Work in progress articles and becoming an "industry expert"

One of my New Year's Resolution was to post more "work in progress" articles. In general, my "work in progress" articles tend to be on smaller positions where I still have lingering questions. My goal with "work in progresses" articles are to initiate a discussion around the company / position where people who have more knowledge than me / know the industry better can provide their thoughts. My recent post on Zayo (disclosure: long) serves as a great example of this:I saw something interesting with the company / situation, and several knowledgeable commentators came at the company from a different angle / provided useful inputs in the comments. Anyway, I wanted to break down a bit more on what qualifies for a "work in progress" article and how it's different than a core position. So to start, what falls into the smaller / work in progress bucket? I think I've mentioned this somewhere on the blog, but the way I generally think about managing a portfolio / portfolio sizing is in two separate buckets:

5-10 positions represent "core holdings" and are the majority (often, the vast majority) of the portfolio.

~20 positions that are sized much smaller. These smaller positions tend to be focused on special situations, but that's not always the case (and sometimes a special situation can get sized as a core holding). Still, for ease, I'll refer to this smaller bucket as the special situations bucket for the rest of the article.

I don't think there's anything crazy unique in that set up. We're in the heart of "manager letter" season currently (when every hedge fund manager releases and/or leaks their annual letter), and I find investors who tend to sit at the corner of special situations and value investing (which is where I place myself) tend to run similar portfolio structures to what I've laid out above: decent sized positions on core value holdings that make up the majority of the portfolio, with smaller "bets" on quirkier special situations (though the bets can grow quite large when the special situation lines up correctly / it seems there's not a lot of downside to the position), while investors who fall harder into the "deep value" camp tend to drop the special situations and focus their portfolio exclusively on the "core holdings" (i.e. if a value / special sits person might run 10 core holding at a 7% sizing each with the rest of the book dominated by special situations, while a more value focused managed would be more likely to run 7 core holdings at 15% each or something along those lines). That explanation defines portfolio construction, but what separates a core holding from a special situation? After all, if you really wanted to stretch, you could probably label any core holding as a special situation by identifying a few catalysts (however soft they are), or you could label almost any special situation a "limited downside / size the position up" holding if you squinted hard enough (That wouldn't be my preferred approach, as special situations are often fraught with risk and downside. Nothing here's investing advice though; you do you!). For me, in general, a core holding is a holding where I've done deep fundamental work on a company and think I completely understand the situation, the potential value, and the risks and rewards. It generally takes several weeks / months to hit the level of research needed here, as it often takes reading through all of a company's filings, their competitors' filings, and then rereading the company's filings to really begin to understand a company and the intricacies of an industry. The good news is that once you've done that work, the industry is pretty opened up to you and it's pretty easy to add competitors or similar companies to your circle of competence. An example might illustrate this best: earlier this month, I started to research Aercap (AER; disclosure; long a token position). Below is a slide from their Q3'18 earnings. The first time I looked at it, I was pretty confused. I knew or had a good idea what everything on that page meant, but in general the information was just gibberish to me. Is it better to have longer remaining lease terms, because it means you have more visibility? Or is it better to have shorter lease terms because you can release at a premium when the lease is up? What's a good annualized net spread, and should I be concerned that AER's dropped YoY in the slide below? Fortunately, as I began to dive in, I began to understand a lot better what these numbers meant and what were good / bad numbers (for example, in general, a higher net spread is better, but newer planes result in lower net spreads so you need to balance between the two). Once you understand those metrics for AER, it becomes a lot easier to go take a look to AL (their main public competitor) and value the two against each other / understand the difference between the two.

