One simple trick to see if a company is buying back shares during market drawdowns

Markets have been rocky recently. The Russell 2000 (my preferred benchmark) is down ~13% for the year and ~22% from its peak in early November.

Honestly, I’m surprised it’s not worse; outside of anything commodity / energy or maybe consumer staple related, I feel like every company I look at has been cut in half in the past six months.

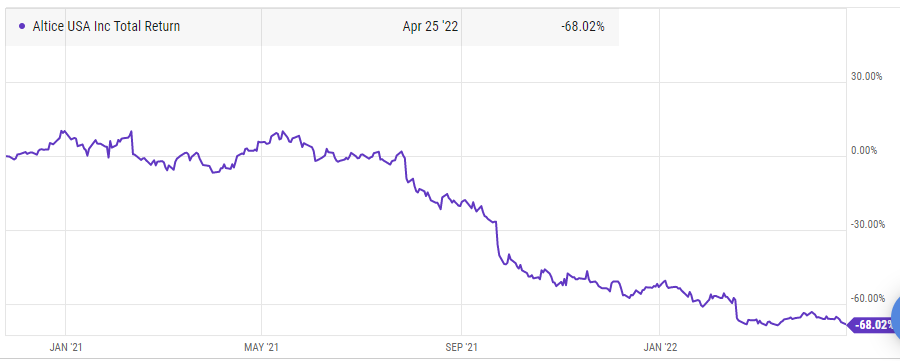

When markets get rocky, it reassures me to know that my portfolio companies are out there buying their shares back at a discount…. but, for domestic companies, it’s extremely difficult to know in real time if your companies are actually buying shares back because there are no filing requirements to alert shareholders if the company is actively repurchasing shares. Too many companies buy back their shares when they are high, and then sit on their hands when the stock gets hit. Altice, where I am a major bagholder, is a classic example: in 2020, they demolished their share count (including a big tender) with the stock trading over $30, and management would constantly brag about how they were taking advantage of a cost of capital arb by taking out cheap debt to buy back shares. Today, the stock is barely above $10, and ATUS has stopped buybacks to delever and reinvest in the business.

So, in general, the best investors can do for figuring out a company’s share repurchase during major drawdowns is look at management’s history with buybacks and hope that the pattern continues (note: that’s only for U.S. stocks; some international markets require the companies to file every day they buyback shares, which I kind of like but can see some drawbacks to as well).

But there is one trick to figuring out share repurchases in real time. I thought it was pretty obvious, but I’m frequently surprised to talk to investors who don’t know about “the trick”, so I figured I’d get it out in the open.

The trick? Read the financial reports carefully!

Ok, that’s lame. But it’s true. There are two versions to this trick that come from reading the financial reports: I call them the 10-K / 10-q version, and the proxy version.

Let me start with the 10-K / 10-Q version. The trick here is that companies will often disclose the most recent, up to date share count at the start of the proxy. Compare that to the balance sheet number, and you can sometimes catch a big share buyback.

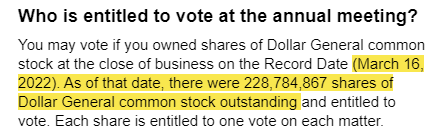

An example might show this best. Consider Dollar General (DG). Their balance sheet discloses ~230m shares out at the end of the (fiscal) year.

But if you zoom to the front of the 10-K, they disclose they have ~228.9m shares outstanding as of March 11, 2022.

We know that the company cut their shares outstand by >1m from the balance sheet date (January 28, 2022) until March 11. How did they do that? Share buybacks!

So that’s the beginner version of this trick. But there is a more advanced version: proxy statements disclose how many shares there are as of the record date for the proxy going out. By comparing that to the last share count, you can find out how many shares have been bought in the mean time.

An example might show this best. Sticking with DG, their proxy discloses 228.8m shares outstanding as of the record date (March 16). So we know DG bought back ~100k shares between March 11 and March 16.

Maybe you’re thinking “so what; those are pretty small changes!” And, in DG’s case, you’re right! But I find the process useful for two reasons:

It gives confirmation that the company is still buying back shares.

Sometimes, you’ll catch a company with an unreal share buyback in between the dates, and the market might be asleep at the wheel.

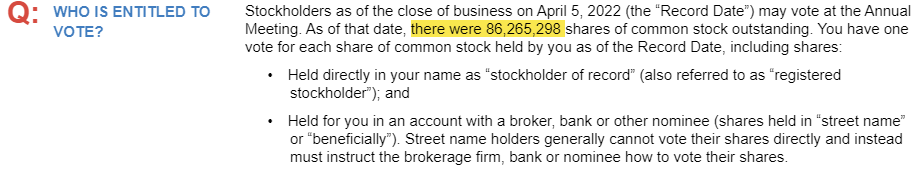

An example might drive home point #2. Consider ASO. At the 10-k date of March 22, they had 87.1m shares out.

When their proxy went out, they disclosed that as of the record date (April 5), they had 86.3m shares out.

That means that in the two weeks from March 22 to April 5, ASO bought back ~880k shares, or just over 1% of the company.

That’s an aggressive pace; annualized, it’d put them on track to buy back over 25% of the company!

Will ASO keep to that pace? As a shareholder, I sure hope so! While I doubt they’ll be that aggressive (though, again, I hope so as a shareholder), that they’ve been so aggressive in the two weeks between the K and proxy suggests to me that they see clear value in their business and gives me a little extra confidence that the business isn’t falling off the cliff (despite what the stock market price is implying!).

What makes the ASO signal even more interesting is that they are not the only people in the sporting goods world pursuing an aggressive buyback. HIBB’s 10-K reveals that they had 13.14m shares out at March 22:

By the record date on April 7, they were down to 12.97m shares out.

So, just like ASO, HIBB retired >1% of shares out in ~2 weeks between the 10-K in the proxy. That means we’ve got two players in the industry who are buying back their stocks at frantic paces. I’ve been saying for a while that retail stocks in general and sporting goods stocks in particular are undervalued; maybe the market’s right and I’m wrong, but it certainly appears that the management teams agree with me! I suspect these repurchases will create a lot of value in the long term, but we’ll see!

Is this “intra-quarter buyback check” the most powerful signal in the world? Of course not! You need to do your own work and make sure you’re not getting ATUS’d, it’s obviously not perfect (option dilution and the like can mask buybacks to some extent), and it’s not always relevant (plenty of companies don’t buy back shares, or buy them back at such an insignificant rate that this signal isn’t going to move the needle). But it’s a signal that’s very much worth checking; I’ve stumbled a few times on situations where using this trick revealed a company had cut their share count by a huge amount (>10%) in between filings and the market was completely asleep at the wheel. Sometimes a stock can be undervalued because the market is worried management won’t buyback shares and will waste all the cash on awful acquisitions; when that happens and you notice a big stock buyback has started through this trick, it can result in really powerful returns when the market catches on. And, even without set upt, continued share repurchases at a decent pace between filings can certainly lend incremental confidence in a position / that the business isn’t falling off a cliff.

I hope you find this trick useful (and, if you find any companies that have gotten crazy with demolishing shares between filings; I hope you’ll be kind enough to slide into my DMs and share them with me so I can add them to my research list!).

I wonder if it makes sense to write a script to scrape the information and detect large buy backs automatically for every ticker.

Tianwei, is it possible to scrape the "quarterly earnings conference call" transcripts?

This could be another good source for what you're trying to do.

If feasible, what source do you get all/most CC written transcripts from?