Starting the year with some forced selling cleanup: $NTP

I mentioned it over the weekend, but I’m really looking forward to 2022! I’ve got some slight tweaks and changes to all of the pieces of my YAV “empire” I plan on rolling out in the next few weeks, but I wanted to start the year off with an idea I’ve been looking at that I think is both very interesting and a place where I would love to swap thoughts with any readers who have some more info on it (feel free to slide on into my DMs or just respond to this post).

The idea is Nam Tai Property (NTP). I’ll note my buddy Clark Street Value mentioned it (briefly) over the weekend (that rascal beat me to it!), but I was already planning to write it up and it’s a situation where more eyeballs can’t hurt!

The idea here is actually really simple: in late November, activists (lead by IsZo capital) finally won a long running battle to take control of NTP’s board. I won’t rehash everything that the old control group (Kaisa) did, but it was not pretty and showed a complete disregard for minority shareholders. IsZo taking control of NTP was a very good thing for shareholders, and IsZo had argued that NTP’s real estate holdings were worth at least $40/share.

IsZo moved quickly on their win, installing Michael Cricenti (an IsZo senior advisor) as board chair and terminating all of the representatives from Kaisa.

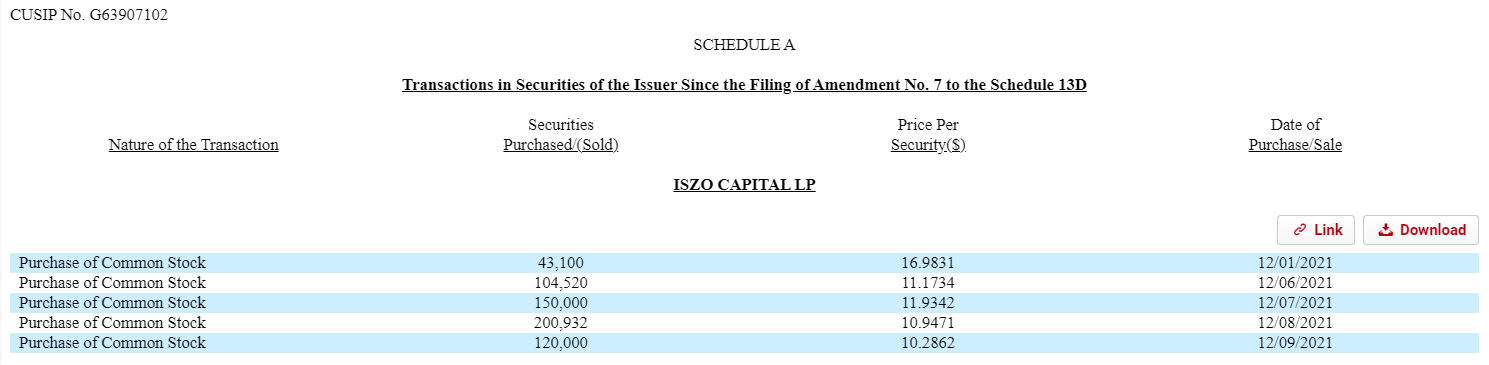

At the same time, Kaisa faced a margin call on their NTP shares. Deutsche Bank foreclosed on Kaisa’s NTP shares on December 3 (according to their 13-D). I’ve got a one year chart of NTP’s price and volume below; see if you notice anything strange starting around December 3.

I think it’s a safe bet the DB has been price indiscriminately dumping the shares they margin called Kaisa on. Given those shares represented >23% of NTP’s shares out and DB just wanted to get made whole on the loan, I’d guess they were pretty insensitive to whatever price they were getting and they’ve been the big driver behind NTP’s fall over the past month.

So I think NTP could be set up as a classic “forced selling situation”; things just got better with a shareholder focused management team finally in control, but the price is getting hammered because you have a price insensitive seller dumping almost a quarter of the company. If that’s right, you’d have to think shares have a little tailwind behind them over the near term as the forced selling alleviates (based on the volume, it looks like DB should have been able to get out by now; I wouldn’t be surprised if that big spike at the end of the year was DB dumping the last of their stake to clean their books for the New Year).

One thing I particularly like about NTP is that IsZo bought a nice chunk of shares in early December in front of the first wave of margin buying. Why does that matter? Well, the buying was early in IsZo’s rule, but it at least suggests they didn’t take over and immediately find that everything in the place had been looted (as sometimes happens in activist situations!). Doesn’t mean there won’t be problems longer term, but it at least suggests some of the worst short term scenarios are reasonably off the table.

NTP is a simple idea: hopefully the forced selling is over and the stock responds well now that it’s done (and maybe with some shareholder friendly representatives on the board / in control now).

