The future of media free webinar $NFLX

Tl;dr: I’m doing a free, live webinar with AlphaSense’s director of TMT research on March 10th at 1 PM ET. We’ll be taking live questions from audience members, so it would be great if you can come join / discuss the future of media; if you’re interested, you can sign up here (a replay will also be available if you can’t make it live!).

Long time readers will know that I’m not a full out media expert, but I’m a passionate follower of the industry. Media blends so many different things I love (storytelling, business, power, politics) in a way I find completely fascinating. And I’m obviously not alone: media’s cultural power far outstrips its economic size. Paramount’s (PSKY) enterprise value is ~$26B (per Bloomberg). To put that in perspective, the “real-time billionaires” list suggests that there are ~90 individuals in the world who are worth more than Paramount and makes Paramount far, far smaller than even boring businesses like grocery giant Kroger (KR, ~$65b EV) or toilet paper king Kimberly-Clark (KMB, ~$45B EV)…. but Paramount’s public presence and ability to shape news and culture (through movies, CBS news, talk shows, etc.) gives them cultural relevancy and political power in a way that KMB and KR could never dream.

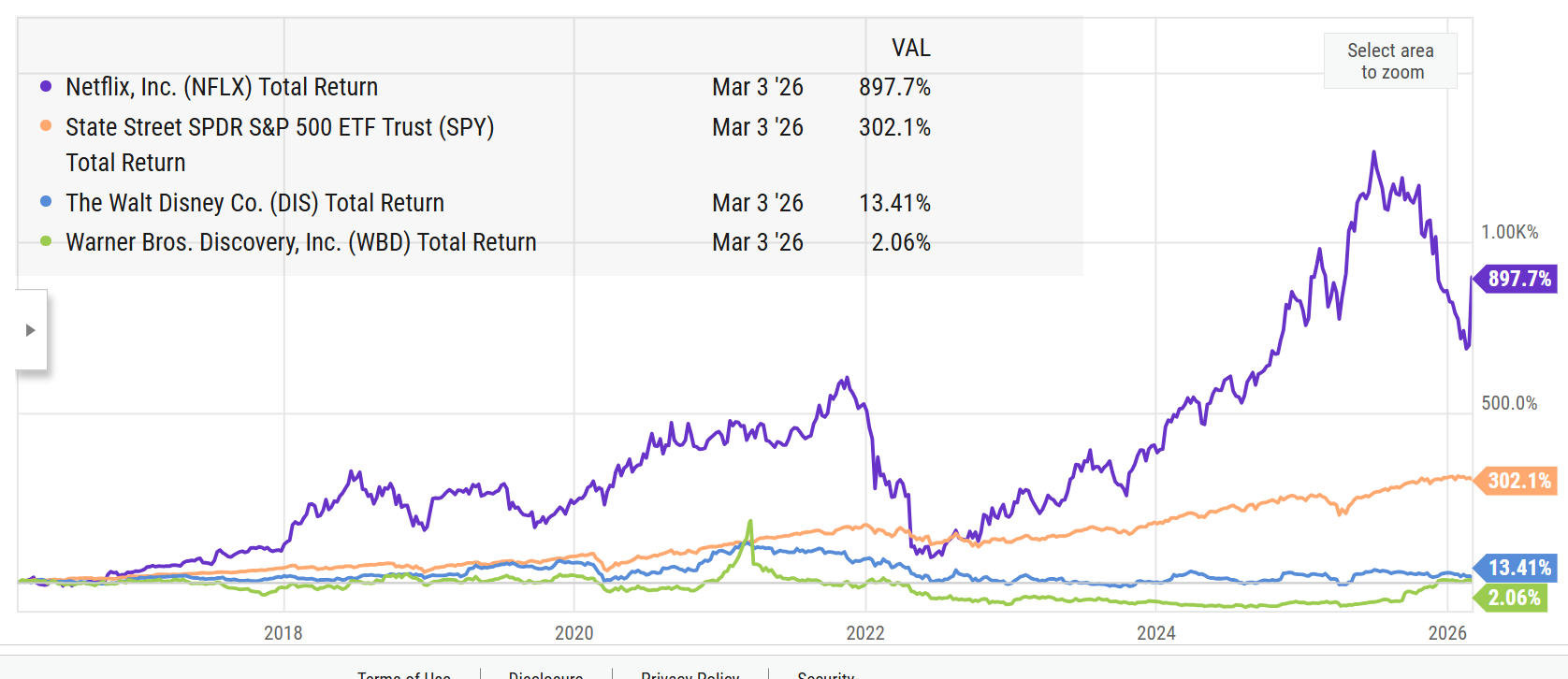

The media landscape has been dramatically shifting over the past ten years. The cable bundle was perhaps the greatest business ever invented, and it created a bunch of scaled winners in the media landscape with some of the strongest moats we’ve ever seen. The rise of streaming (and Netflix in particular) started to chip away at that bundle in the early 2010s; the market had its head in the sand about the model’s death for awhile until the infamous August 2015 earnings call when Disney noted they were seeing “some subscriber losses” at ESPN. Since then, basically every non-Netflix media stock has been a massive loser.

