Some things and ideas: July 2018

Some things and ideas: July 2018

Some random thoughts on articles that caught my attention in the last month. Note that I try to write notes on articles immediately after reading them, so there can be a little overlap in themes if an article grabs my attention early in the month and is similar to an article that I like later in the month.

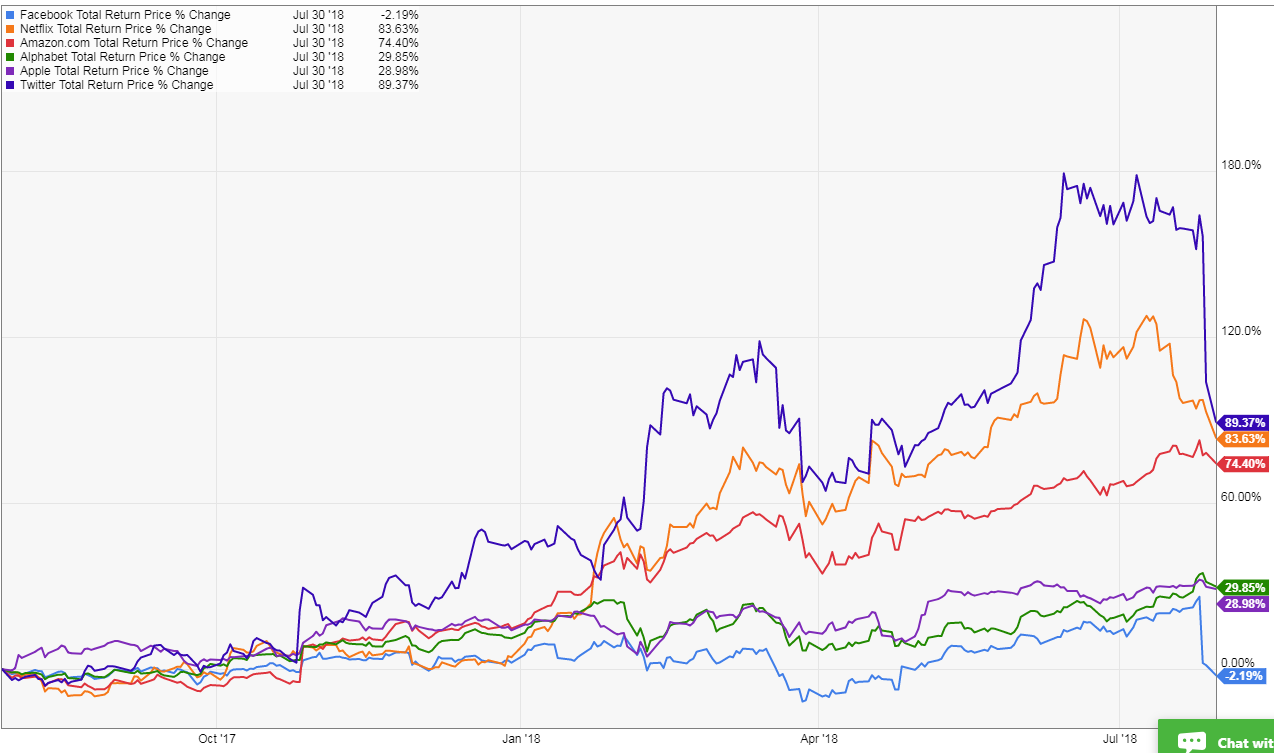

Tech stocks, particularly the FANG and FANG related stocks, have been weak since facebook’s earnings last week, and the fast money / CNBC type crowd is freaking out.

I’m a “no-FANGer” (I don't own any of them), so I don’t have a huge opinion on the stocks, but I do think the narrative override caused by short term stock performance is interesting. These stocks have been massive, screaming homeruns for the past year, even after the small recent drop. An interesting thought experiment: if we lived in a world where all of these stocks ended up with the stock prices they currently have, but just rose a bit less slowly over the past year so that they didn’t have the massive drop over the past few days to get them to today’s prices, would we be seeing the “death of tech” headlines we’re currently seeing? Or would we still be reading the “tech is taking over the world” stories? I would bet the later.

