Corporate dark arts: the strangest 8-K I've ever seen $DMRC

One of the areas of the market I’m tracking most closely right now is the “dark arts”: how management teams and boards can reveal company value and inflection points through how they use compensation to enrich themselves. It’s a huge focus of mine…. so much so that I wrote a twelve-part series on it recently!

This week, I saw perhaps the strangest “dark arts” filing ever: DMRC put out an 8-K that gives their incoming CEO a shot at a >$40m payday if the stock roughly 5x’s over the next four years.... and, a few paragraphs later, discloses substantial doubt about the company’s ability to continue as a going concern. I instantly texted it to my buddy Tarot Capital (Tarot does awesome work on corporate governance setups if you’re looking for someone other than me to follow in the space!), and I’ve been thinking about it for two days straight, so I needed to put some pen to paper.

So how did we get here? In June, DMRC announced that they’d hired a new CEO. It seemed like a great hire; the press release notes the CEO turned his last company into a “Rule of 50” company, DMRC’s chair gave a ton of glowing quotes about the new CEO, and the old CEO would remain on the board1.

However, buried within the 8-K announcing the new CEO were some interesting items. First, the company noted they’d established an “at the market” (ATM) offering of their common stock. ATM offerings are never a good sign for a stock (at least in my opinion!)….. but more concerning was that the bottom of the 8-K disclosed a customer “exercising a contractual right to terminate two of its contracted projects with the Company, effective June 16, 2026, due to a change in requirements imposed by its government end-customer.” These projects represented $2.7m in ARR2, a not insignificant amount given DMRC reported $15m in ARR in their March quarter!

So you’ve got a company with a new CEO incoming and a history of maybe quietly burying bad news inside unrelated 8-Ks….. which sets the stage nicely for DMRC’s July 6th 8-K. On the surface, it appears benign, as it simply announces the new CEO officially stepping into the job. However, the fine print here carries a lot of weight, as buried in the 8-K are:

The terms of the new CEO’s PSUs, which have the potential to be very juicy… if the stock goes up a lot

A disclosure that the company believes its cash “will not be sufficient to fund the Company’s operations,” and that “substantial doubt exists about the Company’s ability to continue as a going concern.”

That is just a wild combination. I don’t think I’ve ever seen an 8-K that expresses so much bullishness on the top end alongside a possible going concern warning! And the mechanics make it even better: the 8-K notes the going concern disclosure is being made in connection with the company’s S-3 and S-8 registration statements. In other words, DMRC had to admit substantial doubt about their ability to survive in order to register the shares underlying the new CEO’s moonshot grant (and to keep selling stock on their ATM)!

The going concern warning explains the bearish side all by itself, so let’s quickly dive into the CEO’s pay package to see the bullish side of things.

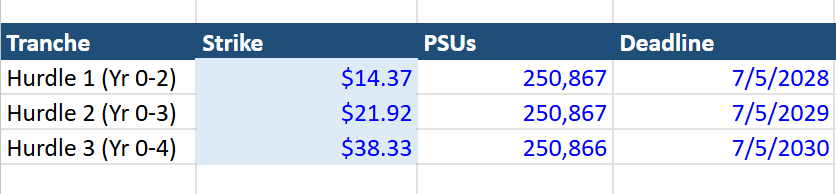

If you go back to the early June 8-K, you can see the CEO will make $500k/year in salary with a target bonus equal to his salary. So call it $1m/year in target cash comp. He also got ~300k shares that vest over the next four years (DMRC’s stock closed that day at ~$13.50/share, so at grant this was worth >$4m if they vested), and up to ~750k more shares that vest “on achievement of certain stock price goals.”

The July 8-K laid out the stock price targets; a table will probably show them best:

DMRC’s stock closed at ~$7.65/share on July 6th (the day the 8-K was filed), so those targets were wildly aggressive. You’re talking ~40% IRR to hit the 2028 and 2029 tranches, while the 2030 tranches would require the stock to do ~50% IRR and go up ~5x over the next four years!

Now, you could argue that DMRC’s stock has been on a bit of a roller coaster:

So perhaps DMRC and the new CEO were negotiating when the stock was in the teens in early June and thus the targets didn’t look quite that aggressive at the time, and they just didn’t readjust the targets for the new (lower) share price when he joined. There certainly could be something to that…. but I’d push back and note that even from a mid-teens share price the 2030 tranche still requires the stock to perform extraordinarily well (~30% annualized over 4 years; a ~3x in that time frame).

More importantly, I’d just note the sheer size of the upside… if the CEO could hit those share price targets, he’d be richly rewarded. Including the time-based vesting shares, his contract would have him earn >1m shares, resulting in a >$40m payday. All equity awards need to be put in perspective, but I mentioned at the top that the CEO would make ~$1m/year in cash comp. With a $40m payday on the line, I think it’s fair to say this is a contract that puts a heavy emphasis on getting the stock price higher!

Which is why this is such a strange contract / 8-K. The CEO is signing on for basically parabolic upside on the equity (again, the stock needs to 5x within four years for him to hit the top end payouts!), but he’s stepping into a company that’s filing a going concern warning? That’s quite the paradox!

What’s going to happen here? I have no idea. Could DMRC just be facing a short term liquidity crunch but the long term upside the CEO signed up for is still very much there? Sure! Could the CEO have been sold a bill of goods and be stepping into an epic disaster? Also sure! I’m no expert on the company…. but I have spent a lot of time on corporate incentives, and I don’t think I’ve ever seen one where the upside executives are playing for so clearly diverges from the short term realities of the financials.

A CEO giving up his operating role and remaining on the board is generally a sign of a friendly transition / some bullishness in the company’s outlook!

To be fair, the 8-K notes the customer is trying to get the programs recertified and, if successful, they may actually see a “substantial” increase in ARR.