Berkshire's secret? Do nothing when there's nothing to do (Trite Munger quotes that hit me, H1'25 edition)

I’ve got a few loose annual and semi-annual traditions1 on the blog. One of those traditions are my “trite Buffett” and “trite Munger” quotes series. The basics of these series are simple: both Buffett and Munger say a lot of stuff that is, quite frankly, trite. But part of their genius is that, every now and then, I’ll be working on something and a huge light bulb will go off that unlocks some deeper meaning for me in something I heard them say and laughed off 5-10 years ago.

Ironically (and as with so many things), Munger (and probably Buffett) were decades ahead of me in understanding the wisdom of things that sounds trite:

“Just because it’s trite doesn’t mean it isn’t right. In fact, I like to say, ‘If it’s trite, it’s right.’”

Back to the present. I will be honest: I had trouble selecting a quote for this post. Not because there were none that were speaking to me… in fact, quite the opposite! There were about 20 Munger quotes that I was interested in talking about!

One quote that I was sorely tempted to use was a Munger quote on envy,

The idea of caring that someone is making money faster [than you are] is one of the deadly sins. Envy is a really stupid sin because it’s the only one you could never possibly have any fun at. There’s a lot of pain and no fun. Why would you want to get on that trolley?

Why? Well, the past few months for the market have seen some absolutely wildly speculative stuff just rip higher. When that happens, there will always be someone who is getting wildly rich because they are implicitly or explicitly assuming some insane risk. It’s easy to get envious in that environment and/or do irrational stuff to try to “catch up;” neither of those choices is beneficial (financially or emotionally) in the long run.

So I was going to use that quote…. but I’d already discussed a similar quote in my 2023 trite Munger post!

I also considered using this one,

“It’s not that much fun to buy a business where you really hope this sucker liquidates before it goes broke.”

If you’ve been a regular reader of this blog (or particularly the ideas focused premium side) or listener of the podcast, you know much of my attention this year has been on “zombie biotechs” (pharma companies trading below cash). To date, the results of that strategy / focus have been more than satisfactory….. but I will admit that it is a little difficult to invest in a company and know that every day the company exists their value is diminishing2. Not a perfect fit for the quote, but I appreciate the spirit of it more and more every day.

But, ultimately, I decided to settle on this quote:

Part of the Berkshire3 secret is that when there’s nothing to do, Warren is very good at doing nothing.

I chose that quote for a few reasons…. but, before I do discuss the reasons, I’ll sidetrack and note that writing a blog is a bit of a flywheel: more readers creates more incentive to write. Substack statistics has been telling me for more than a year I do not encourage people to sign up for the blog anywhere near enough and it is hurting my readership, so if you are enjoying this (or any other) post, toss your email in the button below to become a sub (free or, if you’re really interested, paid!).

