly was1) is worth ~two times as much under an extraordinary manager (which I think Jacobs has proven to be) as it was previously under the average-ish management team. And, to be honest, I don’t know if that premium is too much, too little, or just right. It will be fascinating to find out (I have no horse in this race!).

Let me back up a little to explain that paragraph. Let’s start with the simplest: Jacobs is a great manager. I don’t think that should be too controversial; his track record speaks for itself. I’m not sure if there’s another manager alive with his track record of building multi-billion dollar companies (and, given Jacobs’ book is “how to make a few billion dollars,” Jacobs certainly knows that too!). Sure, some people have built bigger companies, but how many people have done it more than once? Not many…. and Jacobs has done it 3-4 times now!

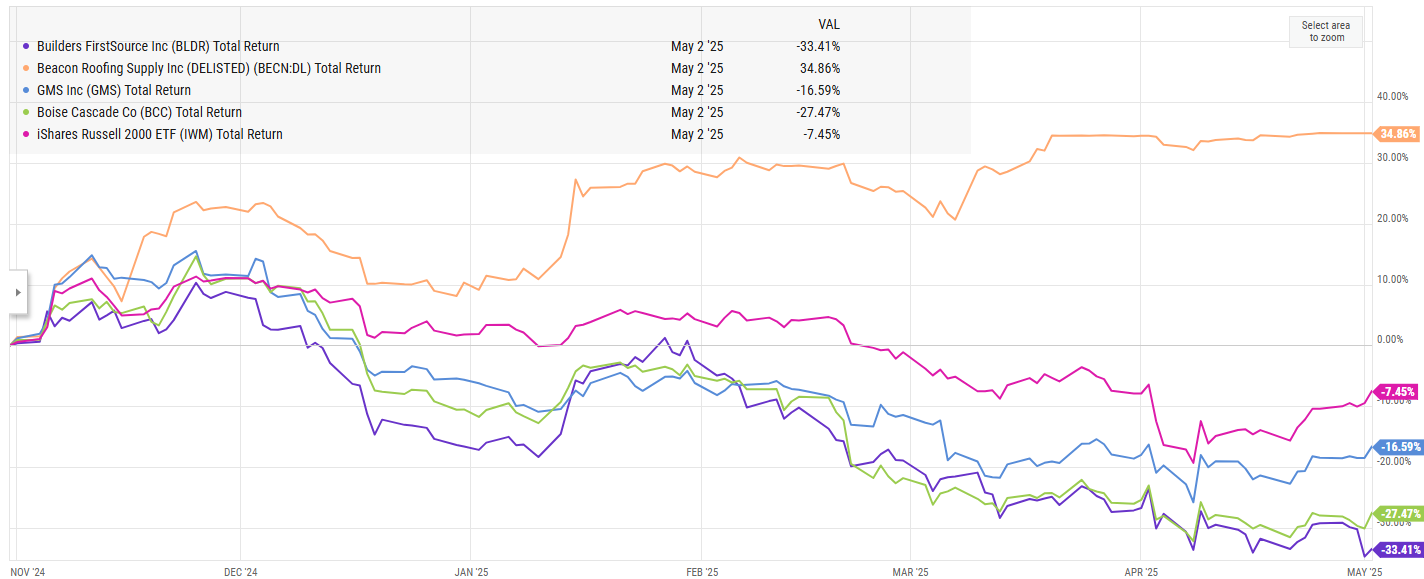

Let’s turn to the next piece of that statement: BECN was ~an average company with ~average management. I can’t claim to be an expert on BECN, but I don’t know anyone who would have pointed to BECN’s results (be it operating or stock performance) and said “this is a company that is horrifically mismanaged” or “this is the best managed company I’ve ever seen.” Again, not an expert, but their stock had tripled over the past ten years, neatly outperforming the indices but trailing think is their closest peer (BLDR2), and a glance at their financials doesn’t reveal any glaring under or overperformance versus peers (even QXO’s hostile tender docs had trouble pointing to a problem at BLDR other than “we’re paying you way more than you’re worth standalone and you won’t take our offer”).

Sometimes, in M&A, you’ll see a company that’s getting run by a bunch of clowns, and an acquirer can pay a huge premium because the acquirer can come in day one and massively improve performance by installing a bunch of average managers to replace the clowns. Basically, on a scale of 1 to 10, the company is getting run at a 1 or 2 and an acquirer bets they can make a fortune by coming in and taking the operations to a 4 or maybe 5 (and make a huge fortune if they can do better!). That does not appear to be the case with BECN; BECN was probably getting run somewhere around average…. an industry expert could probably come in and make an argument for exactly where BECN was getting run (i.e. were they a 4 out of 10? A 7 out of 10? I don’t know!), but no one would say “BECN is a disaster; I’ll make a fortune buying them and stabilizing.”

