Busted deSPACs: when do the activists arrive? $XL

I wanted to take a break from my cable deep dive series (here’s part 1, part 2, and part 3) to return to an old favorite stomping ground: SPACs.

Long time readers will know I’m endlessly intrigued by SPACs and have written them up extensively (some readers might say I’ve written them up too extensively). I don’t want to dive into all of the nuisances of the SPAC market here (though I may have a podcast coming up on the topic in the near future); instead, I wanted to ask a simple question: when are the activists going to step into some of these deSPACs?

Activism could come in a variety of forms depending on the SPAC. Some SPACs are “babies thrown out with the bath water”; good companies that went public through a deSPAC and are now seeing their share prices murdered as no one wants to touch a company that came public through SPACs in the past year. Those seem ripe for the traditional activist playbook (push the company to return capital to shareholders / buy back undervalued stock).

But perhaps more interesting is the wave of deSPACs that have businesses that could be generously described as science projects. If they deSPAC’d at the right time, their share prices often went parabolic. That gave them the opportunity to have limited redemptions when they completed their deal, raise lots of money in a PIPE, and maybe even redeem their warrants to get even more cash on their balance sheet. Those companies are now often trading at or below cash value; I wonder how long it takes for an activist to step in and say “hey, let’s cut off the cash burn, sell whatever IP or operations we have, and return the rest of the cash to shareholders.”

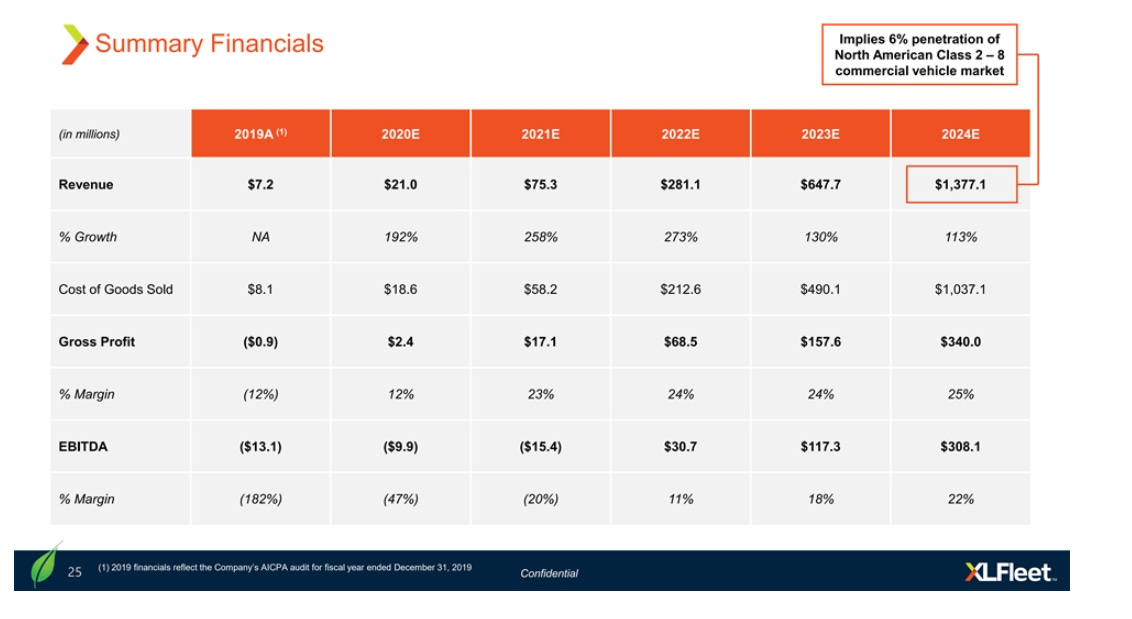

A good example of this opportunity would be XL Fleet (XL; I’ll disclose I have a tiny tracking position just because I’ll buy a tracking position in almost anything trading below net cash). XL is “a leader in vehicle electrification solutions for commercial and municipal fleets”. They announced their deSPAC in September 2020, and boy was it a buzzy one. On top of $232m in cash in trust from the SPAC, they had $150m in PIPE money. The founder went on CNBC to pitch the deal after the announcement, and the stock went parabolic as investors dreamed of a multi-year growth story. Those dreams were in large part supported by the company’s outlook, which projected revenues to grow from basically nothing in 2019 to $280m in 2022 (when they’d hit EBITDA profitability) and almost $1.4B by 2024 (when they’d spit off >$300m in EBITDA).

Again, investors loved the story. Shares instantly traded at a premium to trust, and they peaked at ~$30/share in late 2020 / early 2021 as XL completed their SPAC merger and growth stocks went parabolic. At that price, XL’s market cap was well over $2B.

XL used the strong stock price to redeem their warrants in January 2021, which generated ~$86m in proceeds, and to make a small acquisition of a profitable business at ~1x revenue.

