Weekend thoughts: $NYCB and regretting sweetheart deals

There was lots of financial news last week (a FOMC meeting (which, by the way, I can’t believe how much time supposedly long term focused investors spend thinking about), META and Amazon smashing earnings, etc.), but nothing was more interesting to me than NYCB’s stock cratering (and the wildly spicy / fascinating earnings call that ensued).

I saw some pretty wild takes about NYCB on the heels of the stock collapsing. If you’re interested, the best thing I saw on the whole NYCB situation is from my friend Marc Rubinstein; I’d encourage you to check that out. I also really liked five point’s note on the issues, which came out right before I got ready to publish this but was good enough that I had to add a last second link to it!

For my money, there are clearly some credit issues at NYCB, but I agree with Marc’s general take: this was a largely regulatory driven issue. NYCB went over the $100B asset mark with their purchase of Signature last year. Going over the $100B mark as a bank has all sorts of new regulatory burdens: increased capital requirements, more rigorous testing of loans, etc. NYCB clearly thought they’d be given a few years of grace period to comply with the regulations given they had just bought a distressed bank; regulators were not messing around on the heels of all the bank failures last year and told NYCB in no uncertain terms they would instantly be held to the regulatory burden of a full $100B bank. Instead of being allowed to build capital and reserves over a multi-year period, NYCB had to do it all at once this quarter.