Instead, QXO is making a bet that they can come in and take operations from “around average” to “exceptional.” And, for the privilege of making that bet, QXO paid a huge premium. QXO’s hostile offer docs back in January noted they were paying a ~26% premium to BECN’s unaffected price and a 17% premium to BECN’s all time high stock price; however, those numbers probably understate the premium QXO paid for BECN because the entire industry had fallen off since the first QXO bid:

With the indices down and peers down even more, I think you could make a fair argument QXO paid a ~50% premium to where BECN’s stock would have been trading without the QXO offer on the table (I actually think the premium may have been bigger / the stock would have been lower without the bid). QXO paid ~$11B EV all in for BECN; some of that EV is debt, but if you think the unaffected price of BECN would have been ~$80/share without the QXO bid, then QXO paid ~$2.5B of acquisition premium to buy BECN (~62m shares outstanding * ~$44/share premium over the unaffected3). BECN had some debt, so the equity premium I just laid out actually overstates the premium on an enterprise value basis; on an EV basis with that math, QXO paid maybe a 30% premium to BECN’s unaffected value.

Again, BECN does not strike me as a company that was particularly poorly (or impressively) run before QXO bought them. QXO is betting that by taking a company that’s ~average and putting them in the hands of a legendary entrepreneur (like Jacobs), the company is instantly worth >30% more. Is that a reasonable bet? Probably!

But investors are actually upping the ante on that bet. When QXO announced the definitive deal to buy BECN, QXO’s stock was trading for ~$13.80/share. Interestingly, QXO was trading for basically double their asset value (at the time, QXO was effectively a cash shell with ~$5.1B in cash ~($6.90/share) and ~739m diluted shares of stock (I’m using their cap structure before the recent round of BECN-deal close related equity and debt raises changed the cap structure!)). The difference in price between QXO’s BECN-close trading price ($13.80/share) and QXO’s cash (~$6.90/share) could be looked at as how much value QXO shareholders thought Jacobs would create from M&A; that comes out to ~$5.1B in implied value creation… however, remember that value creation has to be above and beyond the ~$2.5B premium we just calculated that QXO paid to buy BECN. Add those together, and QXO shareholders were betting that QXO would create >$7.5B of value from buying BECN…. we just calculated that BECN would have been worth barely more than $8B EV if it was trading standalone in the public markets, so QXO shareholders were betting that BECN is worth almost twice as much in QXO’s hands with the Jacobs magic applied to it as it was worth in the public markets.

Now, I know QXO bulls will quibble with a bunch of things in this analysis. The main argument QXO shareholders will have is that BECN is just the first step in the Jacobs playbook; he’s clearly going to use BECN as a backbone of an M&A / roll up strategy (a huge part of the Jacobs playbook). And QXO will run more levered than BECN was running standalone; that leverage will amplify value creation and give more room for acquisitions. QXO shareholders are absolutely correct on both of those points; Jacobs / QXO can and will do those things…. but levering up and rolling up are not strategies that are unique to QXO! BECN very much had those opportunities available to them as a standalone company; they just chose not to pursue them for one reason or another.

Why didn’t BECN chose to pull the leverage / M&A levers if they’ll create value? Well that’s an interesting question! Perhaps the reason the market thinks BECN is worth basically double its standalone value under Jacobs / QXO ownership is because M&A / leverage are value accrettive when done by an outstanding manager (like Jacobs!) but value destructive when done by an average-ish management team (like BECN’s old team). That would make total sense to me… but again, it’s fascinating! What’s so unique about Jacobs / QXO that they can make fortunes doing things that everyone else in the industry could do on their own but would destroy value doing?

Again, I have no horse in this race. But I’ve followed it out of the corner of my eye gives the hostile bid / event driven nature / having loosely followed Jacobs for years, and given my recent coverage of bad incentives and poor capital allocation, it’s a really interesting case to see a company where stock holders (probably correctly) are betting on an enormous amount of value creation after looking at busted biotech after busted biotech where shareholders are pricing out exactly how much value will get destroyed…. and it’s really interesting to see how much more the market thinks average companies are worth in the hands of skilled allocators.

PS- Jacobs has a pay package that will give him enormous upside if QXO is a grand slam (you can see it on p. 28 of their proxy). It doesn’t move the needle much so it’s not worth splitting hairs over, but it’s worth pointing out that QXO shareholders are actually betting on more value creation than I laid out above once you start factoring in the overhead drag from Jacobs and the rest of the C-suite’s incentive payments! Not saying the team isn’t worth it, just pointing out the dilution is a real cost and it suggests shareholders are betting on even rosier targets than I laid out!

Note that saying a management team and business are “about average” can come off as an insult; it is certainly not meant that way. Reasonable people can disagree if BECN were a bit above or below average or right in the middle; I don’t think the results would allow for any disagreement of them being insanely above or below average! “About average” as a publicly traded company is a dig the same way saying an NBA player is “about average” for an NBA player; that means they’re in the 99.9% of skill!

Or at least I think that’s their closest competitor; again, not an industry expert!

The unaffected would have been $80 in this example, and QXO bought BECN for >$124/share, so ~$44/share premium

jacobs mentioned on podcast that qxo is not a longterm gig, ~decade.

of course, subject to changing incentives as always with this type personality.