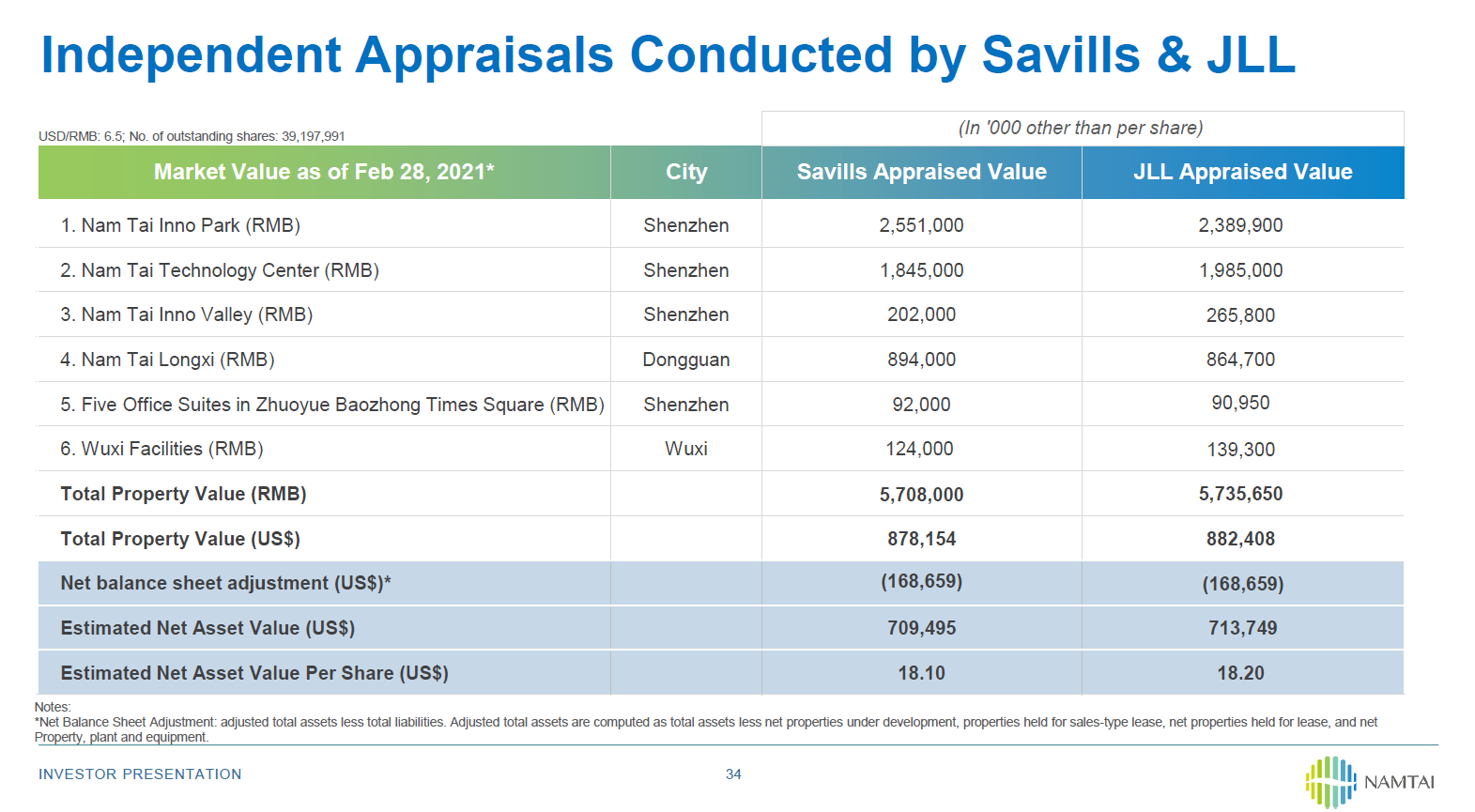

But there are some risks here, and they are big ones. You’ll notice that in this entire write up, I didn’t mention what I think NTP’s value is once. And that’s because NTPs value is pretty much all locked up in Chinese real estate. I have absolutely no experience in Chinese real estate, so I don’t know how to value any of that. NTP’s website has some appraised reports from early in 2021 that painted a NAV picture of >$18/share (see slide below), and you can see IsZo thought the business was worth $40/share in the PR I linked above… but I’m not a Chinese real estate expert. I’m not sure how to back those claims up, and I’m not sure if appraisals from early in 2021 have much weight now there appears to have been a pop in the Chinese real estate bubble.

So there’s obviously mammoth risk here (readers should remember this isn’t financial advice / please do your own work), and I’m necessarily summarizing the story / skipping some key points for the sake of brevity…. but overall the risk / reward here seems pretty favorable.

I’ll disclose I have a small position here…. which is where I would normally end this post. But there is one more thing worth mentioning that I hope some readers can help me with.

One of the most difficult things with NTP is that IsZo was running a lot of their NTP activist stuff through the “fixntp.com” website, which has gone offline / password protected since they took control of the board (see screenshot below). That means a lot of the materials the IsZo used to lay out how they looked at NTP’s value and what their plans for NTP were are not publicly available / hidden now.

So here’s my request: if you have any of the old IsZo / NTP materials (or just anything you think would be helpful with NTP), feel free to slide on into my DMs (or just respond to this post). I’d love to get smarter here!

But deep discount to NAV is ubiquitous in Chinese commercial real estate isn't it? HK2136, HK410, HK207, to name a few.

is DB supposed to update their holding every 1% they sell, as a 13d holder? I am not familiar if there is an exception for them as a bank, or for how they came into possession of the shares, but my understanding is that they have 2 days to amend if they are a 13d. Not sure who else would be selling in volume like this down here though