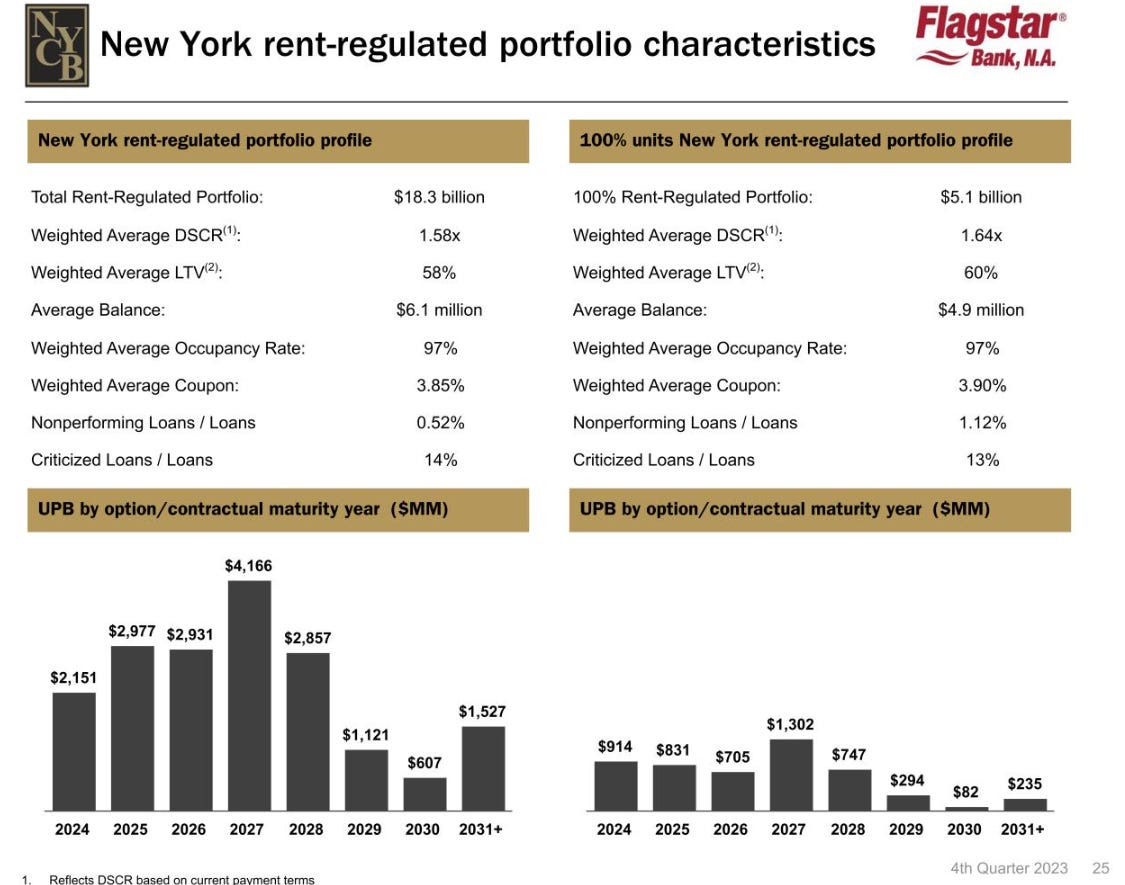

That’s not to say NYCB doesn’t have issues! But I saw lots of handwringing that I thought were much too draconian. Most of these concerns centered on NYCB’s large rent regulated portfolio; NYCB provided a bit more info on the portfolio below:

I’ve seen several people point to the Fed’s recent sales of Signature bank’s rent regulated loans and suggest that this portfolio is eff’ed. It’s tough for me to drill down to the specifics, but just using the high level info in the press release it looks like the fed sold signature’s loans for something around 70-80% of face value. NYCB has $12.3B of loans with >50% rent regulated units; assume those loans are worth 70-80% of face and NYCB is looking at ~$3B in write offs. With ~$7.3B in tangible equity, that write off alone would cut NYCB’s book value almost in half.

That math seems just way too draconian to me. To start, it’s worth remembering the fed has “a statutory obligation to maximize the preservation of the availability and affordability of residential real property for low– and moderate–income individuals” (source). In practice, that means the Fed limits the pool of buyers for these loans and imposes very specific operating restrictions / mandates on them, thus depressing the value of the loan. Even without those restrictions, loans are a rather illiquid security; you generally wouldn’t comp a huge forced sale of a pile of loans to the fair value of loans that could be sold in an orderly fashion (or, preferably, held to maturity)

NYCB just took their reserves way up and it’s worth noting that NYCB said on the call they haven’t really started to see losses in their multifamily book. I would not be surprised in the least if we eventually saw some issues in the multi-family / rent regulated book…. but I think calling for billions of losses in there is pretty wild. My guess is it ends up being very manageable: most of those buildings were underwritten with ~60% LTVs; assuming inflation and interest rates don’t spike again, I’d guess there’s still a solid sliver of equity underneath the vast majority of those loans and losses end up being reasonable. (Note: after I wrote most of this, I saw this analyst note clipped on twitter, which says everything I just wrote in a much more coherent and abbreviated form! I also saw this BB article right before I went to publish; obviously it paints a dire picture but if worst losses they are showing are 50% losses that suggests the majority of NYCB’s portfolio shouldn’t be too dire given they were underwritten to 60% LTV).

One last thing on the rent regulated portfolio: things can flip badly quickly given onerous regulations, inflations, and interest rate options that could reset into a much higher rate, so perhaps I am being too generous given the downsides possibilities…. but it’s just really hard to look at the stats they gave (~13% criticized loans, ~1% of loans nonperforming, etc.) and look at this portfolio and really think “yeah, we’re likely to see a billion of losses from it.” Again, anything can happen, and perhaps NYCB is being quite cavalier* with their criticized loans number…. but if I showed you the chart below in a vacuum I don’t know anyone who would think “yeah I’d guess all of those loans are worth 80% of face and are going to take a bank into distress”.

Anyway, there were three things that I found really interesting about NYCB that I wanted to focus on. They are:

The curious response of other bank stocks

How “sweetheart” purchases can turn into a nightmare

NYCB: Opportunity or disaster?

