Quickie idea: Atlantic Power arb / potential bidding war $AT

This post is another in a series I do on an irregular basis. A “quickie” idea is an investment specific idea that I’ve been mulling over and find interesting, but haven’t dove fully into yet. The hope is to provide the jumping off point for a discussion of an idea I find extremely interesting right now, as I suspect the opportunity could be fleeting.

The idea? Buy Atlantic Power (AT) on a "heads I win a little, tails I win a lot" thesis.

The overall thesis is pretty simple. AT announced a deal to get bought out a $3.03/share on Friday. The deal is expected to close in "the second quarter of 2021"; let's be conservative and say it closes on June 30, 2021 (the exact last day of Q2). Shares are currently trading for ~$2.92, so we're talking a ~3.8% gross spread and a ~8.5% annualized return if you simply buy the shares and the deal closes on current terms. Not bad!

So that's probably your most likely case..... and if that's all that was going on here I wouldn't have written the stock up. But I think there's an argument to be made that AT is getting bought out way too cheaply, and there's a possibility a competing bid emerges or shareholders simply push back hard enough on this bid that I Squared (the buying firm) needs to bump their bid a bit to get the deal done.

The argument for a topping bid is pretty simple: AT owns a bunch of different types of power plants. Power plants are infrastructure type assets, and in a world of zero interest rates infrastructure assets generally command large multiples. AT is.... not getting bought out for a large multiple. Their 2020 guidance calls for $100-115m in cash flow (after taxes and interest expense); at $3/share, AT's market cap is ~$350m, so they're getting bought out for a low single digit equity cash flow multiple.

Now, AT's management would likely counter with two somewhat interconnected points (and indeed, they did on their merger call. I'd encourage you to read that whole transcript):

This bid is a huge premium to our share price, and we've engaged in multiple deal talks over the past few years and this is the best deal / bid we've gotten.

A lot of our earnings come from long lived PPAs (purchase power agreements) that will expire in the next few years; earnings will likely drop significantly as those contracts expire as they were struck when power prices were materially higher. By selling now, we lock in value for our shareholders and shift recontracting risk to someone else.

In fact, management might even say that they hold a lot of stock, and they've been saying for years that they'd be a seller at the right price. See, for example, the quote below (from their 2020 annual meeting)

There's definitely something to those arguments.... I would just counter that there's a price for everything and this isn't it. Consider the quote below from AT's Q4'19 earnings call:

Or consider this quote from their 2020 annual meeting:

Keep those quotes in mind and read this quote from their Q3'20 earnings call:

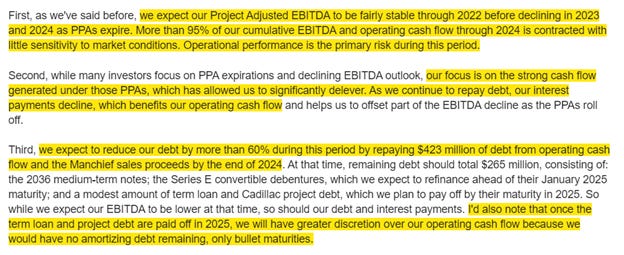

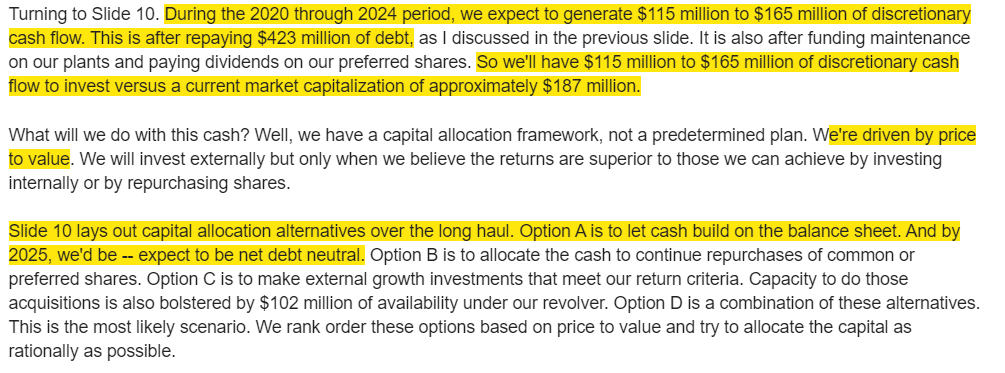

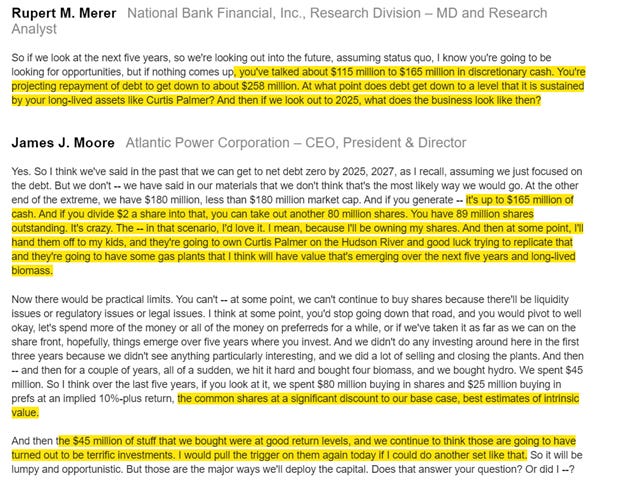

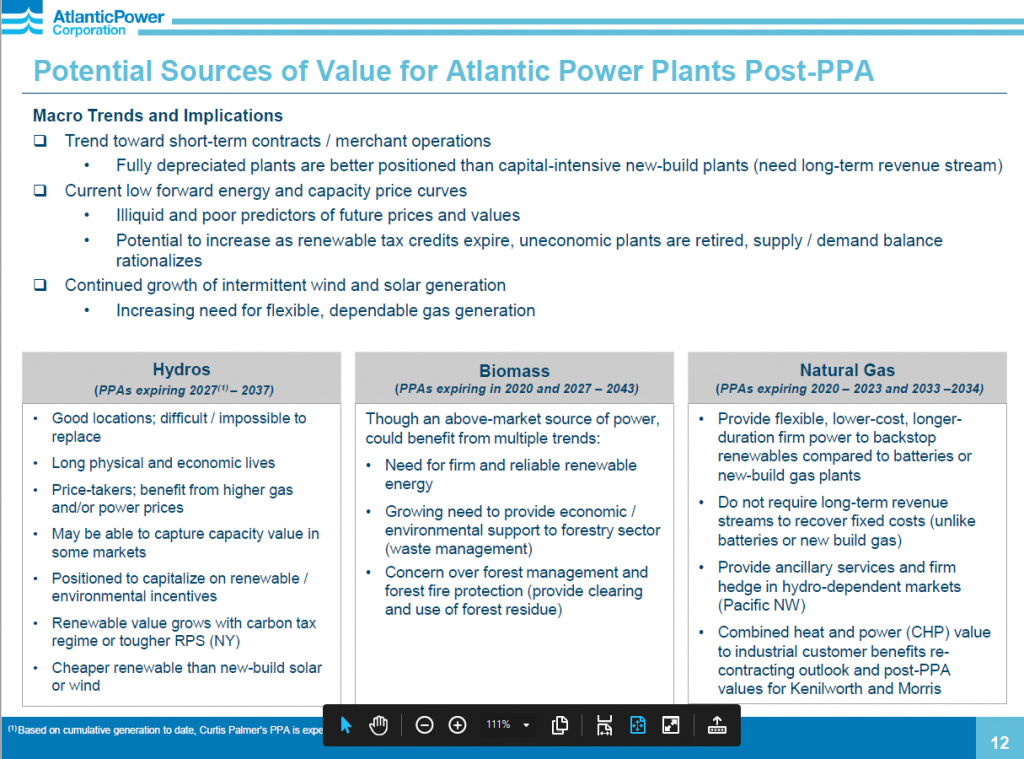

Or take a look at this slide from their annual meeting slide deck. Certainly seems like they think the PPA risk is very, very managable.

To sum up all those quotes, for the past year AT's line has been, "sure, recontracting is a risk, but we're gonna pay off a ton of debt before those contracts expire and it's 'crazy' how cheap we are once you adjust for that. I'm looking forward to buying back all of our shares and handing the remainder to my kids." Now suddenly the line is "recontracting is risky; let's take a bid and run?"

Seems weird.

