Quickie idea: $CKH bumpitrage

This post is another in a series I do on an irregular basis. A “quickie” idea is an investment specific idea that I’ve been mulling over and find interesting, but haven’t dove fully into yet. The hope is to provide the jumping off point for a discussion of an idea I find extremely interesting right now, as I suspect the opportunity could be fleeting.

The idea? Buy Seacor (CKH) with an eye towards their current deal needing a bump to go through.

I'm going to keep this simple because time is somewhat a factor here, and the situation is pretty uncovered so this is much more me throwing it into the ether to see if anyone who has done serious work on this can point out flaws.

Some background: Seacor entered a deal to be bought by American Industrial Partners (AIP) for $41.50/share in early December. On its face, there's nothing crazy about the deal. It's probably on the cheaper side, but it's at an alright premium (14% to prior day closing price; 31% to 90-day VWAP). The background of the proxy seems to reveal a reasonable process was run to get there, and there are no enormous conflicts of interest that immediately jump out when reading the proxy.

Still, the valuation and timing of the deal seem cheap. The company is selling themselves for basically book value, and they decided to sell themselves at a pretty inopportune time (2020 wasn't exactly a banner year for dry bulk cargo barge, which makes up the majority of CKH's value). T. Rowe, which owns ~15% of the company, noted this and pushed back on the deal in mid-January. CKH responded to the pushback by (again) saying that they ran a robust prospect and that the company was facing lots of terminal value question marks.

To date, shareholders seem to be agreeing with T. Rowe. As I write this, the stock is trading for ~$42.30, a slight premium to the AIP bid. AIP has been forced to push the tender back three times due to lack of acceptance, The first pushback was January 22 (~28% shares tendered). The second pushback was Feb. 5 (13% of shares tendered). The third and (to date) final pushback was Feb. 16th (9% of shares tendered). This last pushback expires this Friday (Feb. 19).

Alright, that's enough background; you can flip through all of the links and stuff for more.

So why do I think this idea is interesting?

It's pretty clear that the AIP offer is going to fail at this point. Shares are trading at a (slight) premium, and every successive offer has had fewer and fewer shares tendered in to them.

So there are two paths here: first, AIP could bump their bid, or second, AIP could walk and CKH would be left as a standalone company.

Let's start with the first path: AIP bumps their bid. I think this is the most likely path, and it's (obviously) why I'm interested in the stock right now.

What makes me think AIP is so likely to bump their bid?

First (and perhaps most importantly), there's AIP's actions. AIP has extended their bid three times in the past month despite the amount of shares being tendered dropping consistently. I don't think AIP extends the tender this many times in the face of diminishing shares tendered without entertaining a bump. AIP might have extended the tender once if they were right on the border of hitting the acceptance threshold or just hoping that the threat of walking would lure some hold out shareholders to tender at the last second. But they wouldn't do it three times without some type of plan. My guess is AIP keeps extending because they are simultaneously negotiating with T. Rowe for a bid level that T. Rowe would accept while also considering what bump level they would come back to shareholders with if they can't reach an agreement with T. Rowe (i.e. they'd like to announce a bumped deal that T. Rowe has already agreed to accept, but if they can't come to an agreement they'll just take it directly to shareholders and hope enough ex-T. Rowe shareholders accept the deal to push it through).

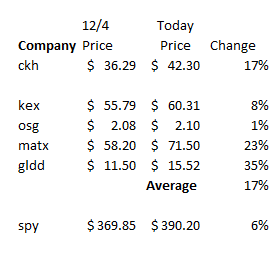

Second, I think there's room for a bump. Markets have gone up a decent bit since early December, and CKH's peers have gone up even more. If you go to p. 35 of CKH's 10-K, they list four peers as well as the S&P 500 to comp their stock performance to. The average peer is up ~17% since CKH got their bid, while the S&P 500 is up ~6%. That peer movement is important for two reasons: it gives AIP a little cover to bump their bid, and it also significantly reduces the downside if the CKH / AIP deal breaks and CKH trades standalone.

Third, while CKH notes that they ran a full process, and there are no obvious signs of related party / corporate governance shenanigans, there are a few things in the proxy that suggest to me CKH was sandbagging a little / there's room for AIP to make a bit of a bump while still allowing themselves to generate a pretty strong return on the deal.