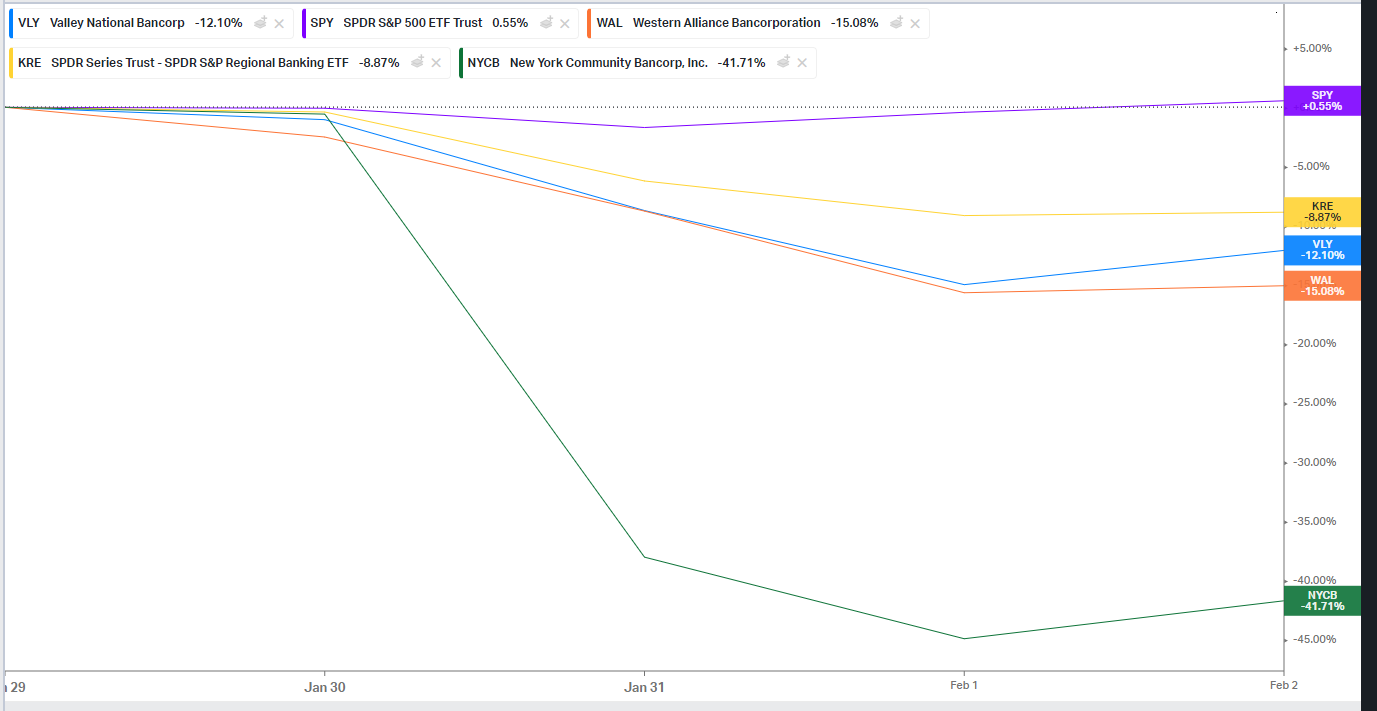

Let’s start with the first: the curious response of other banks to NYCB’s sell off. Regional banks were crushed by the NYCB announcement / sell off: with the overall market roughly flat, the KRE is down ~10%. Many peers are down more; for example, VLY is down ~12% and WAL is down ~15%. The reasons are obvious: people are worried NYCB is the canary in the coal mine and all of the banks are sitting on big CRE issues / about to report surprise write offs.

It is entirely possible we’re about to see an awful CRE cycle…. but what’s so interesting to me is that NYCB is one of the last banks to report, so we’ve already seen the types of loans and marks that other banks are taking! For example, both VLY and WAL reported Q4 results on January 25 (i.e. before NYCB reported). I’d expect banks in general would get murdered if one of the first banks to report earnings reported surprise write-offs / asset issues, as investors would (rightfully) start “shooting” banks that hadn’t reported on fears that the asset deterioration was broad based, not idiosyncratic. But, in this case, the peer banks had already reported earnings / discussed the trends in their loan book; investors had a full week to digest those and properly value the banks …. and then NYCB reported one or two bad loans and investors completely changed how they looked at the other banks loan marks / earnings. That seems strange and honestly wrong / an overreaction to me.