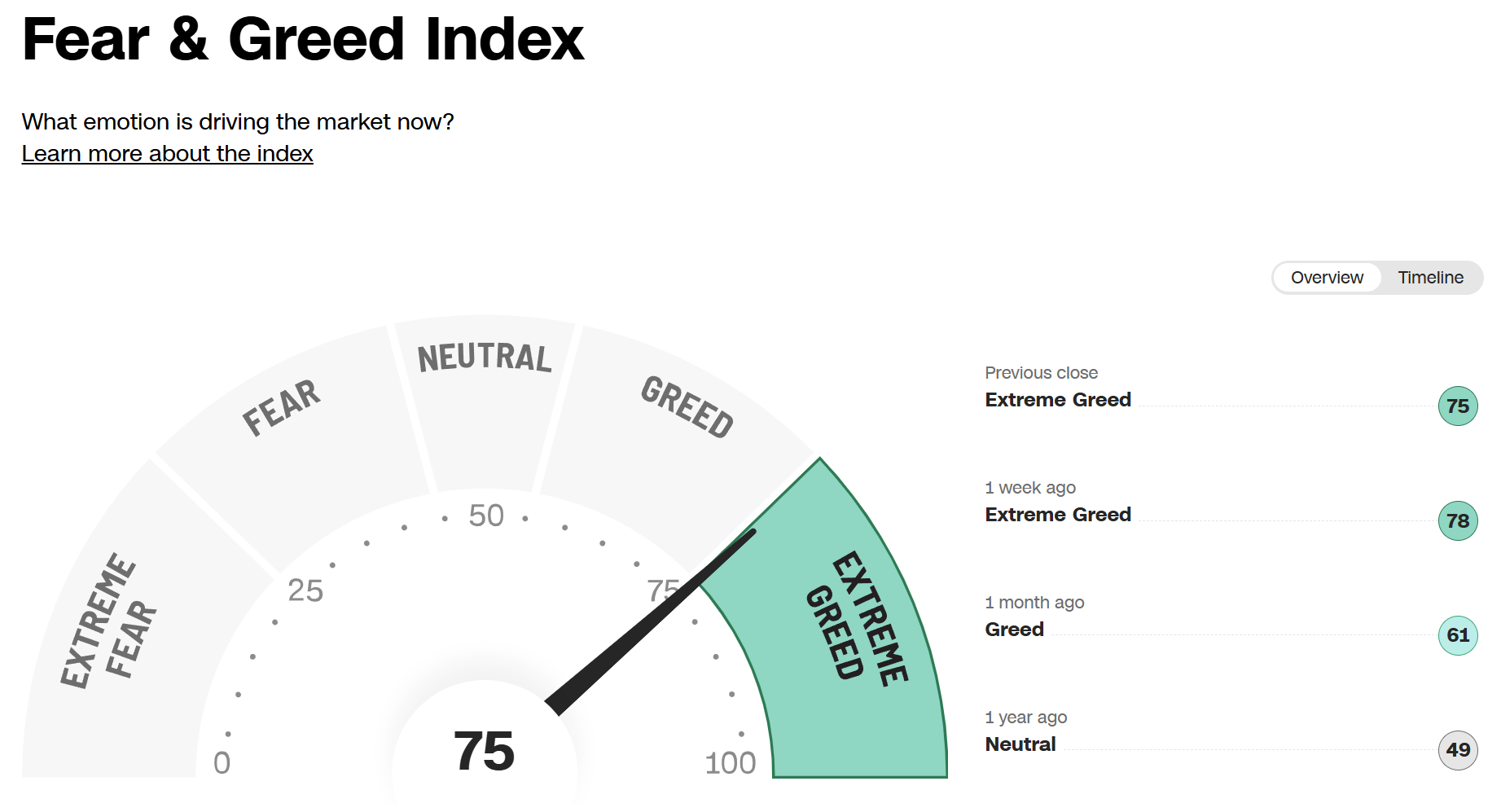

Anyway, back to the quote. The main reason I chose that specific quote is that markets feel really ebullient right now. CNN’s Fear & Greed index is tipping into extreme greed, and we’re seeing all manner of silly things just rip higher every day. The headliner of “silly things ripping” is obviously the seemingly infinite money hack of any company being able to transition to a bitcoin treasury company and instantly trade for 2x NAV, but there are plenty of others!

When markets are really racing, it’s easy to stretch as an investor. It’s one of the main ways you see investors have big stumble. Stretching can take a lot of forms, but one of the simplest / most common forms of stretching looks something like

You’re an investor with deep knowledge of a few sectors / companies

You’re not fully invested, or you’re fully invested in the higher quality companies in the sector (which tend to have the lowest betas)…. so when the market rips higher you underperform by a decent bit thanks to that low beta / cash drag

Then comes the stretch. There are a few companies at the edge of your universe that aren’t in your normal wheelhouse, but they’ve sat out the rally and look pretty cheap…. so you buy positions in them even though you would normally consider them low quality passes. Or there are a couple of companies in your sector that are generally regarded as the worst of the bunch…. but when things start to rip and they sit out the rally, suddenly their multiple looks really cheap comparatively. So even though a year ago you told yourself you wouldn’t buy those companies because their management teams are awful, you cave and buy them on the classic “they’re cheaper than everything else and due to catch a bid” thesis.

Something bad happens, the stock drops like a rock, and you look back and think “I must have lost my mind; I normally would never have bought that company!”

So I put that quote down as a nice reminder that just because markets are screaming higher does not mean you need to do anything; in fact, when markets are racing it’s probably better to raise cash (slowly) and head to the beach rather than stretch4!