Family Activism

Joseph Hughes owns 42% of TSRI. He was the CEO from 1969 until July 2017. He’s in his mid-80s, and now that he’s retired he’s been disappointed by the company’s results and wants liquidity for his stake. Given the size of his holdings, he’s asking the company to put itself for sale. All of this is pretty normal…. Except for the fact the current CEO is Joseph’s 56 year old son who has worked for the company since at least 1991. Also humorous: James Hughes wrote the “please sell the company letter”. I’m guessing James is Joseph’s son, so he was going activist on his brother. Talk about an awkward thanksgiving!

That got me thinking about other examples of family activism. Modest Proposal gave a very funny example of the Chairman of 99 cents making an unexpected bid for the company that shocked the CEO / his son in law. A few years ago I remember Mark Birner going activist on his brother at Birner Dental (BDMS). That story is actually still playing out- Frederic was just ousted as chairman, and if I’m doing my math right every share that was not owned by a Frederic or one other board member was voted against him, which is worthy of an award. Honestly, the more I look at the vote results the more impressed I am by how poor a showing this was- Frederic was “unanimously” recommended by the board, but despite that recommendation ~400k of the ~1m shares owned by the board had to be voted against Frederic for him to receive as few votes as he did (in addition to every vote from an outside shareholder going against him). Truly incredible stuff.

Amazingly, there’s another example of family activism going on in the market right now! On Friday, LGL Group published a press release announcing they were evaluating a non-binding acquisition proposal. The release included a quote from LGL’s non-executive chairman, Marc Gabelli, announcing that the company continued to work to find value creation opportunities. The company’s largest shareholder responded that the transaction made “no economic sense” as described. The largest shareholder? Marc’s father, Mario Gabelli.

Semi-related: this filing has to have the best activism / word ratio in history (I posted this last month but I kind of buried it so I wanted to make sure everyone saw it).

Speaking of crazy activism stories: Over at TIXC, someone just intentionally triggered their poison pill, and honestly I can’t remember a poison pill ever being triggered, whether unintentionally or intentionally (I can think of a few examples where someone slightly went over the ownership limit on accident and the company forgave them, but can’t think of examples of one actually getting triggered). Wild!

Update: after I wrote this, TIXC responded to “point out the consequences” of a poison pill being triggered, and Matt Levine wrote about the case and helpfully pointed out the one time a pill had been triggered.

Not to be too much of a #basicfinancebro, but I spent some time over the weekend rereading a bunch of Amazon shareholder letters and a few things popped out at me

First, the letters are semi-timeless. If you exclude names of specific product launches, you could read any of the letters and have no idea which year it was. An anecdote may show this best- I had printed out the letters and got the papers a bit mixed up; the 2005 letter got slotted between the 2011 and 2012 letters and I barely noticed the difference as I read throw them. Heck, if you re-read the 1998 letter and ignore the specific numbers, the focus on customer experience, hiring the right people, and setting audacious goals for a future with even more opportunities feels right in line with the more recent letters.

Second (and semi-related), Bezos (almost) never talks about macro in the letters. One of the reasons I started rereading the letters was an interest in how Bezos talked about the financial crisis. But he didn’t mention it once in his letters. As far as I can tell, the only time he really mentioned anything macro was at the very start of the 2000 shareholder letter, when he mentions a brutal year for capital markets and Amazon stock (down 80%+) before quickly transitioning to how bright the future is and how well they are performing.

