A cyclical boom is eating the whole index: memory, semis, and the active manager's nightmare

Markets are cyclical; there's nothing new about that. There's always some corner of the market riding a bull wave or a strong pricing environment. There was peak oil in ~2006, or the commodity bull market in ~2022 after Russia invaded Ukraine. There was a wild memory cycle in ~2012 when one of the memory plants got flooded, and there have been too many crypto booms and busts to count over the past ten years.

For anyone who benchmarks to an index, I'm not sure we've ever seen anything quite like the current memory / semi cycle: a single cyclical boom that is big enough to move the whole market by itself.

In the short term, the supply of memory and semiconductors are somewhat fixed; it doesn’t really matter how strong the demand is, it takes years to build up new plants to make more of these. The AI boom has driven seemingly unlimited demand for memory and semiconductors. Combine skyrocketing demand with no immediate supply response, and memory and semiconductor prices are soaring… and taking their underlying stocks with them.

Nothing in that sentence is new when it comes to cyclical booms/busts. Most big commodity industries have relatively fixed supply in the short term, and they all run through booms and busts….. but the AI boom is somewhat unique in its structure. Consider a few factors:

Scale of demand increase: most commodities tend to have pretty stable demand because they’re reasonably mature industries. A really strong economy is going to send the demand for energy up by a few percent at most. The auto cycle tends to swing on 5-10% moves in annualized new car sales. In contrast, memory demand has gone up by ~400% inside of a year or two.

Lack of supply response: Send prices up enough, and you’ll find some form of switching. When oil spikes, governments will release their strategic reserves to smooth out prices. If nat gas spikes, you’ll see switching from nat gas to coal. And it only takes a few weeks to bring on some marginal supply of nat gas / oil…. but there’s no strategic memory reserve to release from, and there’s really no alternative to memory a la nat gas / coal.

Lack of demand destruction: When oil prices double, people respond on the margin with less oil consumption. Flights get cancelled, road trips get shortened, etc. When electricity prices go up, you’ll see factories ration production. But the AI boom has shown no sign of abating, and the only demand destruction we’ve seen has come from the AI labs throttling their users to meet booming demand.

So those factors make this cycle even hotter / faster than a normal commodity cycle. Consider this: Micron did ~$1b in free cash flow in FY25 and was trading for just over $100B EV. Today, Micron is forecasted to do $100B in free cash flow in 2027. That’s right: Micron’s free cash flow is up almost 100x in ~2 years, and they’ll print almost their entire EV heading into the cycle. Again, we’ve seen cyclical booms before, but the scale and speed of this one is mind blowing!