That history is what makes the current moment so interesting (and serves as the inspiration for the webinar!). The story of the past ten years has been Netflix’s inexorable rise as they ate the lunch of literally every legacy media player. It didn’t matter what legacy media did: basically every legacy media player eventually launched their own streaming service, and we saw a wave of consolidation (after splitting years earlier, Viacom and CBS recombined to eventually form Paramount, Disney bought Fox, Discovery bought Scripps and then Warner Brothers) and nothing could slow Netflix or reverse the decline for the legacy media players. The stock chart tells the story nicely; over the past 10 years, Netflix stock zooms higher and smashes the indices, while the legacy players not only dramatically underperform the index but basically underperform cash over the same time period.

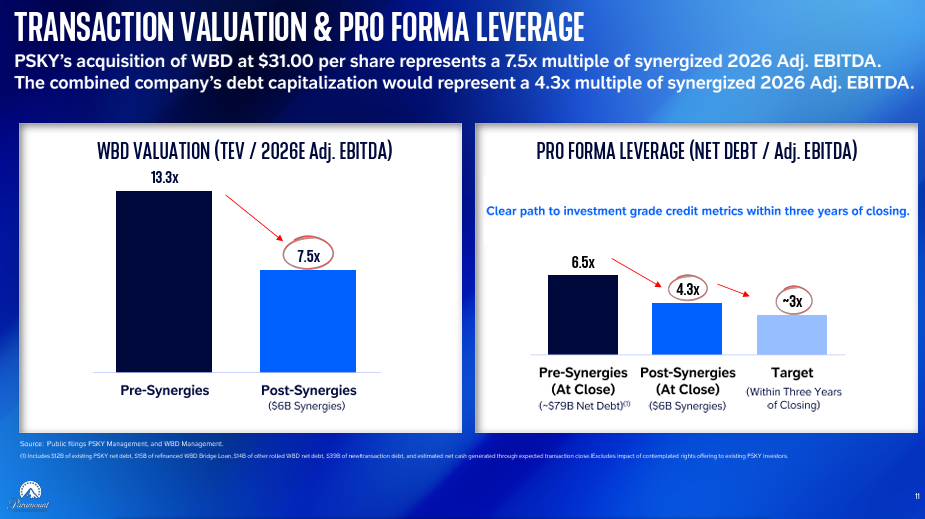

That background sets the stage for why now is such a fascinating time for the media sector in general and this webinar in particular. We’re coming off the heels of one of the great bidding wars we’ve ever seen, with PSKY ultimately topping Netflix (and Comcast) to buy WBD for $31/share, a ~150% premium to WBD’s unaffected price1. The whole saga was fascinating, but it leaves more questions than answers.

On the heels of this, I’d say Netflix has the most questions to answer. After stomping all over the legacy media sector for the past ten years, why did they suddenly decide to buy into the sector? Yes, I’m sure their scale meant a WBD deal may have been attractive, but Netflix is a company that has historically been averse to acquisitions. They had done only a handful of minor acquisitions in their entire history, and NFLX’s current co-CEO admitted that Netflix’s founder was “more in the build vs. buy mode” and “not an enthusiast about these kinds of deals.” It seems like a wild stretch to go from “we build things” to “let’s complete one of the largest acquisitions in history.” When Netflix looked at the playing field for the next ten years, why did they think they needed to buy now? Was it really just this deal made sense economically on its own? Or were they seeing signs of weakness in the core Netflix business that they thought they needed to address? Perhaps they thought the continued rise of AI might shift even more power to the most elite IP, something Netflix is woefully short on but WBD has in spades?