Third, Bezos’s vision for the future is always super clear: maximize FCF per share by investing for the long term (in particular, by maxing out the customer experience). With the benefit of hindsight and how clear Bezos’s vision was, it’s easy to say Amazon “dominating” the world / performing to the level it has was “inevitable”. I think that’s a bit hindsight driven, but one thing is clear to me: if you were shorting Amazon in the past simply based on valuation, you weren’t thinking seriously about the company. My favorite letter is his 2005 letter, where he talks about using data to drive most decisions but going against the data with their decision to lower customer prices in the short term in order to improve customer experience / retention in the long term. Bells should be going off in anyone’s head reading that paragraph: the company is sacrificing short term profits to acquire more customers (or increase customer LTV) in the long term. Sure, maybe you can short Amazon on the thesis that customers would not have a positive lifetime value for some reason, but if you were short them then simply on valuation you were way too wedded to GAAP profitability numbers and not looking at the investment Amazon was making.

This made me giggle for some nerdy reasons: the 2013 letter discusses all of the things customers are using Mayday (their 24x7x365 live video service that they just quietly shut down) for. 475 customers ask to talk to Amy, the Mayday television personality. That’s no surprise as Amy is cute and friendly and people always want to talk to the cute / friendly semi-celebrity. A bigger surprise is that 109 Mayday customers ask for assistance ordering pizza. 109! That is insanity; it takes more effort to open Mayday and ask for help with a pizza than to simply call your local pizza spot and order a pizza (to say nothing of ordering it directly through the company’s website or app, though apps weren’t as big back then).

PS- the 2013 letter mentions Pizza Hut narrowly beating Domino’s in “Mayday orders”. Pizza Hut had 7,846 units in the U.S. at the time, while Domino’ had just under 5k. Maybe Dominos coming close to Pizza Hut in “mayday orders” is a small sample size or a meaningless number…. Or maybe it shows Domino’s was doing a better job of capturing internet order share of mind. Tough to say, but Domino’s stock is up ~4-5x since that letter came out, so it is interesting to think about the potential implications!

Sports media update

A core tenant of the monthly update: continued highlights of the increasing value of sports rights (mainly because of my love of MSG (disclosure: Long)).

Lebron to Lakers a big win for Charter (disclosure: long chtr)- the article contains some interesting stats / things to think about in relation to RSNs in general and MSGN (disclosure: long) in particular. Note that the Lakers contract is the biggest in the league: $180m/year for 20 years (MSGN's similar length contract for the Knicks is in the low $100m/year). The article also discusses how far ratings have dipped as the Lakers went from playoff contenders to tanking mode (the Knicks are awful and have been for a long time, but at some point they'll be less awful and ratings will increase significantly).

Amazon linked with remaining La Liga rights: if you’re bearish on sports rights, your worry is there’s a sports rights bubble. This bubble comes in a variety of forms, but at its most basic it’s a worry that the legacy TV bundle overpaid for sports rights and as people cut the cord nothing can pay sports leagues what the TV bundle currently pays them. I’ve always felt that argument is short sighted: sports league rights are one of the few things (perhaps the only thing) that can consistently drive people to your platform, and given tech giants focus on getting people into their platform there’s no way major tech giants aren’t going to play in the space (plus, given all the data they have on you, the tech giants are going to be able to monetize your sports viewership / engagement like crazy). This deal is just another example (albeit a small one) of how the tech giants are quickly moving in to sports rights internationally; it’s just a matter of time before they make a big move domestically. (See also: why Jeff Bezos covets Cristiana Ronaldo)

Facebook acquires 200m Premier League broadcash rights for southeast Asia- speaking of tech giants getting in to sports media….

Who would buy Fox’s 22 RSNs after Disney deal closes (disclosure: long FOX, short DIS)- I doubt Amazon buys them (I think they’d rather build their own solution to everything, and I feel like they’d rather a national contract than regional) but it is an interesting thought.