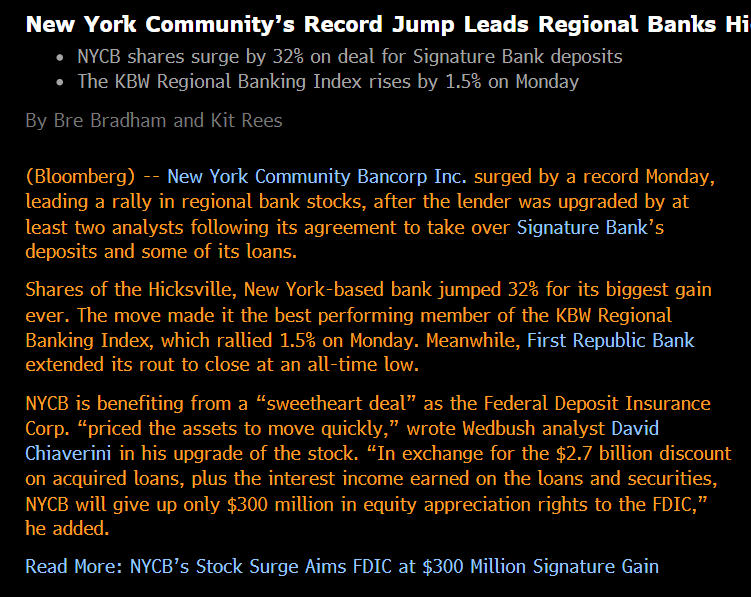

Second, it’s really interesting to look at NYCB’s purchase of Signature banks assets with the benefit of hindsight.

Remember, at the time, NYCB’s purchase of Signature was viewed as a huge win. Analysts praised it as a sweetheart deal, and the stock jumped 32%.