That was really the peak for XL. Since then, the stock has fallen off a cliff. As I write this post, it trades for ~$2/share. Their initial deal projections called for ~$75m in revenue in 2021 and $15m in EBITDA losses; they’re going to miss both those projections just slightly (insert sarcasm emoji of your choice here). Through Q3’21 (they haven’t reported full year results yet), revenue was just $7.6m (down from $9.5m through Q3’20) and EBITDA burn was $35m. XL replaced their CEO in November, and the stock has cratered to ~$2/share.

Normally, I’d chalk this up as yet another broken SPAC. But remember that the company used their share price euphoria to raise a bunch of cash and redeem their warrants; check out XL’s balance sheet (here’s their Q3’21 10-Q). The company has ~$367m in cash and just $40m in total liabilities. That’s ~$327m in net cash less all liabilities; with ~140m shares outstanding (and basically no options in the money), the company has net cash per share of ~$2.33/share versus a current share price of ~$2/share (the company also has ~$20m in inventory and A/R I’ve ignored for this, as well as a few million in other long term assets).

This is a business that has absolutely no reason to be public at this stage. The capital markets are saying it’s worth less than it’s cash value. They’re burning ~$10m/quarter in cash, and most of that appears to be related to legal and accounting costs from being public (per their 10-q, “Selling, general, and administrative expenses increased by $7.4 million, or 140.2%, to $12.7 million in the three months ended September 30, 2021 from $5.3 million for the three months ended September 30, 2020. The increase consisted principally of an increase in legal, accounting and other professional fees incurred in connection with meeting SEC and other financial reporting responsibilities in the amount of $0.5 million, and an increase in headcount of about 46 employees attributable to the responsibilities of becoming a public company and to build out our human resource infrastructure in the amount of $3.6 million.”). It seems like the potential activist playbook here is clear: force the company to immediately stop the cash burn. Sell the assets and relationships to the highest bidders, and then liquidate the company.

Now, liquidations and proxy battles have costs (particularly if the company tries to fight you), and XL is currently burning money. So I think a reasonable push back would be “by the time the activist wins, cash is going to be below the current stock price.” I hear that, but I’d have two slight push backs to that push back.

I only gave value to XL’s cash above. On top of the receivables and inventory, XL does have relationships with lots of big companies (look at all the logos from their going public deck). I’m guessing there’s some value in their IP, relationships, etc. that you’d realize in the liquidation. Heck, they paid $16m (~1x revenue) for a company last summer that they said was already profitable; there has to be some value there, right?

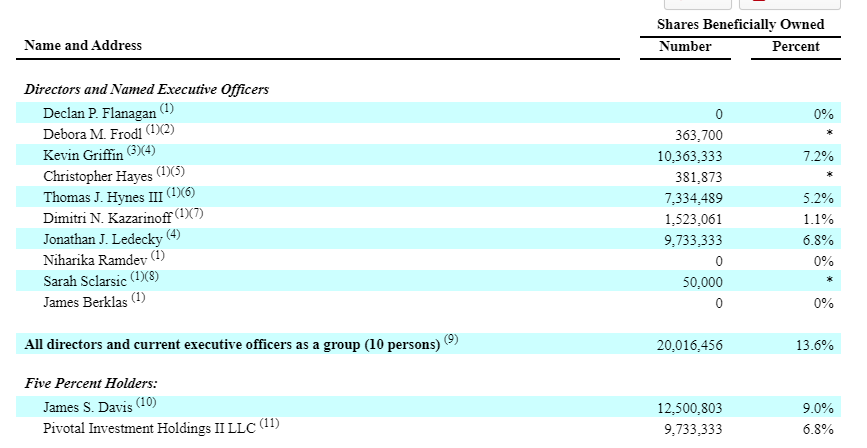

XL’s board has reasonable insider ownership and there are several financial people on the board (mainly from the SPAC sponsor). They have to know this is a lost cause as a public company at this point; maybe they’d support an activist that let them salvage a portion of their investment before they burn it all to zero on public company costs (note: the share counts include sponsor warrants that are hopelessly out of the money, so insider ownership isn’t quite this good….. but the Pivotal shares are founder’s shares with a pretty low cost basis, so maybe they’d be happy to just liquidate, take a profit, and move on). (table below from the 2021 proxy; I haven’t seen any insider selling buying or selling form 4s since but I could be off)

Anyway, you and I could quibble with lots of different parts of XL and the potential liquidation value, but I don’t want to miss the forest for the trees here. I chose XL because a reader pointed them out to me and they’re a perfect example of a type of company I’m looking for: deSPACs that have seen their shares hammered but took advantage of the hot market last year to raise a ton of cash and, because of that, have incredible balance sheets and are often trading for low multiples or even below liquidation value.

If you’ve got any favorites I should be looking at, I’d love to hear them (or, if you want to buy up a bunch of XL and push for rationalizing the cost structure and returning cash to shareholders, I’d be broadly supportive!).

I've been doing work in this area for a few weeks...will be sharing some detailed thoughts shortly :)

I've seen a few of these deSPACs. I guess the challenge is - where's the upside? Net cash of $2.33 versus share price of $2.0. You can make 15% on a gross basis, but you have to deal with the interim cash burn and any costs associated with the liquidation. They are burning roughly $0.30 per 12 month period, so the upside goes away pretty quickly. Feels like you need a much bigger discount.