Confessions of a digital dinosaur: Esports is the next great traditional sports

How an ‘Overwatch’ Update Derailed One of the Most Dominant Teams in Esports

I’ve made no secret of the fact I’m obsessed with the future of eSports. I think things like this article are interesting: in the middle of the season, overwatch introduced a new character that completely threw off league dynamics. It would be like if the NBA removed the three point line one week before the playoffs started. I wonder if such sudden changes are good for eSports (more randomness, more excitement, more balanced field) or bad (game changes too often for casual fans to keep up with, players constantly complaining about changes). I would lean towards the later and think eSports will need to get used to not making wholesale changes in the middle of a season, but the ability to do so at a level that sports leagues can’t do (normal sports can’t ever change their physics, but an eSport could literally change the laws of gravity if they wanted to) is certainly interesting.

How Cord Cutting is turning local sports TV into winners and losers

Music Industry / Spotify

‘The Middle’ is a hit for Maren Morris after Demi, Camila, Bebe don’t make the cut

“In simple math, a million streams on Spotify averages out to around $6,800 in revenue, the lion’s share of which ($6,000) goes to the master rights holder (the label). The remaining (around $800) is allotted to the publishers, which then divide the earnings between their writers based on percentages of ownership (rates vary between paid and free streams). “The Middle,” as of this writing, had 236 million streams on the streaming service, which could net out $184,000 to the publishers — and that’s just for Spotify. Factor in other DSPs like Apple Music, and it’s already at $250,000. By comparison, Ed Sheeran’s “Shape Of You,” the biggest song of 2017, has 1.7 billion streams on Spotify. A songwriter’s share of that track easily tops a seven-figure payout.”

I’m not sure if I’ve mentioned it before, but I find Spotify absolutely fascinating. There are two big bear cases against Spotify. The first is, given their cost structure (streaming payments increase with revenue increases), Spotify has limited operating leverage and can never scale into the profits needed to justify their valuation.

Look at the quote from the Middle article: a label keeps >80% of streaming revenue. What services are they really providing today? Over time, doesn’t it make sense that Spotify (the firm with the best data) displaces them by offering artists a much larger cut of their streaming revenue? If that’s right, Spotify will see their gross margins increase significantly overtime while offering a much better deal to artists.

I think this line in the ‘Moneyball’ article is key- “Instrumental’s selling point is a dashboard called Talent AI, which scrapes data from Spotify playlists with more than 10,000 followers — 8,212 of them at the point I met Withey in the spring. ‘We took a view that to build momentum on Spotify, you need to be on playlists,’”. If they’re scraping the data off Spotify… why can’t Spotify just provide that data / analytics themselves? If they key to building momentum is being on Spotify, why isn’t Spotify working with artists and giving those artists premium playlist placement part of the endgame (doing so could erode consumer trust in Spotify, but no one has pushed back on Netflix favoring their own originals on the homescreen so far…).

The other thing to consider- over time, can Spotify leverage their ownership of the customer into different forms of entertainment? For example, if Spotify could push more people to listen to podcasts on their service (which they don’t have to pay streaming fees for), that could lower their streaming costs over the long term.

So I think the first bear case is kind of short sighted. Unfortunately, I am really worried about the second bear case: all of the major tech players (google, amazon, apple, etc.) seem to view music as strategic, and I’m worried they’ll undercut Spotify on price and forever limit Spotify’s potential. Unlike w/ video, people are generally only going to subscribe to one music service, and if Amazon is just going to give people their music service for free as part of prime (and monetize it by selling them related merchandise or perhaps event tickets over the long term), are there going to be enough people willing to pay for spotify versus just take Amazon’s free offering?

No position in Spotify, and I’m still thinking about all this stuff from a high level. But fascinating!

Related: Music investment firm purchases majority of the dream catalog for $23m

How E-Commerce is Transforming Rural China

I learned a lot about China and the major Chinese internet players reading that article.

All of the major Chinese tech companies interest me. I know a ton of very sharp investors who are bullish on them, and the thinking behind it makes sense to me. So I’ve always wanted to do more work on them, but every time I start thinking about them I come to my big worry: any company in China is ultimately going to be run with the government as its beneficiary, whether it’s explicitly (through nationalization) or implicitly (forcing them to make crazy non-economic investments in infrastructure or job guarantees), and outside shareholders (particularly foreign ones!) will never see a dime.

