The house is losing: prediction markets vs. sportsbooks $CZR $DKNG $HOOD

If you’re a basketball fan, last weekend was probably the best sports weekend of the year, as you got the combination of the NBA entering the regular season’s home stretch before the playoffs and the first weekend of March Madness…. a truly magical time when we can all try to remember what state Gonzaga is in and root for a 16 seed to knock off Duke.

If you’re a basketball fan, it’s also impossible to escape ads for online sports betting this week. Every podcast I listen to has calls to go “get in the action” by downloading DraftKings or Fanduel, and the games are loaded with online betting ads as well12. Given that deluge of ads, those businesses have been on my mind over the weekend.

It’s crazy what a difference a year makes for these businesses. As I’m writing this post, prediction markets are taking enormous share and, without regulatory intervention3, may break the online sportsbook model. In contrast, a year ago, DraftKings and peers looked to have evolved into a somewhat rational oligopoly that was growing quickly and seeing explosive operating leverage and margin expansion thanks to exotic bets. Today, they look more like incumbents facing a cheaper, better-regulated substitute.

Why sportsbooks briefly looked fixed

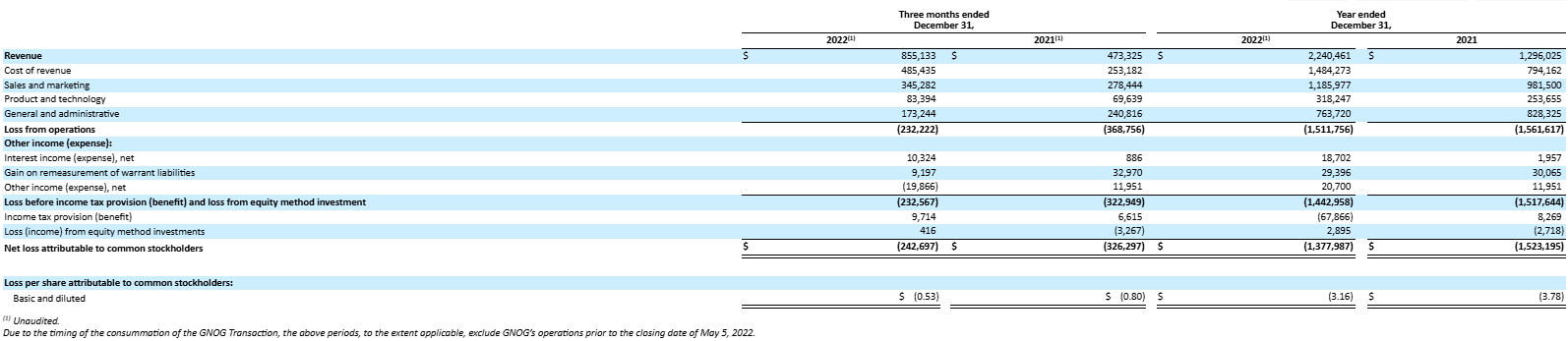

Some history might help here: when online gaming first got regulated / rolled out, there was a wild orgy of player promos (I’ve got a lot of nostalgia for the mania of the NYC launches!) and competitive launches cash furnace. If you were looking at the business in ~2022, it would have been reasonable to question if the businesses would ever earn a real profit; a quick look at Draftkings’ 2022 income statement shows why:

That’s right; Draftkings lost ~$1.4B on ~$2.2B in revenue. Even if you wanted to use their heavily adjusted EBITDA number (which excluded almost $600m in stock comp!), Draftkings lost more than $700m. Given players can switch from one gambling app to another with a click of a button, a large fixed cost base (huge marketing costs, massive payments to the sports leagues themselves for data streams and other goodies, and taxes in every state they operate in), it was fair at the time to wonder if these businesses would ever eke out an economic profit given they were currently operating as unrivaled money pits.

