Black box risk and $GECC

In general, markets have been pretty ebullient recently…. but if you talk to anyone who is running long / short, they’re probably tearing their hair out.

Why?

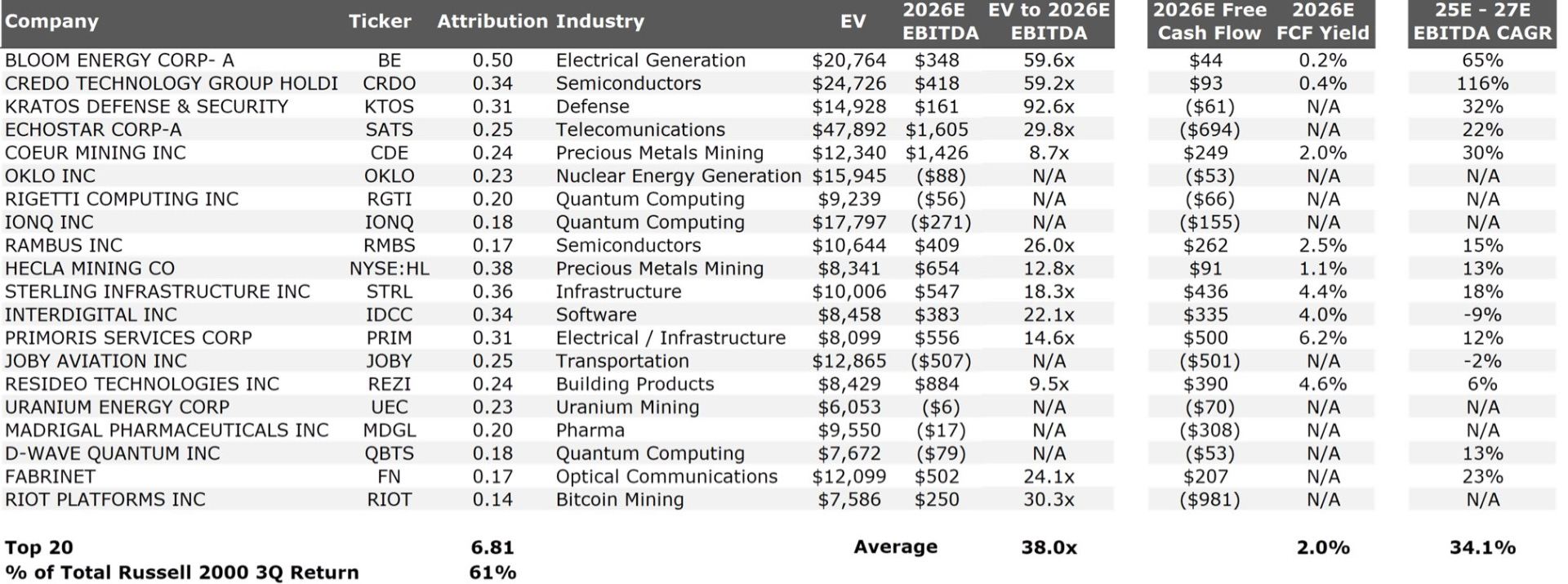

Well, while markets have been ripping, the rip has generally been lead by “low quality” stocks (as well as anything that touches AI, though “low quality” and “touches AI” can often go hand in hand). I thought the chart below was kind of interesting; it shows 20 stocks drove 61% of the Russell 2000 returns! I’ll refrain from commenting on any specific stock in the grouping, but at a high level I’d note that most of these have been on the radar of one activist shorts seller or another at some point, and that even ignoring the higher level short thesis many of these are names trading at nose bleed valuations with questionable business models. Again, I’m painting with a very broad brush here, and there are one or three gems in here, but high level I think I’m being directionally accurate with that categorization and I wouldn’t be surprised if this basic drastically underperformed on a longer time horizon.

But even in a rip roaring bull market (and, if we’re not already there, we’re definitely close), there are pockets of dislocation. And one tiny corner of the market is currently seeing a whole lot of dislocation: BDCs.

Most of the issues can be traced back to the bankruptcy of First Brands. Multiple BDCs had exposure to First Brands (as did some banks); at the center of the storm is Great Elm Capital Corp (GECC), which is taking a ~$16.5m write down (~10% of its NAV) on its loans. That write off has set of a bit of a…. well, panic is too strong a word, but strong worries as investors fret about both exposure to First Brands and what else lies in the BDCs loan books.