With that worry in mind, one line in New Yorker e-commerce article stood out to me. JD’s CEO says: “Our country can realize the dream of Communism in our generation,” he said. “All companies will belong to the state.” Isn’t that confirmation that the founder / CEO of one of the major Chinese tech companies believes that my “end game worries” is actually the plan?

Maybe I’m too bearish here; if you’ve done work on the topic and have other thoughts, I’d love to hear it.

I’ll note that I’ve heard the “the Chinese government would never do that; they want to encourage foreign investment!” argument 100x. I get it, but I’m not sure I buy it. Yes, they want to encourage foreign investment today…. But what do they want to encourage tomorrow, after all the foreign capital is in the country? Maybe at that point China is rich enough that they’re more concerned with international rule of law and order, but I’m not convinced that chance to capture trillions of dollars in one swoop (by nationalizing all orders of foreign investment) doesn’t overrule that concern. Perhaps that’s too cynical though; the bear case does always sound more interesting / intellectually compelling than the bull case…

PS here’s a clip from JD’s 20-f. It’s wild to me that it’s possible ~10% of their offices are based on fake leases!

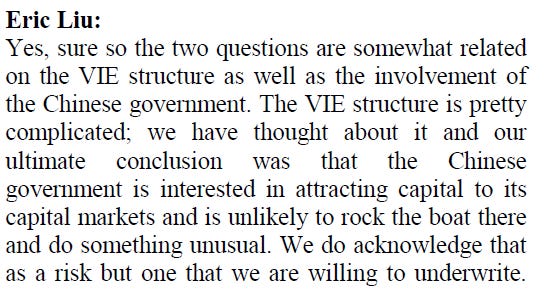

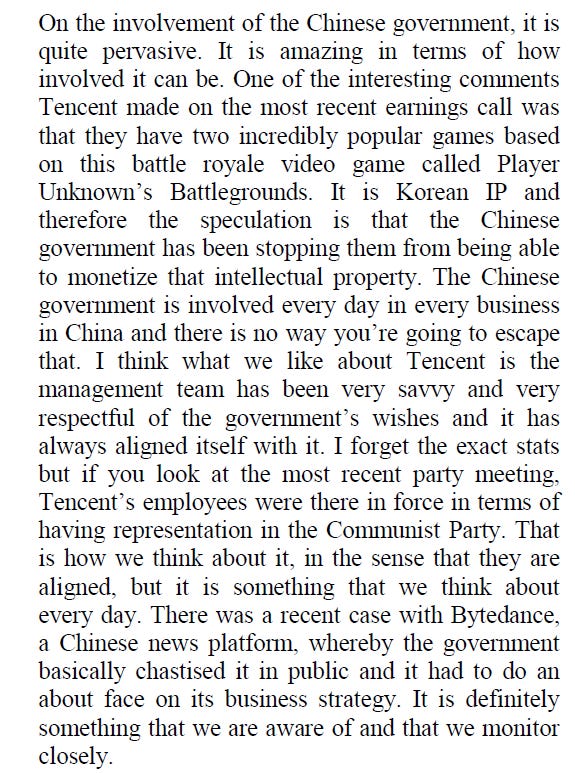

Tencent: (Sequoia 2018 Investor day transcript and For China, Tech Giant Tencent is both a national Champion and a Threat)

Speaking of Chinese e-commerce, some quotes from Sequoia’s Investor Day

One thing I worry with social media companies in general and Chinese ones in particular is how tempting a target they are for government interference, whether it’s regulating them to death or outright nationalizing them. Perhaps the latter is quite far out on the “tail risk” spectrum, but these are hugely powerful companies that have the ability to swing elections through small algorithm tweaks and they’re currently operating with basically no oversight or regulation; I can’t imagine that doesn’t change at some point.

For Chinese companies in particular, the VIE structure is a huge worry as well- as mentioned in the e-commerce piece, I know most people will say “the Chinese government is trying to attract foreign capital, so they won’t mess with the VIE structure”, but I wonder if that’s always the case….