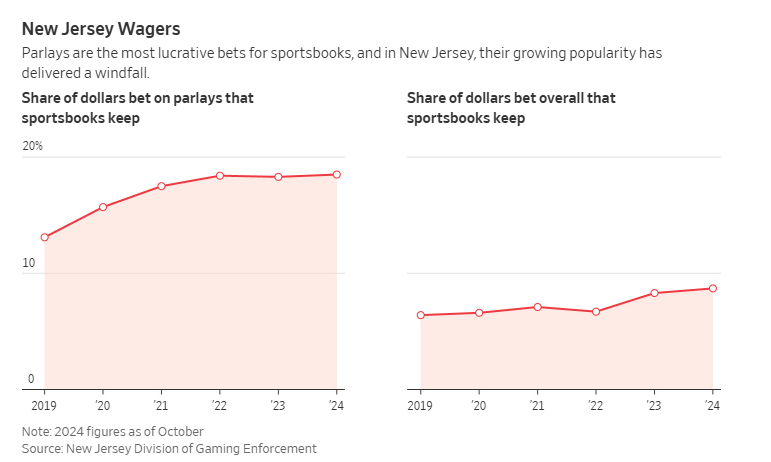

The business economics changed over the next few years, as the industry normalized their marketing spend, a lot of the smaller players decided to shut down their operations rather than continue to light money on fire (with the high profile ESPNBet failure probably serving as the headliner), and the gaming firms were successful in pushing customers more into higher odds (and more profitable!) exotic bets like parlays (margins on parlays are roughly three times as high as margins on generic bets):

Combine all of those factors, and the economics of the business got materially better: Draftkings did ~$180m in adjusted EBITDA in 2024 and over $600m in 2025 (on over $6b in revenue). So if we were writing this article and talking about the online gaming businesses last year, we would have been talking about how it had evolved into a rational oligopoly (DraftKings, Fanduel, MGM, and maybe CZR) and been wondering what end state margins looked like as marketing continued to rationalize, a new generation that was more comfortable with gambling continued to age up / increase in wealth, and the companies got even better at pushing bettors towards higher margin parlay style products.

My how things have changed; over the past year, the online gaming stocks have been absolutely crushed4:

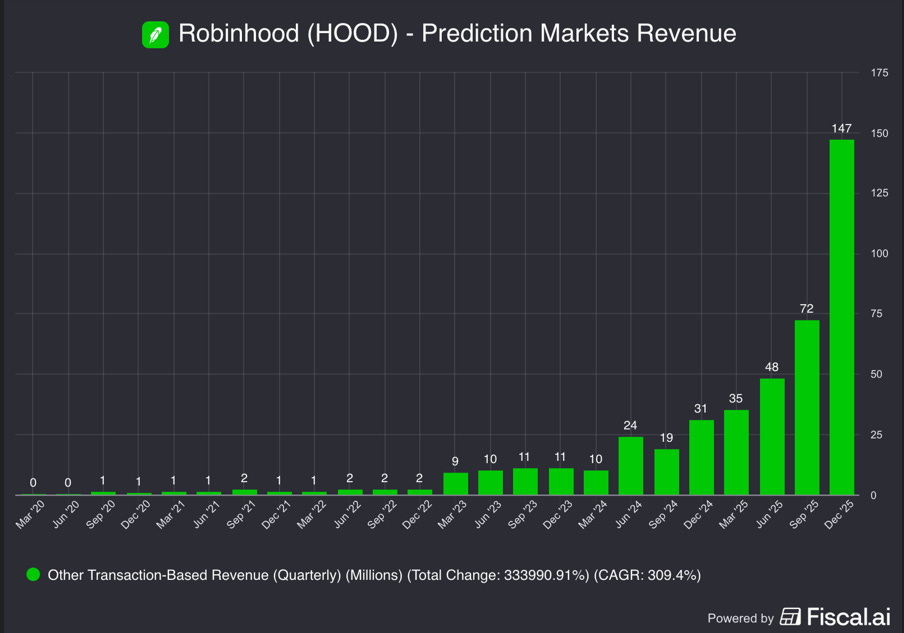

Why the big sell off? The main driver is obviously the rise of prediction markets. These things have come on fast; Robinhood has noted that prediction markets are their “fastest-growing product line by revenue”, and it doesn’t exactly take a scientist to look at a chart of Robinhood’s prediction market revenue and see this is a hyper growth business (revenue more than doubled quarter over quarter in Q4’25!).

Why prediction markets are a real substitute

Prediction markets are absolute death for online sports gaming companies for three main reasons (though there are others):

Destroys the oligopoly: remember how we talked about online sports betting’s profits getting better because the industry evolved into something of an oligopoly? Prediction markets absolutely shatter that status quo; now you have a flood of new entrants to compete for players again. Polymarket and Kalshi are obviously the headliners, but Robinhood, Interactive Brokers, and Coinbase have all gotten in on the action, and you have to imagine more competition can’t be far behind given the growth here.

