Take the win (and one exception) $TASK $STAA

Every now and then, I’ll make my displeasure known about a merger that I think is priced too cheap, or I’ll send a letter to a board about a situation where a sale is needed. Because of that, once or twice a month I’ll have a shareholder reach out to me about a setup where a company is getting sold for a price the shareholder finds disappointing.

My advice?

Take the win.

Most of the complaints I hear about sale process / premium come on a multiple / valuation / cycle argument. Examples might show this best:

The company is being sold for 10x EBITDA, and I think it is worth 12x EBITDA

The company is selling right before their big product launch that will create a ton of value!

The company is selling for $35/share and I think they’re worth $50

Now isn’t the right time in the cycle to sell (note: the “cycle” here could refer to the overall macro cycle or a specific industry’s cycle)

I completely understand those arguments, and it’s natural to feel jilted when a company is sold for less than you think it is worth.

But my personal rule of thumb is pretty simple: if the company ran a full and fair process and decided to sell to the highest bidder, it’s best to just take the premium and move on. Yes, maybe the company is about to launch a new product that will be gangbusters…. but maybe management is deciding to sell now because they are seeing worrisome signs about the launch and want to shift the risk onto someone else? Or maybe the company is getting rumblings of a new competitor coming in that will increase their capex cycle and decrease sector returns, and they want to sell before seeing the impact of the competitor?

Obviously every situation is different, but I will just note that I have seen way more situations where investors rage against a sale at a huge premium, vote it down, and then come to regret that vote than situations where investors vote against a deal and see the stock fly higher later. In fact, the reason I’m writing this post is because we’ve seen news in two recent situations where I bet shareholders wish they could have a do over.

But, before we get to those recent situations, let me start with perhaps my favorite example because it has such a happy ending for shareholders (though, as this story will note, the happy ending may not have been deserved). Way back in 2021, H&F entered an agreement to buy At Home for $36/share. The deal included a go-shop, which was unsuccessful. Several shareholders, led by CAS, pushed back on the deal as “grossly” undervaluing HOME.

Now, I had just started the podcast at the time, so I was new to having a (small) public presence1 and the type of things people would pressure you to shine a light on…. but I could not believe how many inbounds I got from furious (largely retail) shareholders suggesting HOME was getting stolen and asking me to write a letter to the board / use the mini-podcast platform to help (further) organize a campaign against the deal2. I mean, these were furious emails. One emailer got me on a call and told me the whole board should be thrown in jail for taking anything under $90/share3 and that he was going to try to find a way to hold them all personally liable.

That pressure campaign had a happy outcome for shareholders. H&F bumped their bid to $37, and the deal closed a month later…. but it had a much less happy ending for H&F. The COVID home goods boom ended soon after the deal closed, and HOME was quickly in distress as it burned through an enormous amount of cash. It eventually filed for bankruptcy last year (perhaps with a nudge from the trade war).

Look, it’s entirely possible things go differently for HOME if they don’t have the leverage from the take private…. but I’d suggest the shareholder who wanted the board tossed in jail for taking such an “awful” deal should be sending them some gift baskets for saving him from himself.

Anyway, that’s my favorite historical example just because I think about the furious emails about stealing the company and the ultimate result all the time when I’m thinking about not looking a gift horse / big premium in the mouth. Let’s turn to the current examples.