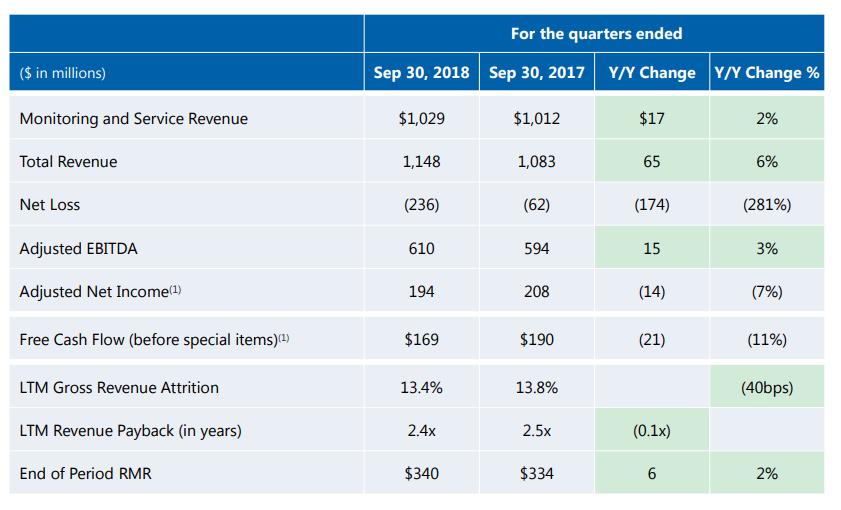

There are plenty of others examples of this type of lingo, both for Aercap or for other industries. For example, I spent some time looking at ADT earlier this month, and End of Period RMR is probably the most critical number to follow if you look at them and I had no clue what it was or what it meant for the company when I saw this slide.

Once you start diving into an industry, industry specific terms like RMR will become second nature to you. That's just one small piece of understanding an industry; as you dive further and further into an industry you'll begin to understand the different strengths and weaknesses of each company. The great thing about being an investor is this knowledge is generally cumulative: so if you've done deep work on one industry (i.e. the cable industry), it's generally pretty easy to apply that work to a related industry (the wireless industry or the video industry) that has some connection it. Anyway, for me a core holding is a holding that I've done that type of deep work on and feel like I've become an "expert" in a particular industry and on a particular company and think I have a significantly differentiated view of the company's value from the market. The way I generally judge if I've made that leap is from how willing I would be to hop on the phone and talk to anyone about the company and its strategy. If I haven't done enough work on a company and I get on the phone with a manager or someone who follows the company really closely, most of our conversation will probably end up with me asking relatively basic questions. If I've done enough work, then I can feel confident I could hop on the phone with anyone on the company and talk on "equal footing" with the other people / have an interesting debate about the merits of doing one thing versus another. For example, I'd consider myself a relative expert on cable: I'd feel comfortable hoping on the phone with anyone on the cable companies and talking about the relative merits of any piece of the cable industry (CABO's decision to focus on broadband instead of a video bundle, the threats of 5G, etc.) and we could both learn something from the conversation. Are there analysts with more knowledge of the cable industry than me? Of course... but at some point you run into diminishing returns from increasing industry expertise, and the point here is I could probably have a pretty deep conversation with anyone on cable. In contrast, I wouldn't consider myself an expert on ADT: I could talk for a second on RMR and the threat from cable companies entering their space, but in about five minutes a discussion with a knowledgeable analyst or ADT insider would quickly turn into me asking them basic industry question. That's a generally a waste of both of our times, and if I think that's the case then I know the company / industry isn't in my "circle of competence" yet. How do you become an "expert" on an industry? That's tough, but here's something that's worked for me recently. Choose a company and find their top three competitors. Get a transcript of their latest earnings call, their latest annual earnings call, their most recent investor day (if they had one), any M&A calls they've done in the past three years, and any investor conferences they've attended in the past year (this is easiest if you have access to CapitalIQ / Bloomberg / Factset, but there are other transcript services floating around that are pretty good and reasonably priced, or you could just listen to the webcasts online and take notes while you listen). Read them all (in conjunction with the earnings calls, read the corresponding earnings releases) and take notes while you do. Now, go read the introduction section for each of the companies' annual reports / 10-Ks. Then set up a news alert for those three companies and follow any press release / news they put out over the next month or two. Finally, after a month or two has passed, go back and reread all of the transcripts for the specific company you want to follow. I can't guarantee you'll be a complete expert on the industry at that point, but I can tell you that you'll be a long way there. And when you reread the transcripts the second time, I guarantee you'll pick up on things you missed the first time and you'll be surprised by how much easier it will be to think about the industry and the company you're following. I've done this with plenty of companies / industries, and I'm still amazed by how often I'll read through the transcripts the first time and a bunch of things will fly over my head, but when I come back around to the transcripts I'll be nodding along / understanding almost everything on the second read through.