Would I have been the patsy at $QVCPQ? $QVCAQ

Some thoughts on edge, resulting, and scar tissue now that QVC's prefs are zeroes

One time I was walking with a friend and their dog, and when we walked by a certain coffee shop the dog went nuts. Apparently like three years before the owner wasn’t looking and the dog had found a whole blueberry muffin or something on the sidewalk, and now the dog was convinced it would find a muffin anytime it walked down that street.

My style of investing leans heavily event / catalyst driven, and I sometimes worry I can be like that dog. If a certain situation or setup works for me the first time I’ll do it, I’ll get super excited every time I see it, and I worry that I’m getting excited not because the setup is actually edgy or actionable but because I “found a blueberry muffin” and got blessed by random noise / pure luck.

Now, I do hope I’m a little smarter than the dog, and if I do a situation once and “find a blueberry muffin there” (have good results) but then strike out ten times in a row after that, I think I’ll be able to course correct and realize I probably got lucky that first time rather than get excited about it for the rest of my life… but, even with that course correction, it can be a painful (and expensive) lesson to go looking for a muffin and come up empty ten times in a row!

A few areas that I’ve historically been really into but have gotten less interested after one or two initial successes and then multiple repeated losses in a row have been legal special sits, distressed equities, and levered buybacks. It’s funny I say “gotten less interested” in all three of those, because I am still very interested in all and actively looking at all of them and am currently invested in a few…. but a few years ago these were pretty much all I looked at and invested in, and today my bar for them is just much, much higher than it used to be because I’ve been hurt so many times.

Anyway, I write all of that because I just listed three buckets of historical interest (levered buybacks, distressed equities, legal special sits) and, depending on when you bought the stock, you could have gotten any of those interests filled by buying QVC (the old QRTEA). Yesterday, QVC had their bankruptcy plan confirmed, and the confirmation brought up some very old scars and a lot of questions for me, so I wanted to throw some thoughts down to deal with some old trauma.