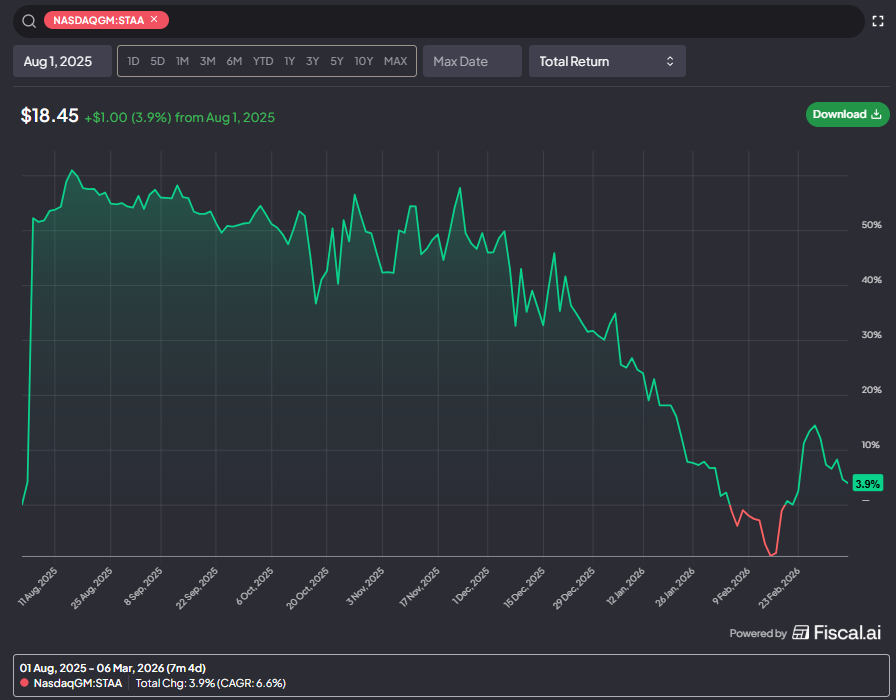

The first is STAA. I wrote about STAA late last year, so I’ll refer you there for a full breakdown but a quick recap is they had entered an agreement to be sold for $28/share to Alcon. Shareholders were not a big fan of the deal, as the company’s stock had been hammered by recent results, and shareholders thought the company was selling at a cyclical low. Alcon eventually bumped the deal price to $30.75/share even after STAA couldn’t find a better bidder, but shareholders eventually rejected that bid too and the deal was called off. Management then basically handed control of the company to the largest shareholder.

Did shareholders make the right choice here? It’s too early to make a firm judgement here; the company hasn’t reported a single quarter under the new board’s stewardship yet! However, I’d suggest that current results leave a lot to be desired. Their Q4 results were weak, and while the company is “optimistic” about the business in 2026, my math suggests it takes a very rosy outlook / rebound over the next few years to even begin to compensate for the lost “bird in hand” of the $30.75/share Alcon bid. And that’s just talking business fundamentals; on a mark to market, with the stock currently trading for ~$18/share (roughly flat with where it was before the merger was announced), I would certainly want a mulligan on taking the Alcon bid if I was a shareholder!

The second topical example is TASK. This is timely because late last month they concurrently announced earnings, a big refi + special dividend, and a CFO transition.

Last May, Task announced a deal to be taken private by its co-founders and Blackstone for $16.50/share. The company noted that their business would be significantly impacted by AI, and going private would give them the chance to make needed changes to keep up.

Shareholders were not happy, and I admit that I have a lot of sympathy with shareholders here. Blackstone and the co-founders basically said, “we won’t sell to anyone else; take our deal or accept an uncertain AI future.” That is not a good process and exactly the type of thing shareholders should generally try to stand against. And stand against it they did; shareholders voted the deal down and TASK and Blackstone eventually backed down and broke the deal.

However, TASK’s business is getting rapidly disrupted by AI, and their recent earnings reports make it seem like the business has stalled out. When a business is getting disrupted, it’s not a far throw from “stalling out” to “rapidly shrinking”, and TASK’s share price is perhaps foreshadowing the latter is likely to happen.

I admire TASK’s shareholders for standing up to a flawed process, but when they pushed back on the deal last summer and the company published a note asking shareholders to vote for the deal and noting4 that the buyer had repeatedly refused to increase their purchase price in light of the shareholder frustration, that may have been a signal that all was not alright at the company and they should have just taken the bird in hand and thanked their lucky stars.

Just to wrap this up, I want to again note that I’m not saying “always take the premium and walk away.” But the time to fight a takeover is when there is a flaw in the process, not when you think your excel output is better than the company’s. So if a company’s CEO is buying out shareholders and refused to give anyone other than his preferred private equity partner a look while he’s getting to roll his equity for a song, that’s a good reason to fight a deal. If a company refused to engage with a logical bidder because management hated them and carried a personal vendetta, that’s a good reason to fight the deal.

But history suggests if a company is selling for $10 and you’re furious because you think the company is worth $12 or even $20…. absent a flaw in the process, you’d be better off just taking the $10 and finding something else to invest in.

As I say all the time, I can’t believe how dumb I was then.

I could not believe it both because the process seemed fine to me, so I was surprised so many people were mad, and I simply could not believe the pure number of (again, largely retail) investors who were ready to burn it all down to fight to keep their HOME shares.

Memory is a funny thing; I’m pretty sure he was arguing for $90, but it sounds so crazy in retrospect maybe I’m misremembering and he was arguing for $50 or something

The full quote: “Since the announcement of the transaction, the Special Committee of the TaskUs Board of Directors (the “Special Committee”) and the Buyer Group have engaged in discussions with several stockholders concerning the proposed transaction. In light of AI’s impact on the Company’s business and its future prospects, the Special Committee continues to believe that the proposed transaction is in the best interest of TaskUs stockholders and recommends that stockholders vote “FOR” the proposed transaction. The Special Committee has not received a non-binding proposal from the Buyer Group to amend the terms of the merger agreement to be more favorable to the Company’s stockholders unaffiliated with the Buyer Group.”

Love the piece. The HOME story is the perfect illustration — shareholders were convinced it was worth far more, fought the deal, got a small bump... and then the company went bankrupt. Their valuation was never realized. Having a number in your model and having the market ever price it there are two completely different things.

Alcon has a significant number of local distribution channels that STAA could have leveraged in China if the deal had gone through, and STAA even made changes early in 2025 to facilitate its greater collaboration. It will be interesting to follow the new management's strategy for taking the business to new heights alone, in light of the significantly different domestic competitive landscape post the 2024 approach, given the domestic certification and market entry of Loong Crystal's products in 2025.