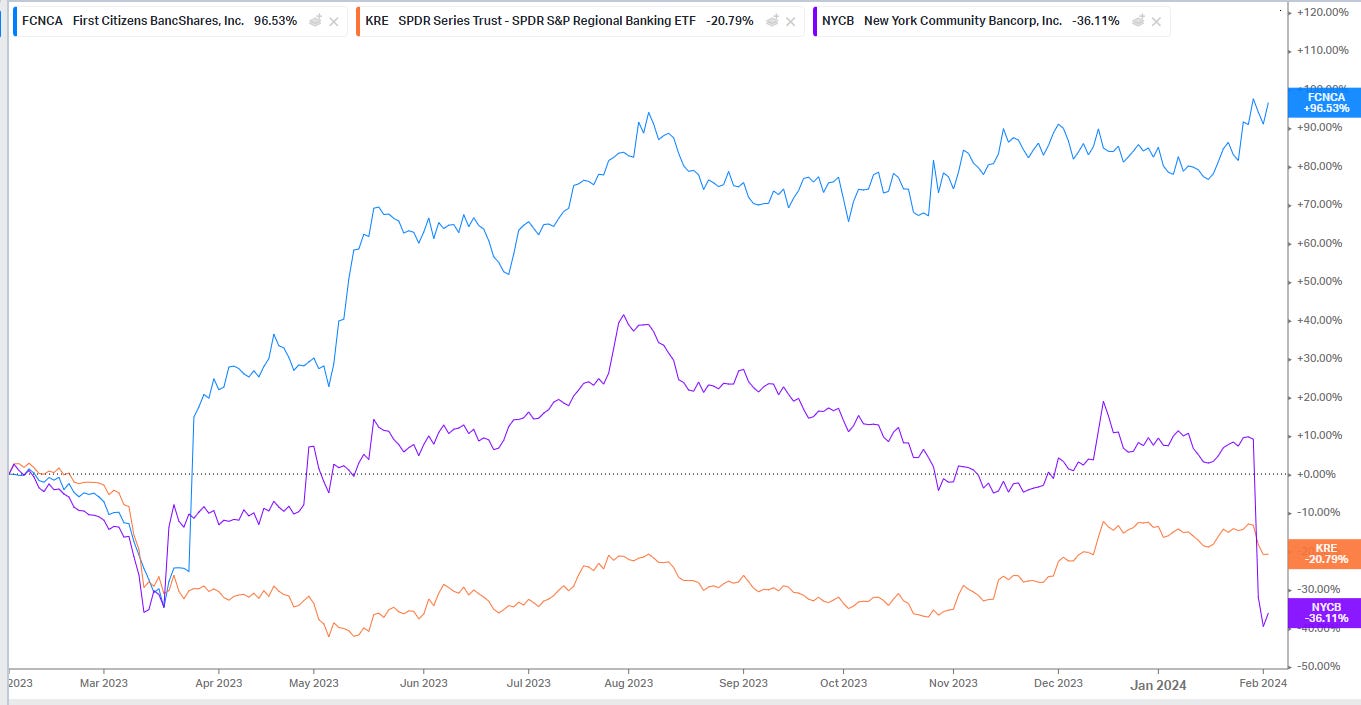

NYCB’s deal to buy Signature actually happened a few days before another “dream” deal: FCNCA’s deal to buy Silicon Valley out of bankruptcy.

It’s just so crazy how much things can change in a year. FCNCA’s deal is one of the best deals in history; the stock has almost doubled over the past year. In contrast,NYCB’s dream deal has turned into a nightmare: the bank has actually underperformed the index significantly over the past year, and a lot of the issues NYCB is having today can be traced back to the Signature deal (but certainly not all of the issues! Astute banking analysts have suggested NYCB had some skeletons in their lending closet for years, but the Signature deal and resulting scrutiny appears to have accelerated some of them).

Finally, I guess it’s just worth throwing out some thoughts on NYCB.

Gun to my head, I’d guess the sell off is an opportunity. After the Q4 reserve top off and write off, NYCB’s metrics look much closer to peers, and I’d guess NYCB knew the write offs and dividend cut weren’t going to be well received so they went ahead and ripped the band-aid off / were probably a little over conservative in their marks during the quarter. Maybe the company needs to build reserves / capital a bit more, but this is a bank with a solid deposit base trading way under tangible book value (Tangible book value here is just over $10/share; they’re trading for ~$6/share). Historically, their returns on tangible equity have been in the mid teens (for both 2022 and 2021, they did just shy of 15%); that’s obviously before a whole bunch of mergers and growth (which will increase capital requirements going forward and likely serve as a ROE drag), but given the deposit franchise and everything I see no reason why NYCB couldn’t do at least a low double digit ROE over the long term. At that earnings level, they’d warrant a slight premium to book value, creating a pretty interesting set up. Maybe it takes you a few years to get there, but you’d still end up with a pretty attractive IRR. Here’s some fun with math: if we use their current dividend, assume NYCB earns nothing this year (just assume all earnings go to topping off reserves / capital building), and then they average a ~8% ROE for the next four years and the stock ends up selling at 1.1x book value (because ROEs are trending up and you’re getting line of site to a double digit ROE), NYCB would do a >20% IRR over the next five years from today’s share price. That’s obviously in large part driven by the assumption that they go from almost half of book to a slight premium to book value, but still…. not bad!

Sure, it’s a simplification, but it’s a pretty attractive set up. What would keep me up at night with NYCB? Everyone is going to focus on the marks in the rent controlled book, and there is certainly risk there (though, as mentioned above, it seems a little overblown to me)…. but the more concerning thing to me is the company’s co-op loan write off. I’ve included what the company said about the write off on their earnings call below:

we had 1 co-op loan with a unique feature for piece funded capital expenditures. Although the borrower is not in the fall, we transferred the loan to held for sale in the fourth quarter and expected to be sold during the first quarter. Importantly, this loan is a one-off, and our review did not uncover any other co-op loans similar to this one.

If the loan is a one-off, why is that so concerning?