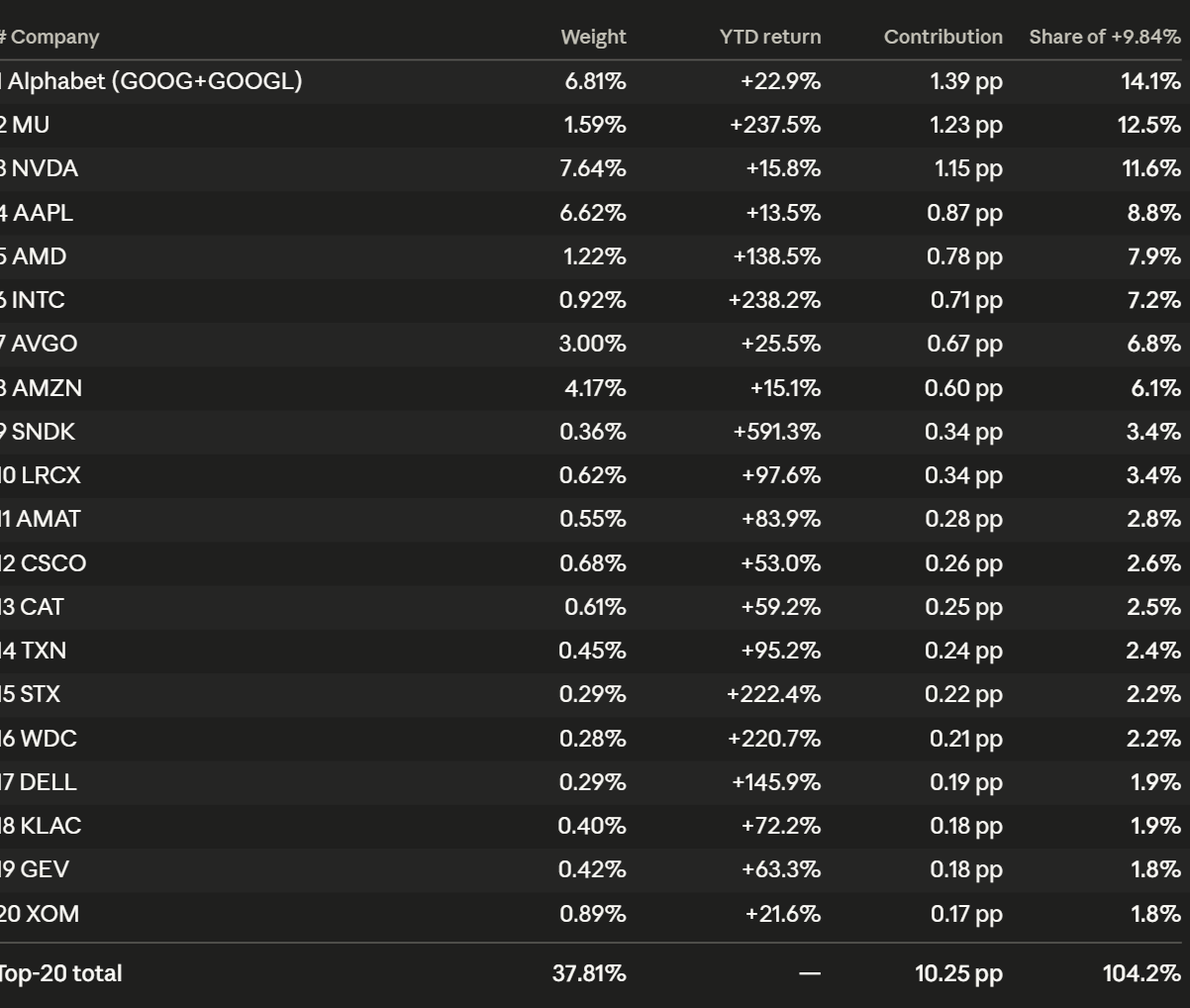

Perhaps my memory (pun intended) is lacking, but I’m not sure we’ve ever seen a cyclical upswing like this drive an entire market before. As I write this, the S&P 500 is up ~10% YTD. Basically half of that return is coming from just four stocks: Google (~7% of the index, up 25% YTD), NVDA (~7.6% of the index, up 16% YTD), Micron (~1.6% weighting, up ~250% YTD), and AMD (~1.2% of the index; up 140% YTD).

If you broaden it out a little bit to include just AAPL, INTC, AVGO, and AMZN, 8 stocks have driven 75% of the S&P’s YTD return.

And the top 20 contributors to the S&P have generated more than all of the index’s returns YTD:

Those are large companies making massive moves! Again, it’s nothing crazy to see companies generating massive returns during a cyclical bull. What is crazy is to see it happen to companies this large and have them single handedly drive an index.

Now consider what those massive, concentrated moves mean for an active investor benchmarked to the index: if you were underweight a single one of those stocks, you’re trailing the index by a mile. If you were underweight a handful of them and long a single SaaS stock (shudders), you’re currently writing your first draft of your H1 letter explaining to your LPs why you’re trailing the index by 1500 bps.

I was in grammar school during the dotcom bubble, so I can’t claim to have personally known what it was like investing then. But you’ll read about value investors then tearing their hair out as dotcom stocks doubled seemingly every week with no fundamental value while their value stocks languished.

The current market is nowhere close to that bad. The AI beneficiaries are minting money while they’re riding the current wave. Again, Micron might do $100B in free cash flow in fiscal 2027; that’s roughly what its EV was in mid-2025!!!!

But a lot of value stocks are languishing. And while AI bulls would tell you that cycles are over, I’m somewhat skeptical that this time is different when it comes to the boom/bust nature of semis or memory. These companies are simply printing too much money for there not to be a supply response, and history suggests that a super cycle this profitable will eventually be met with a supply overbuild for the ages.

If and when that happens, it’ll be interesting to see what happens to the indices!

PS- there’s a wave of big IPOs coming (SpaceX, Anthropic, etc). These are some of the biggest companies the markets have ever seen, and they’ll almost certainly quickly get added to the indices. While they will carry a lot of AI related “factor beta”, I would guess they’ll also be less cyclical than something like Micron or AMD. So, humorously, you could live in a world where MU and AMD drive the indices up, then see their weights diluted when a new wave of mega IPOs get added to the indices, and then don’t have anywhere close to as big of an impact if their stocks go down as the cycle ends. Being an active manager is hard!

The filing language has not caught up to the cycle yet. Micron's most recent 10-Q (accession 0000723125-26-000006, filed March 19 2026 for the quarter ended Feb 26 2026) still carries Item 1A risk-factor language about oversupply, falling average selling prices, and inability to reduce per-bit costs as fast as price declines. That is the same boilerplate they have run in 10-Qs going back through 2009. The fiscal Q4 10-K filed in October will be the interesting diff: if the supply-overbuild language stays verbatim while FCF is up roughly 100x, the legal team is writing a different filing than the CFO is guiding. If it gets watered down, that is the company telling you which way they think the cycle is breaking.

Today’s blog: water is wet.