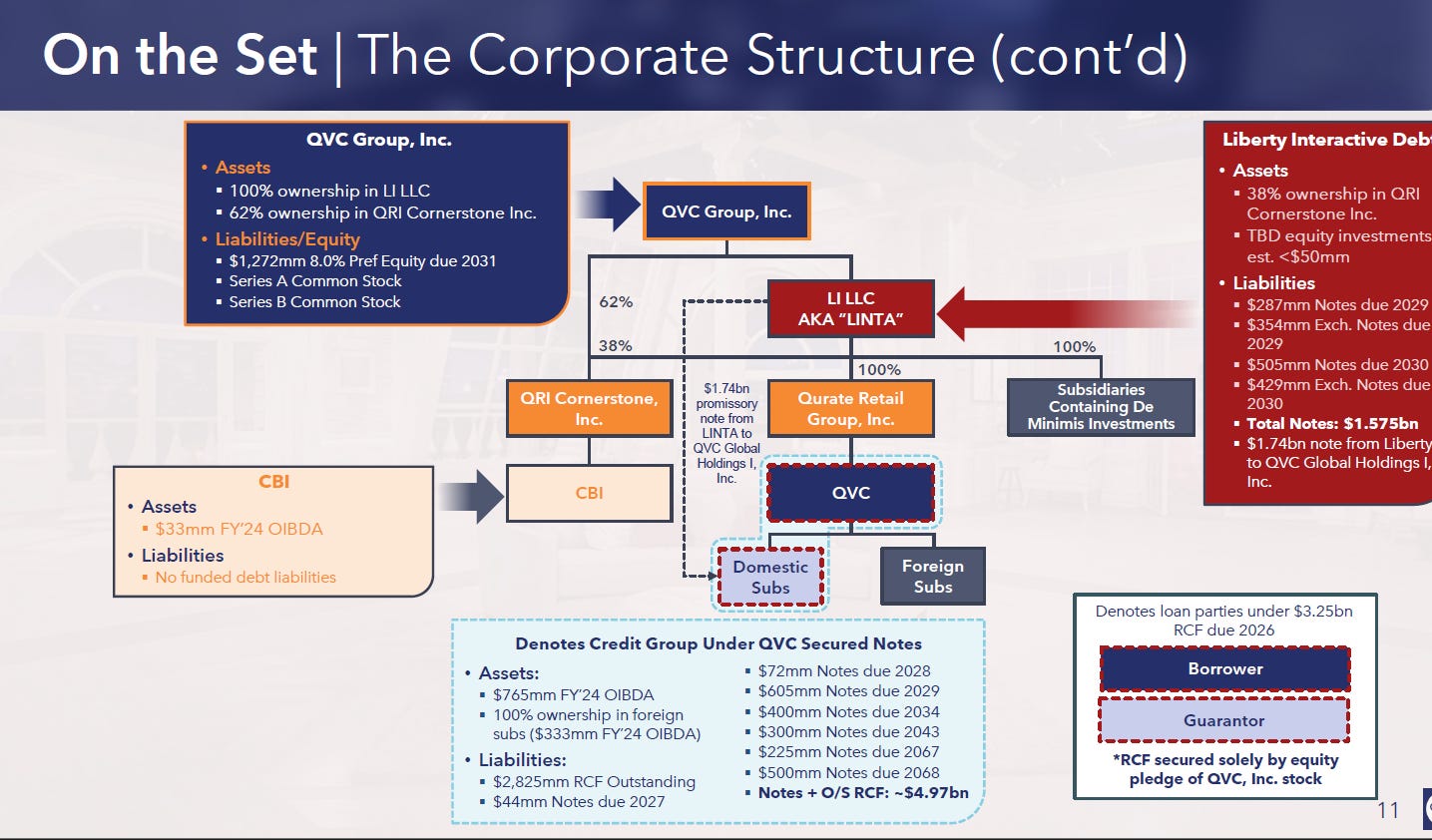

Some quick background will be helpful: after years of struggling, QVC filed for bankruptcy in April. The plan, as filed, wiped out all equity (common and preferred); that might sound typical for a bankruptcy, but QVC had a holdco structure with no debt at the holdco and hundreds of millions of assets at the holdco. This slide (from QVC’s day 1 BK pres) lays it out well; the prefs sit at the blue “QVC group” box that had no liabilities in front of them.