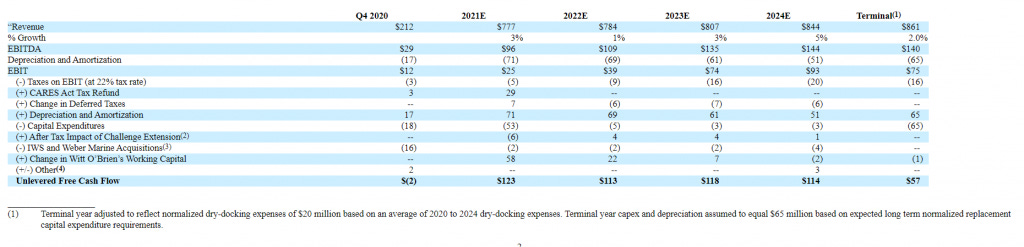

Here are the two main questionable things I see from CKH's proxy. First, check out management's financial projections (screenshotted below). Look at the terminal year capex; CKH is arguing that capex bump is necessary to keep their business running long term.... and they might be right. But I don't think I've ever seen a projection that calls for such a big capex bump in the terminal value. I also think these projections support the view that AIP is buying CKH pretty cheaply; again, the deal is priced at ~$1B. CKH is projecting >$100m in cash flow in each of the next four years, so AIP will be able to take out almost 50% of their purchase price in free cash flow alone over the next four years. Sure, there will be terminal value and capex questions on the back end of that, but getting that much cash flow out that quickly generally results in a pretty solid IRR and can cure a lot of terminal value questions!

The second thing that jumps out at me as questionable is the line below from CKH's background (see p. 16).

On November 19, 2020, the members of the Company Board, other than Mr. C. Fabrikant, held a special meeting, with representatives of Milbank present, to discuss AIP’s bid and the timing and next steps for the Company’s ongoing strategic process. The Company Board had elected to hold a meeting without Mr. C. Fabrikant present in light of the potential continuing role of Mr. C. Fabrikant’s son, Mr. E. Fabrikant, in the Company after the closing of the potential transaction, and the invitation from AIP for members of the management of the Company, including Mr. C. Fabrikant and his son, to potentially roll over their equity in the potential transaction, and any actual or perceived conflict of interest that might arise therefrom.

Later that day, the Company Board held another special meeting, with all directors present, as well as the COO and representatives of Milbank and Foros. The Company Board discussed with its advisors the financial and legal aspects of the proposal received from AIP. Mr. C. Fabrikant stated that he would not be interested in participating in any co-investment or equity rollover. The Company Board scheduled a meeting to be held the next day for further discussions regarding AIP’s proposal.

Later in the evening, the Company Board again held a special meeting with representatives of Milbank without Mr. C. Fabrikant present. Milbank and the directors discussed the independent directors’ responsibilities under applicable law and the Company Board’s process for considering and responding to AIP’s proposal. Despite Mr. C. Fabrikant’s decision not to participate in any co-investment or equity rollover, the independent directors determined to hold additional meetings without Mr. C. Fabrikant present to discuss the potential AIP transaction, and requested that Milbank keep them apprised (including through the Lead Director) regarding the status of discussions regarding the potential AIP transaction. The independent directors also determined that given the supervision exercised by the Company Board over the strategic process and Mr. E. Fabrikant’s knowledge of the Company’s businesses, it would be appropriate for Mr. E. Fabrikant to continue to be involved in the negotiations with AIP regarding a potential transaction notwithstanding his potential continuing role in the Company.

That's pretty weird. AIP basically dangles a carrot to CKH management ("hey, take our deal and roll your equity"). CKH management declines, but the board still decides to exclude the management from the deal process going forward? Note that CKH's CEO will be stepping down if/when this deal goes through, but his son (the current COO) will become CEO once the deal is finished.

Anyway, I can't quite put my finger on it, but something about that management background and succession plan screams "potential for some shenanigans."

Ok, that's the current AIP deal and why I think it's likely to get bumped. But what happens if I'm wrong, the current tender expires Friday, and AIP decides to walk instead of bumping their bid?

Well, then you're stuck with CKH as a standalone business. It's not a business I love: it's a commodity business, and they'll have a lot of management succession issues to deal with. But you're buying it reasonably cheap (at roughly book value), and you've already seen management projections laid out and the company looks cheap on those numbers as well... and I'd guess the business / outlook has only gotten better since those projections were made. So yes, this probably isn't a business I'd want to own for a long time.... but the downside in a deal break looks pretty limited.

Anyway, that's a quick summary / overview of the situation. I think it's attractive, but I've still got lots of work to do in a pretty tight time frame before the tender offer expires Friday.

If you've looked at the company and have thoughts, I'd love to hear them.

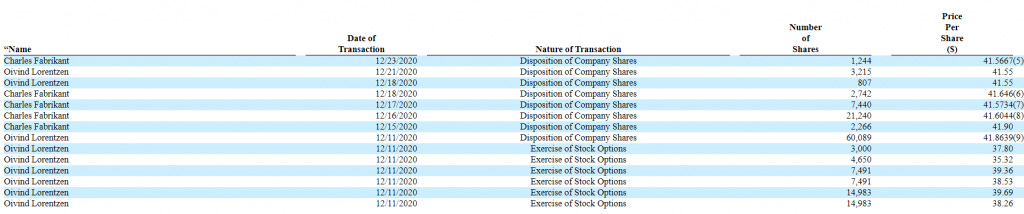

Ps- One last thing while I'm here. This filing shows a decent bit of insider selling after the deal was announced. You could certainly see those sales and combine it with management's decision not to take the equity roll when offered and see a lot of bearishness here. Alternatively, you could see the sales and the CEO's decision to retire and just see a manager who was ready to move on.