Destroying the oligopoly hits margins in a ton of ways. The most obvious and hurtful way is companies start competing for customers by lowering take rates…. but it also increases your customer acquisition costs! MLB just announced a sports betting deal with Polymarket; Polymarket wouldn’t have even been in the running for a deal like that 18 months ago!

Way lower margin: Prediction markets simply take a fee every time someone, and the fee is quite low: polymarket’s fees appear to cap out around 1%, with many markets being free. That’s way, way lower than the online gaming companies; take rate for gaming companies are in the high single digits of each bet, with more exotic bets approaching 20%. A wager is a commodity: you don’t really care if you make the bet on Draftkings or Polymarket, so why would you pay $10 to make a $100 bet on Draftkings when the exact same bet would cost $1 on Polymarket?

Regulatory arbitrage: It’s worth noting that online gaming companies often have to pay a heavy tax burden to states, and so far prediction markets have dodged that burden. Thus, prediction markets truly dominate online gambling: they are lower fee, and their fees are lower than the online gaming companies can ever charge because they’re not paying taxes (for now!). (speaking of taxes, there may be tax advantages for consumers by betting on prediction markets versus sports websites).

Lower barriers to entry: This somewhat ties into the first two points, but being a sportsbook is expensive. You need complicated technology to price every bet, maintain balanced markets, hedge out your book’s risk, etc. That fixed cost creates a lot of fixed cost and gives huge advantages to the largest players / discourages new entrants. Running a marketplace is not that expensive; yes, there is a benefit to being the largest market (there’s a liquidity flywheel!), but the fixed cost of running a market simply isn’t that big.

Combine those three, and it’s not hard to see how prediction markets dominate online sports betting. And, despite the big sell off, it’s easy to see how there could be more downside ahead for the sports betting firms: DraftKings trades at >15x 2026E EBITDA, and that includes a healthy dose of stock comp add back. If you really believe that prediction markets are here to stay and dominate the traditional online sports option (as I laid out above), then DraftKings is a legacy business that is going to be a massive share donor going forward. It’s not hard to imagine a world where DraftKings is getting hit with a triple whammy: multiple continues to come down as people price in continued share donation and price competition, earnings estimates comes down as DraftKings donates share to cheaper prediction market companies, and margins comes down as DraftKings lowers take rates to try desperately to compete on price.

The only real bull case: regulation

Is there a long case for the online sports betting firms? Absolutely… but it rests squarely on regulation. It seems kind of insane that prediction markets, which are clearly gambling, are getting regulated and taxed like futures. I’d never want to make a bet on rational regulation in the U.S….. however, in this case, there are some incentives for the regulators to step in. Gambling companies enjoy powerful lobbies, employ thousands of people, and pay millions in taxes; all of that is at risk from prediction markets. If you’re betting on online gambling companies, you’re basically betting that regulators are going to step in and shut down prediction markets (or at least using prediction markets for sports gambling)5. In any other outcome, I don’t see how sports betting doesn’t become a permanent share donor.

Again, I’d never want to bet on rational regulation, but it’s really hard for me to see how regulators aren’t going to step in just given how much of their tax base is at risk (to say nothing of the obvious issues of insider trading on prediction markets, having policy makers making prediction market bets on policies they are setting, issues with defining outcomes, etc.)

Bottom line? If prediction markets stay open, sportsbooks are no longer growth businesses. They’re legacy toll booths under attack from a business model that is superior in every way (regulation, fees, taxation, speed, etc). It’s hard to define the general state of prediction markets and online gaming in any other way…. but the general state of the prediction markets and online gambling is actually not what I set out to write about when I started writing this article. What I wanted to write about is the CZR mini-bidding war (it appears Tillman Fertitta has outbid Carl Icahn and is in exclusive talks to buy CZR for ~$32/share). Why? Because

I find the recent history of CZR fascinating on a whole host of levels

CZR’s growth investments into digital serve as an interesting cautionary tale for investors and companies going forward

CZR selling in the low $30s would amount to an implicit admission that years of strategic investment created far less value than management promised.

So let’s dive in to that bidding war….

Keep reading with a 7-day free trial

Subscribe to Yet Another Value Blog to keep reading this post and get 7 days of free access to the full post archives.