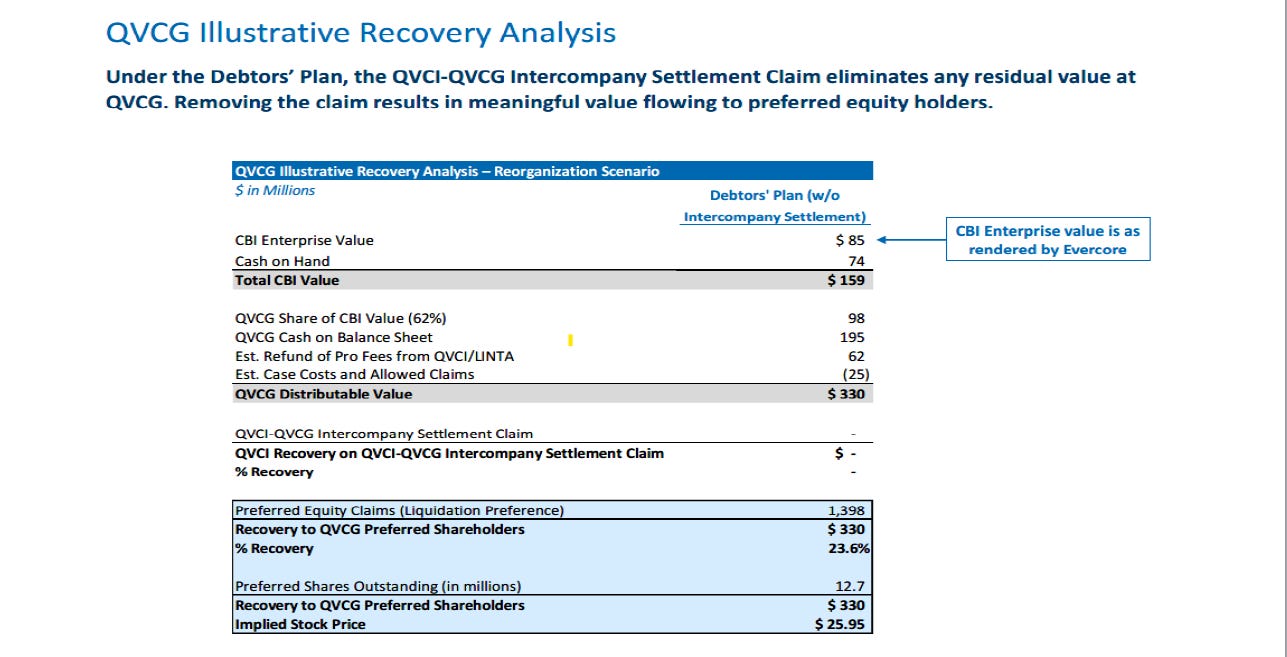

Given that structure, it seems like the prefs should have been entitled to a significant recovery (in the slide below, the prefs argued they should have gotten ~24% of face as recovery)…..