Because it makes no eff’ing sense to me that a co-op loan could result in a write off as large as they took.

I’m obviously not a real estate expert, and I’ve never heard of a co-op loan with pre-funded capex commitments that you’d need to fund when the project is flatlining so badly it’s going to result in a massive write off. I’m sure it’s a thing; that’s not what bothers me.

What bothers me is the size of the write off. To have a building under construction take a write off this big is insane to me; I’m honestly not sure how it’s possible short of some type of disaster wiping the property away (or fraud on the part of the developer). Given NYCB switched the loan to for sale / expects to get rid of it Q1, it seems that the property is still there / there’s still some value in the loan, so it doesn’t seem to be a disaster / mismanagement situation.

What was the loan? How is a loan taking this big of a write off?

Something doesn’t add up with that explanation.

From the outside, banks are black boxes. When management is saying something that doesn’t make much sense, it’s right to start questioning the entirety of the box.

Given the cheap valuation, as we go through the year and no more shoes drop, I’d guess the stock does well just given the huge discount to tangible.

But the discussion of the write-offs leaves me very, very concerned. And this is why I put that * behind the “quite cavalier” on the criticized loans number with the rent regulated portfolio; the big worry is that when you see management say something that doesn’t make sense, there’s another 100 things they are saying that you’ve accepted but that actually don’t make any sense / are covering something up. And, given how little sense the loan write off here makes to me, I’m worried there’s other stuff NYCB is saying that makes sense to me now but is actually too rosy.

That brings me to the last point I wanted to make. Everything in investing is opportunity cost, and NYCB at ~0.6x book is probably interesting if you can get comfy with those issues. But there are plenty of banks that don’t have any of the issues I mentioned above that trade at reasonable valuations. For example,

BANC took over a very distressed bank in PACW last year. At <$40B, they’re far from any regulatory asset level, they’re in a better capital spot than NYCB at >10% CET1, and they don’t have close to as much office or rent regulated exposure as NYCB. BANC trade for ~90% of tangible book; sure, NYCB is cheaper at 60%…. but BANC is forecasting 13% return on tangible equity exiting this year and NYCB is probably still going to be building reserves. Might be a case where paying up just a bit for a still cheap stock is a better bet.

Or, if you want to avoid integration in banks, here’s a pretty vanilla one (at least from my quick review): Veritex (VBTX) did ~14% ROTE last year and trades at almost exactly book value. You could underwrite some pretty strong returns over the next few years buying them without assuming any multiple expansion (though a bank doing a low to mid-teens ROE really should trade for a bit of a premium to book!) or needing to worry about the asset issues at NYCB. Insiders appear to agree; it’s nothing crazy but there’s been a decent bit of buying at VBTX over the past two years:

And that’s just looking at two banks; you could, of course, buy a business in a completely different industry! But I really just wanted to point to the VBTX and BANC examples because they highlight so well the opportunity cost for diving into a bank that’s undergoing some asset issues (like NYCB) versus looking at similar ones at reasonable but still cheap valuation (or at least appears to to me; I can’t say I’m an expert on VBTX or BANC!).

PS- again, most of the skepticism I was seeing / hearing about NYCB was on the rent regulated book. That’s probably justified given the Signature sale and how big the portfolio is…. but in many ways I’m more concerned by NYCB’s office loan book. Obviously NYCB knows there’s some issues here given the 8% reserve coverage…. but 38% of their office loans are criticized. That is an insane number; I can’t claim to be a financials expert but I don’t think I’ve ever seen a number / category with a criticized loan book that high! The office exposure is much smaller than the rent exposure, and maybe I’m being naive on just how bad things on the rent regulated side are…. but I wouldn’t be surprised if the loan reserves in office still had to come up a whole lot.

The size of the condo loan write down is likely not driven by credit at all but by the interest rate and moving the loan to loan held for sale. I gather the condo loan terms with pre-funding for capex were non-standard terms that don't meet NYCB's current lending standards, the loan was subjected to some regulatory criticism and so NYCB decided to sell it.