Corporate dark arts: five big bets $SNDA $CCOI $KVYO $PYPL $CERT

Corporate dark arts, part 10

Today’s post is the tenth post in my “corporate dark arts” series1, and I wanted to hit five of the higher torque situations I’m aware of. They include:

SNDA has something for everyone

CCOI: insane or insanely bullish? (disclosure: long a tracking position)

Everyone at KVYO is betting SaaSpocalypse fears are overblown (disclosure: long a tracking position)

PYPL’s second time is a lot more stock focused….

CERT’s new CEO is down but not out (yet)

Let’s dive in:

SNDA has something for everyone

Pound for pound, Sonida Living (SNDA) is probably the stock I get the most inbounds on. I’d say there are three reasons for the inbounds.

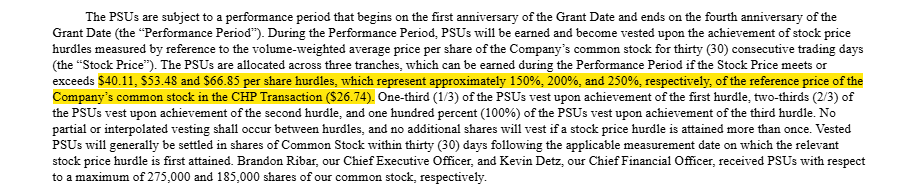

The first and simplest reason is that SNDA has a very obvious “dark arts” angle: they granted their C-Suite PSUs with pretty aggressive hurdles towards the end of February:

Those grants on their own are interesting, but combine them with SNDA’s controlling shareholder (Conversant) investing ~$100m into the equity on the deal closing2…

And insiders are clearly very aligned and very bullish on the equity here…. which blends nicely into the second point: that big insider equity financing and the PSU grants were done in conjunction with SNDA’s merger with CNL Healthcare (they call it CHP), an externally managed nontraded REIT. SNDA is projecting significant synergies from the merger, and I know a lot of people think the synergies are probably understated (nontraded externally managed REITs are notorious for being run for their managers; it would surprise no one if a good operator got inside one and found lots of different cost or revenue levers that could easily be pulled). So the second bull case is not just that insiders are bullish on SNDA; it’s that the CHP merger is going to be a homerun and blow away initial synergy / accretion projections.

Bull point three would build off of point two. A lot of investors are very bullish senior housing on a “capital cycle” story of “we got overbuilt, haven’t built in years, and the 80+ population is exploding”….

And between the insider alignment and the clear vision they’ve laid out for growth and compounding per share value, SNDA seems like a natural place to make an “outsiders” type long term bet.

SNDA is not, of course, alone in making bullish dark arts grants. In fact, I know it’s surprising to say given SNDA’s controlling shareholder bought ~$100m of stock alongside the merger, but I’d argue that SNDA’s “greed signal” is downright mild compared to the wild torque on some of the other grants out there. Which brings us naturally to our next set up:

Keep reading with a 7-day free trial

Subscribe to Yet Another Value Blog to keep reading this post and get 7 days of free access to the full post archives.