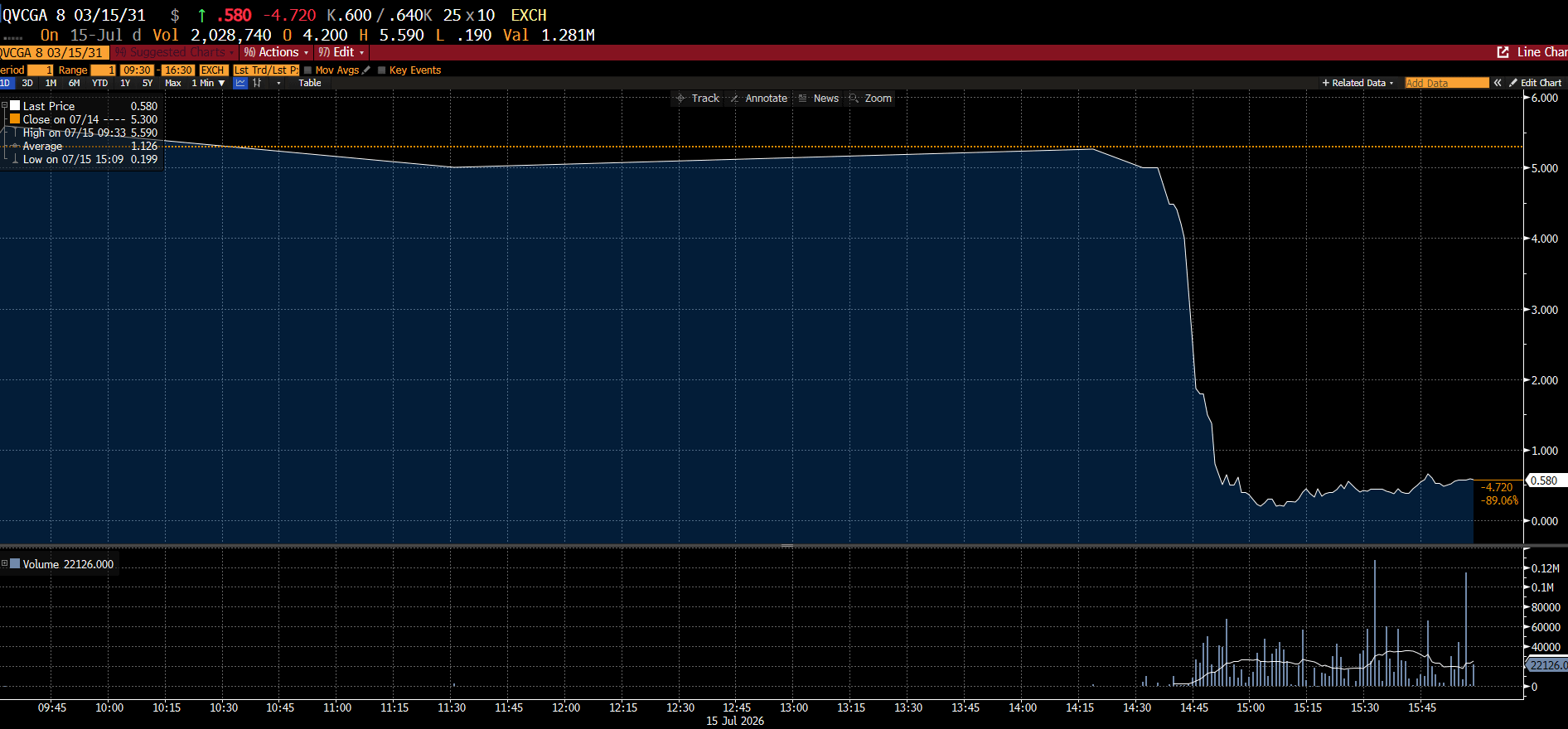

…but QVC’s bankruptcy instead allowed the operating company (where all the debt sat) to raid the holdco for assets and zero out the prefs. As my buddy century egg said, the prefs got screwed. However, prefs had one last hope: a group of them got together and protested the original plan, demanding that the prefs get the assets they were rightly entitled to. That hope had sent the prefs rallying…. until yesterday, when the court approved the original plan that zeroed out the preferreds. This was a pretty shocking turn; the preferreds had been trading >$5/share and dropped ~90% on the news. Absent a successful appeal (a long shot), they’re worthless.

The purpose of this article isn’t to recap the case or the ruling (though I will bias you and tell you I think it’s an abysmal decision; I will also admit my own bias because I had a lot of friends who were involved in the prefs, and I generally think their work here was very, very good (here’s a nice VIC write up with more background on the situation and set up if interested)). The ruling and the whole preferred saga have taken up a lot of my headspace over the past few months; the purpose of this article was just to get some of those thoughts out of my head in the hopes that you’d find them interesting / they might teach you something / they might make the voices in my head go away.

I’ve followed QVC for a long time, but over the past year I’d been monitoring it because I knew of the holdco structure and thought the preferreds could get interesting. On the day the company filed, the prefs puked and I started to nibble at shares (I believe I bought like 1k shares at ~$1/share)… but I kept thinking to myself “Andrew, this is a legal / distressed angle; do you really have edge or are you just a dog going back to his muffin spot?” I quickly sold the stock on the theory that I didn’t have edge here, and I stayed out of it from some combination of the “is this really your wheelhouse” question and some version of “QVC is paying their lawyers a hell of a lot of money; can this really be this big of a slam dunk if all of these high priced lawyers think they’ll get away with it?”