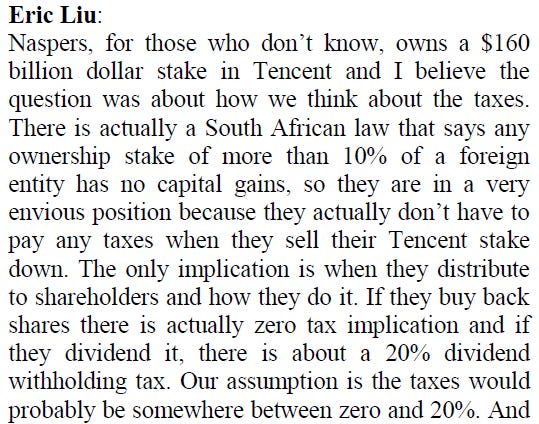

I have lots of worries around Naspers (disclosure: long a small position), but the big one that I think gets overlooked is on taxes. I get that South African law says they don’t need to pay taxes on their Tencent stake, but the stake is worth ~$200B. The South African capital gains rate is ~20%, so if Naspers had to pay a full tax rate on their Tencent stake (which is basically pure capital gains) they’d need to pay ~$35-40B. To put that in perspective, the South African government took in $92B in revenue and spent ~$103B in 2017, so the potential taxes on a Tencent sale would fund the government for almost half a year. I would not be surprised at all to see the government change the rules / laws to capture that large a prize; governments have done significantly worse for much less.

So if it seems like Naspers will probably get taxed on their Tencent stake, why bother going long Naspers? Nasper’s Tencent stake is worth ~$70/share; even if you assume a 20% tax rate on the stake, the Tencent stake alone is worth ~$56/share, more than today’s share price. Naspers probably deserves a conglomerate discount on top of that (the fact they won’t buy shares back at this large a discount is pretty insane), but I just can’t resist that large a discount for a premier growth company (despite the China risks). And if I’m wrong on the Naspers capital gains tax, all the better!