Netflix also faced enormous political pushback in the wake of their announcement to buy WBD2. Did the amount of pushback Netflix faced reveal anything? Will it have any impact on Netflix’s strategy going forward?

Then we turn to the “winner” of the WBD bidding war, Paramount. I use winner in quotes because Paramount faces the issue of the “winner’s curse” on steroids. First, history is not kind to companies that have purchased Time Warner. AOL, AT&T, and Discovery all bought Warner Brothers over the last twenty years. All ended up regretting the deal; AOL and Discovery took huge write downs on their deals, and T was eager to get out of the business. History is also not kind to companies that win media bidding wars; the best case outcome for a bidding war is undoubtedly Comcast buying Dreamworks (there were rumors Softbank or Hasbro were interested). Outside of that one example, it’s hard to find a single successful example of a media bidding war that ended well. Disney would probably do the Fox deal again despite some large write offs in the Indian operations, but, for every single other bidding war example that I can find or think of in media, the bidders would want happily take a mulligan if given the chance. Comcast wrote down >20% of the purchase price of Sky, Amazon paid $8.5B for MGM and still hasn’t gotten a Bond movie of their own, and the 90s were rife with media overpays that ended up destroying companies (ironically, Viacom nearly destroyed themselves buying Paramount in the mid 90s).

The newly combined Paramount / Warner Brothers will face lots of questions. Chief among them: how do they avoid the fate of Warner Brothers Discovery before them? Warner Brothers’ finances were a mess when Discovery merged with them, and the WBD team had to focus on generating cash to the exclusion of basically everything else in order to service their debt post-merger. Paramount is suggesting they can find $6B of synergies in the merger; that’s an enormous number that’s almost equal to WBD’s standalone EBITDA. I don’t doubt Paramount can find that much cost to cut; the question is whether they can do it without impacting the core business.. There, I’m not so sure!

There are interesting questions for the other standalone players on the heels of this bid as well. Comcast made a bid for WBD, though I don’t think it stood a chance given its structure, but the standalone NBCU looks awful small when you put it up against Netflix, PSKY / WBD, or Disney. What’s plan B for them when it comes to the media business?

What about Apple or Amazon? They’re both burning a lot of money on their video businesses to varying degrees of success; are they happy to have their services be nice supplements to the main players, or do they want to think about buying someone else and turning these into real businesses?

How about poor Versant? No one caught more strays than Versant during the WBD / NFLX / PSKY bidding, as PSKY would basically mock the VSNT’s assets and valuation at every turn. With the playing field generally set, what does that poor company do as it looks to stand on its own two feet?

The other really interesting angle on the heels of this bidding war is what is going to happen to sports rights for a bunch of the leagues. The headliner here has to be the NFL (of course). I’m not sure people are ready for how crazy the numbers might get for the next set of NFL rights. Right now, the majority of NFL rights are carried on CBS (Sunday AFC games), Fox (Sunday NFC games), NBC (Sunday night), and ESPN (Monday night)… though ESPN shares with ABC quite a bit. I’m not sure if ESPN and Fox have a reason to exist without the NFL at this point; yes, I know ESPN has some baseball and the basketball package, but just look at their programming. Football is the draw and they know it. If ESPN doesn’t have football games, does that channel even work anymore? And Fox’s lineup is basically the Masked Singer, some Gordon Ramsey shows, and football; if they lose football, what do they have to go to affiliates or distributors and say “this is why you need us.”

So that’s two bidders who will face an existential crisis without the NFL…. and honestly I think CBS and NBC are not far behind! How wild are the bids going to be if two of the four bidders have their literal business on the line when it comes to keeping a package? And then consider new bidders: Amazon seems to be getting the stride of running NFL games and pretty pleased with how the NFL is performing for them; would they want to come in for a package? Netflix continues to say they don’t want to do full league schedules, but they also said they’d never do ads, and their Christmas day NFL games were a hit.

Honestly, I could go on and on. I find the absolute implosion of RSNs fascinating, the non-NFL / NBA sports leagues face very interesting futures, short form videos impact on media is still being felt, and I would not be surprised if AI content kills off some genres of media in much the same way Farmville may have killed soap operas.

Lots to talk about. I’ll see you for the webinar on Tuesday

And honestly the premium is bigger once you add in the break fee PSKY covered WBD paying to NFLX.

Netflix continues to say it was “completely normal” pushback, but I would suggest that’s poppycock