And while management would say the premium is huge compared to their prior stock price, it's honestly not big in the grand scheme of AT's earnings power. Again, AT is projecting ~$180m in EBITDA and ~$100m in cash flow for 2020; the 50% share price premium the company keeps highlighting equates to ~$120m in market cap, or around one turn of annual equity cash flow. Again, not huge when you look at the overall picture of the company's contracted earnings and ability to go net debt free by 2025.

Why would management suddenly change their tune and sell now? Maybe they got sick of yelling into the void that their shares were undervalued. Maybe they really believe that this offer is fair for shareholders. Either or both are certainly possible.

However, indulge me for a second and let's throw our conspiracy theory hats on. Take a look at the question below from the company's deal Q&A:

That's a very cleverly worded dodge. Is it possible that the management team here has struck a sweetheart deal with I Squared? Sell the company on the cheap, stick around and reload on cheap options once the company is private and more leveraged, and then make a fortune once the recontracting is done and you can sell the company for a big multiple to infrastructure funds willing to pay for certainty of earnings / cash flow?

Seems like that's at least a possibility to me!

There's also another angle here. For the past several years, power prices have been very low, driven in large part by record low commodity prices as well as the rise of solar and wind. Right now, it certainly seems like power prices will continue to spiral lower forever.

History, however, shows us that any commodity tends to swing wildly, and often in direct contradiction to how most people think they'll go (remember peak oil?). AT is extremely levered to power prices; if we got a small bounce back in power prices between now and all of AT's PPAs expiring, the replacement contracts could do a lot better than expected. If that happens, whoever buys AT will make a fortune. In effect, buying AT at a cheap price when they have so much contracted near term cash flow gives the buyer a very, very cheap call option on power prices rising. AT is asking shareholders to give that up for almost nothing.

Just to sum all of this up: however you cut it, AT looks cheap at these levels. I think the buyer is getting a steal, and the call option on power prices makes AT look even cheaper. Given that combo, I think there's a chance we could see a topping bid here.

I think the deal docs support that bid potential. The company's deal Q&A makes clear that they sold on an approach from I Squared (see below), and the deal has a very low break fee in the event of a superior proposal ($12.5m, a near drop in the bucket for almost $1B total deal value!).

In a world of zero interest rates, recent history has suggested that complicated, infrastructure like assets getting sold for low multiples without running a full process tend to get overbids. There's simply too much money out there looking for places to park. In some ways, AT reminds me of previous quickie idea Alaska Communications (ALSK), which had a successful bidding war (though it didn't get as frothy as I anticipated).

AT's probably less likely to get a topping bid than ALSK.... but there's definitely a chance, and even without one the spread is wide enough that the arb alone is attractive.

One last note while I'm here: ~26% of AT's EBITDA comes from hydroelectric. Now, that earnings stream is very dependent on PPAs, and up for a lot of recontracting risk when the PPAs expire. However, hydro tends to be a very in demand asset that can command very high multiples from infrastructure funds; consider, for example, the quote below from BEP's Q3'20 earnings. They're thrilled to have an option to buy hydro assets at 13x annual average 2025-2028 EBITDA!

AT's Hydro assets will earn ~$45m in EBITDA in 2020. If you just slapped a 13x multiple on that, the hydro assets alone would be worth >$700m. The EV of the entire I Squared / EV deal is ~$970m, so if you're just looking at that math you could basically say I Squared is paying of AT's Hydro assets and their near term contracted cash flows and getting everything else for free.

That's obviously too aggressive; AT's hydro assets will face repricing risk in the near future and they're not as good as TransAlta's. But I wanted to highlight it just to show the demand for assets like these and the multiples they can trade at. The current deal doesn't come close to reflecting the optionality of recontracting AT's assets on new, long term deals and selling them for a huge multiple to an infrastructure fund.

PS- there's a reason I mentioned BEP: they're a very likely bidder here. They'd have synergies with AT, and like AT they're a Canadian headquartered company. I took the slide below from BEP's 2020 investor day deck. BEP describes their approach as "deep value," "contrarian", and "complex transactions;" buying AT at a super low multiple due to recontracting risk screams all three of those things. AT would be right in BEP's wheelhouse.

PPS- I started researching AT on the deal announcement and was debating writing it up or not. But then separately my friend Kuppy posted that he was already long the stock and thought it was getting stolen from him, so I figured I'd put some thoughts to paper both because it's an interesting situation and to try to drum up some extra eyeballs on the name / extra support for a push back on the deal.