Is that trite? Sure…. but there’s wisdom in triteness. It is really hard for driven, competitive people to sit by and do nothing as markets rip. I’m not saying that in a generic sense; I’m specifically thinking of myself when I write that. I’m generally an action oriented person, and my natural response to anything is “do more.”…. but the current market environment probably calls for doing less and getting ready for the next bout of volatility (whether that’s three months or three years from now!).

And it’s important to remember: it’s easy to tell yourself “do nothing” in response to markets getting more and more maniac….. but mania can go on for a long time. It’s easy to say “I’m going to sit on my hands and raise cash” when markets start to get maniac. And most investors will laugh off a quarter or two of underperformance if markets are ripping.

But what happens if a market goes manic for several years in a row? Can you handle years of underperformance waiting for mania to correct?

Most investors tell themselves they’d just stoically sit on their hands. But it ain’t easy. Clients redeem. The siren call to “swing the bat” and buy something gets louder and louder. Druckenmiller is a living legend and one of the world’s best traders…. but he started shorting the dotcom bubble a few months before the top, lost his shirt on the short, caved and flipped long, and then saw the whole market meltdown. If one of the greatest traders of all time can flap around like that, what hope do we mere mortals have?

So that’s the reminder…. but there is one other thought I wanted to explore.

As value investors, we naturally like to buy things lower. I mean, who doesn’t? Again, to hold the mirror up to myself, it’s much easier for me to buy something at $20 if it was $25 two months ago than if it was $15 two months ago. That’s almost certainly an intellectual failing / deficiency of mine. It’s one I’m always working to correct, but a small part of me is always going to yearn to buy things cheaper than they were a few months ago / buy at the lows.

That deficiency is always an issue…. but it’s particularly an issue in markets that are just ripping higher. In a ripping rally like the post-liberation day rally, basically everything is trading higher than it was three months ago, so my natural inclination is to pass on everything.

And I find knowing that I have that issue can play games with my mind. If a friend comes to me and pitches a stock that’s gone from $20 to $30 in the past few months, and I’m having trouble getting “there” on it… is it because I’m correctly identifying some risks? Or is it because I’m anchoring to a lower price? If I try to ignore those concerns, it it because I’ve correctly identified a mental bias in myself? Or am I letting a bull market get the better of me and starting to drop my risk standards to buy more stuff?

As with so much I write about, I have no easy answers here. Sitting on your hands and doing nothing when markets are ripping is sage (if trite) advice from Munger, but in practice it is much easier said than done on a whole host of levels!

I say loose traditions because they require me to remember them to continue them, and I’m ~50/50 on remembering!

Their value diminishes because every dollar of R&D and SG&A they spend is, in my opinion, negative expected value. That is not to say that every company burning cash is losing value; there are clearly companies burning cash that are creating huge value! But when a company raises hundreds of millions to invest in a potential blockbuster, that blockbuster fails, and the company decides to just plow that cash into a new drug or program…. well, in general, that’s a negative EV move to me!

Disclosure: a (very small) position in Berkshire

I obviously mean stretching as an investor. As I hit middle age, I’m rapidly seeing the benefits of actual physical stretching and mobility work!

Good post. I struggle with the mind games you mention towards the end of this article too. I find they get so circular and turned around, inaction ends up being the result. Whether that is a good result, I am not sure. Most instances of large stock declines, I'm usually wrong to average down. But sometimes, just sometimes, I see something the market doesn't. Those few instances prove fantastic buying opportunities and I think cause much internal deliberating and angst because you are always trying to figure out if the stock drop is one of those few instances. I've heard of personal investing policies to only average up. This might make sense from the standpoint that most of the time the market sees something I don't and its time to move on when a stock drops precipitously. However, it sounds like you have the same internal deficiencies I do where averaging up is a pretty painful exercise. You also probably miss out on those fantastic buying opportunities, which is just as painful. This is because you were ready to act on the share price decline, thought through it fully, but let your mental checks talk yourself out of it. But, this all goes back to the mental deficiency of trying to buy at the lowest, best possible price...

there certainly is confusion among competitive people.

but it is usually an inability to ever realize they have enough.

'stay wealthy' is a different mode, and minimal tweaks is a critical strategy.