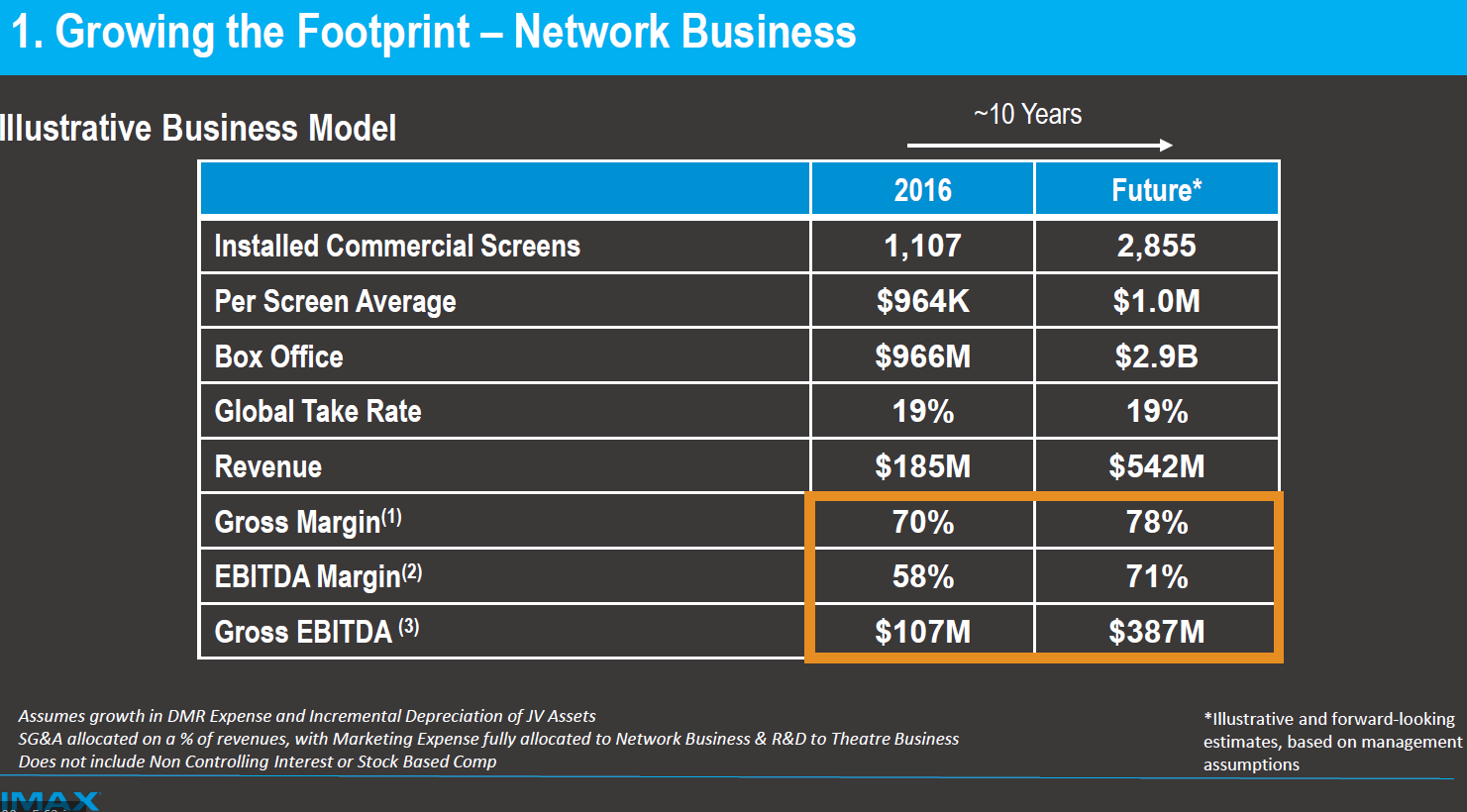

IMAX

One company I keep looking at is IMAX. The basic story here is: the company’s built out a big network of IMAX screens (actually they’ve generally JV’d them, but bear with me), and they take a cut off the box office when movies play at those screens. They’ve got a huge backlog to roll out new screens, and they think it’ll drive years of growth (slide below from their investor day).

Why I’m so interested is I think IMAX screens play well to the increasing “blockbuster” trend at movies (mid-budget movies go to Netflix or other streaming services, and the box office becomes more dominated by superhero movies and other spectacles), and the company seems to be hitting an inflection point in their capital allocation- historically they’ve invested into projects that have been disasters, like funding TV shows and rolling out VR pods in movie theaters (I’m not saying that were awful investments at the time, though I kind of think they were; just that they were disasters with the benefits of hindsight), but they seem to have shifted to just taking all their cash flow and buying back shares. Given a cheap valuation and strong cash flows, that type of capital allocation / levered free cash flow story would turn the shares into a blockbuster (sorry, had to) if they can deliver anywhere close to the growth they’re forecasting.

There’s also a bit of a SOTP story here- they publicly listed IMAX China and own ~68% of it, and the market value of their IMAX China holdings represents a huge piece of their EV today (it actually complicates the story a bit because you have to pull out all of the IMAX china financials from the holdco, but that’s a story for a longer post).

On the negative side, though, I’m worried that the technology advantage of IMAX versus normal movies seems pretty small (my fiancé and I went to see Ant-Man in IMAX (for due diligence, of course!), and we honestly couldn’t tell the difference between the IMAX showing and normal showings), and IMAX theaters have an increasing “comfort deficit” to reseated normal theaters (IMAX’s are rolling out La-Z Boy style seating, which pales in comparison to movie theaters that have done a full reseat to recliner seating).

So why mention all of this? If you’ve done work on IMAX, email / tweet me. Let’s swap thoughts.

Podcasts

Dude, you're getting a (heavily discounted) Dell (disclosure: long DVMT)

Other stuff I liked