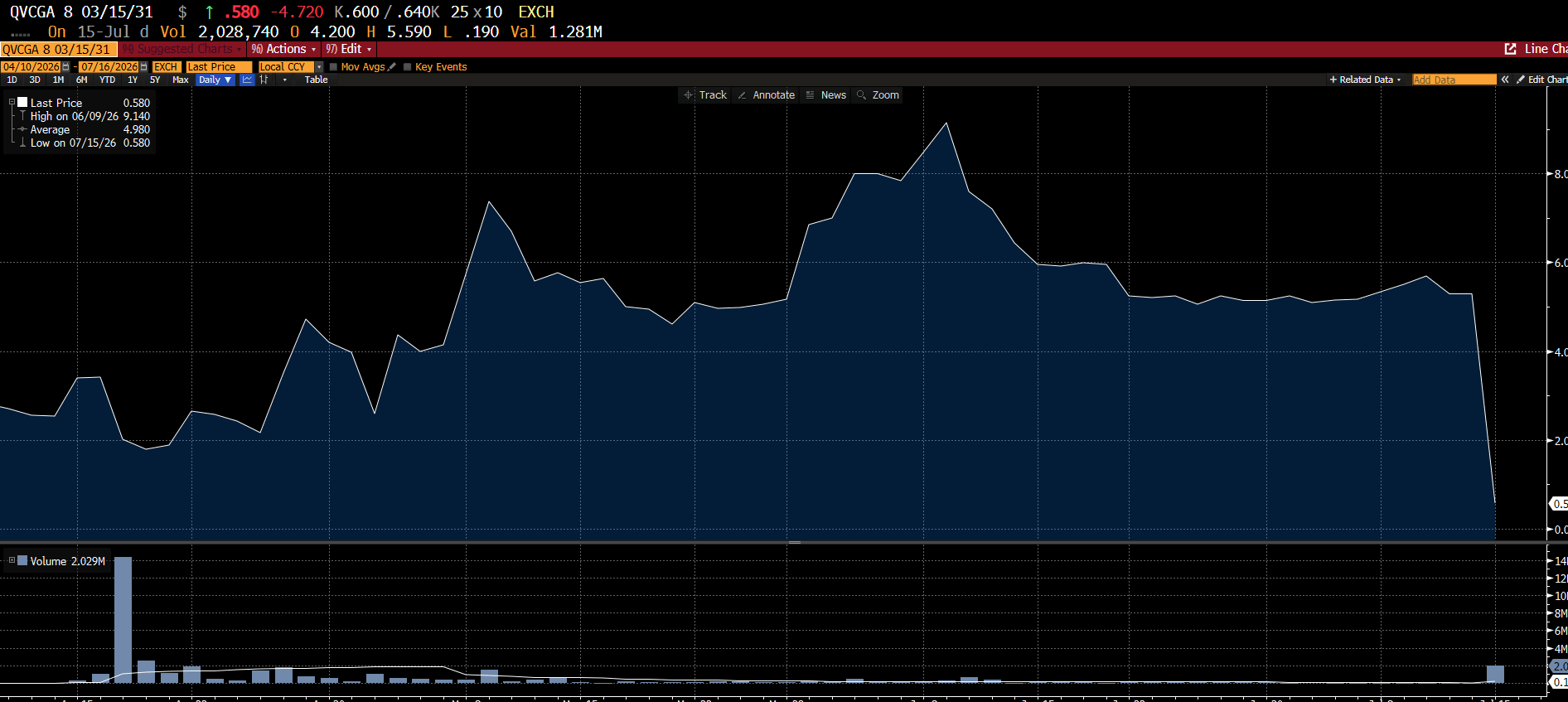

I then watched in horror as the prefs moved from ~$2/share to >$5/share in short order:

So here are the things that have been kind of floating through my head on QVC:

Given the outcome here, was I right to pass at $1-2/share? Or is that resulting; the stock went to $5/share in short order… there’s nothing that says you need to hold forever, and you can buy an option too cheap and cash it in when it’s fairly valued without waiting to see if it pays off or not. Given the massive asset value at the holdco and some shot of playing spoiler in the bankruptcy, isn’t it clear the option was too cheap right when the bankruptcy filing happened? Isn’t my pass inexcusable given that? Or does the outcome justify the pass?

As I go to write this, the preferreds are trading for ~$0.50/share. Even after the plan has been confirmed that zeroes them out, they have some value simply because of the appeal optionality (though, again, that’s a long shot). If that’s not an argument that the prefs were undervalued on the day of the bankruptcy filing just on optionality alone, I don’t know what is!

On a pure fairness basis, it’s hard to argue that the prefs were treated correctly here. But fairness doesn’t really apply in law; contract terms, precedent, jurisdiction, etc. are what matter. Those are all very specific things, and often investors on the outside don’t have the full information on them; some of them are provided to public investors, but some of them will be kept redacted or under seal. Given that knowledge gap, can an investor ever really have an edge in a legal situation? Is the answer the same for a non-lawyer (like me!) and a lawyer who should have some special skills in these areas? Honestly, I don’t know! Sample sizes are very small here; it’s very easy to make a massive return on one legal investment and think you’re a genius, but perhaps the dice just came up your way that time. Markets are insanely competitive; even if you’re a very good lawyer, why should your edge be large enough over 100 other very good lawyers to make continued alpha in legal sits?

To bring this back to the title of this post: there’s an old poker saying that if you can’t figure out who the patsy at the table is, it’s you. Every investor’s worst fear is being the patsy at the poker table. Distressed and legal situations seem so compelling because they are so idiosyncratic and the rewards to getting them right can be so high…. but they’re also very easy places to be the patsy at the poker table. Can you avoid being the patsy as an individual investor without a team of high priced lawyers? Can you avoid being the patsy if you have a team of high priced lawyers on the case? I’m not sure on either!

I’ll end this post the way I end so many posts: I don’t know the answers here. In fact, I realize this post is a little rambling / all over the place! But I was shocked by the QVC ruling, and I’ve been thinking about it a lot recently. Writing can be therapeutic, and I figured it was a win/win if writing this helped me get a lot of these thoughts out of my head while providing you (the reader) with a (hopefully!) interesting case study of a quirky event as well as some thoughts to chew on!