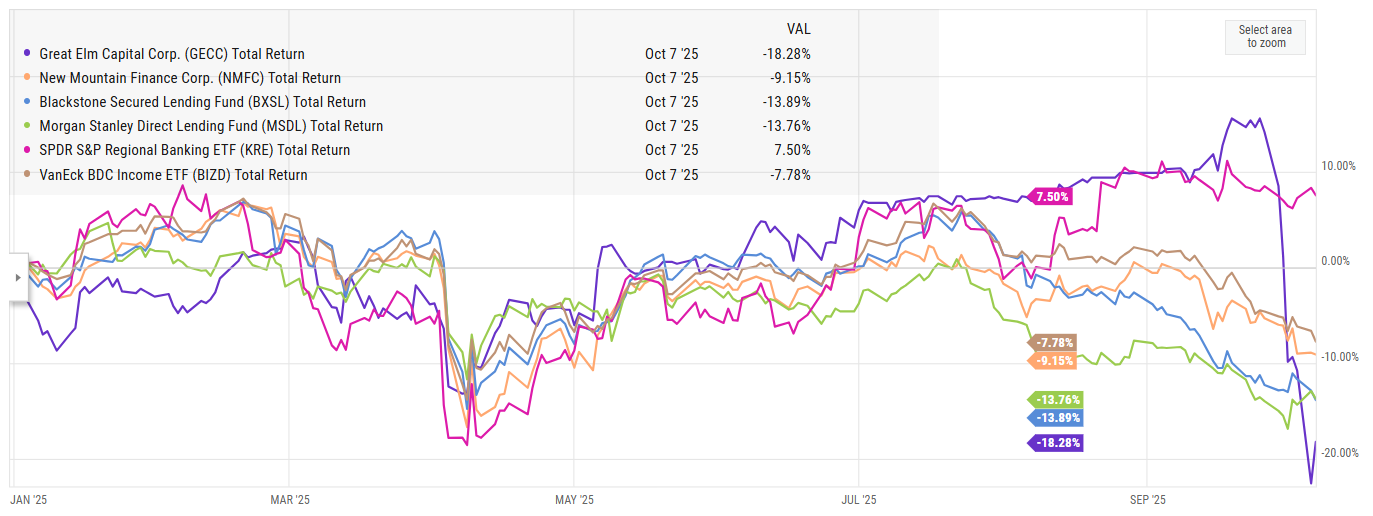

There’s generally opportunity in panics. GECC’s stock was trading for >$11/share before the First Brands situation came up. They’ve already quantified their hit to NAV from first brands (~$1.20/share). As I write this, the stock is trading <$8/share, so the stock has lost ~3x the value of the First Brands write off. That’s the price of any financial losing the trust of the market; if the market worries about where your book is priced, it’s going to take a conservative view instantly and wait for you to proof them wrong.

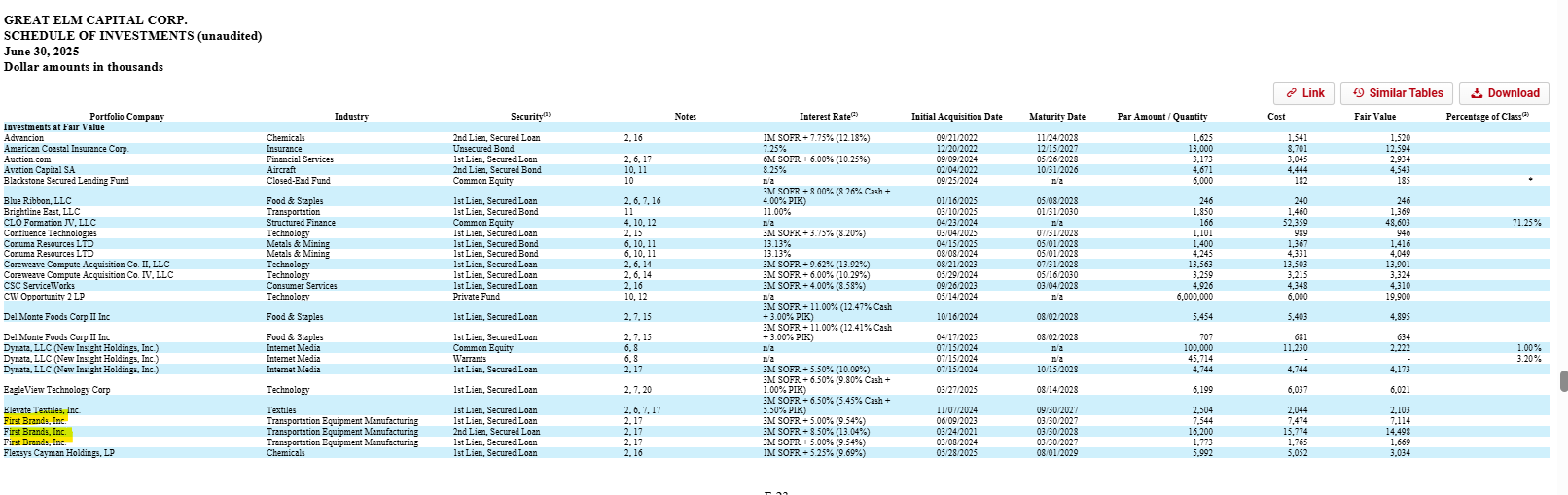

Stepping back, there’s a reason I wanted to talk about GECC. A lot of investors won’t invest in financials because their books are too much of a “black box.” Consider a bank: banks employ substantial leverage to make loans. All it takes is one or two large loans to go bad, or the bank to be two aggressive in one or two assumptions, and the bank can instantly see most of its equity dwindle. BDCs actually solve a lot of those issues; their 10-Q publishes details on every investment they have made, so any investor can go crazy performing any amounts of due diligence they want on their holdings. For example, here’s a screenshot from GECC’s 10-Q; you can see they clearly disclose the loans (and marks on the loans!) to First Brands.

Investor often suspect BDCs are mismarking their books in order to look better (i.e. the BDCs will try to hold loans at par until they’re basically forced to right them off because the company is bankrupt and liquidating at way below par!), and as someone who has dabbled in BDCs previously I’ve definitely seen some wild marks.

But what I find so interesting about GECC is it shows that the insiders often genuinely believe their own marks, and that their portfolios can be just as much a black box to them as they are to us outsiders.

Why do I say that?

GECC raised $15m of equity in late August. They raised that equity from “an affiliate of Booker Smith, a newly appointed director of Great Elm Group, Inc., with extensive experience in corporate credit and real estate investing.” This was a big raise for GECC; $15m bought Booker ~10% of the company at a price of $11.65/share. There were also several other directors who bought small amounts of stock on the open market around $11/share over the summer.

Obviously the First Brands situation has a whiff of… “irregularity” to it, so it’s somewhat unique. But there’s always the temptation when a BDC takes a big write off to say “o, they knew that was a bad loan and they were just waiting till the last second to rip the band aid off and tell shareholders.” And the actions of GECC prove that’s not always the case; GECC insiders clearly believed in the value of the asset here or else they wouldn’t have been pumping so much money into the company!

There is one other interesting angle to GECC. Their FAQ notes they sold ~half of their first lien loan during Q3 for 97.9% of face, a bit above where they had been valuing it at the end of Q2 (by the way; how would you like to be the firm that bought the First Brands loan at basically face value from GECC right now? Woof!):

Again, I just find that fascinating. NAV at the end of Q2 was $12.10/share. If you had told me that the company was selling loans at above their marks intra-quarter (as they did with the First Brand loan) and that a newly appointed director had bought 10% of the stock in a private deal at a discount to NAV, I probably would have been pretty frustrated by the dilution at a mark that was so clearly under fair value as an existing shareholder. Benefit of hindsight, that capital raise might save shareholders!

Anyway, I have no firm takeaways here…. but a few years ago I got really interested in the banks on the heels of the SIVB collapse, and one of my big worries was always the black box risk of the banks. The First Brands blow up reminded me of that black box risk, and combining that issue with the insider buying and everything made for just a fascinating situation that I kept thinking about. I just thought the whole set up was interesting, and given I kept thinking about it I figured I’d put some thoughts to paper. Of course, I’m willing to admit I’m far from an expert in the space / these loans, so if you see any angles I’m missing my comments are always open!

So what if these guys were buying their stock in August. Dick Fuld bought LEH shares too.

Look at how clueless all these guys are. Jefferies with $715M exposure?

The reason this trades at a steeper discount is because the market is now suspicious of all this private credit b.s. all these guys have been selling and putting on their own books

Andrew, I love reading your articles. I like your style and how you think through your ideas as part of your narration. I will say that you have four or five typos in this article that become a bit of a distraction when it’s more than here or there. If you’re using a voice to text or something, you should QC this particular app you’re using and decide if it’s worth it. Keep up the great work otherwise!

Brent