Matching with IAC $IAC $MTCH

Matching with IAC $IAC $MTCH

IAC Interactive (IAC; disclosure: long) represents the opportunity to invest in a company trading for roughly the same price of its publicly traded equity stakes despite the presence of world class capital allocators with a proven history of realizing shareholder value at the opportune time, hundreds of millions in net cash on their balance sheet, and a grab bag of other (quite valuable) assets.

Let me start with a bit of background: IAC is a conglomerate controlled by mogul Barry Diller. The company has a long and storied history which makes for interesting reading (at various points in time, they’ve owned big stakes in everything from a Japanese home shopping network to Ticketmaster and a variety of other big internet companies) but is a bit beyond the scope of this article; however, what is worth noting is that an investment in IAC since its inception in 1995 has destroyed a similar investment in the S&P 500:

Anyway, today IAC has five main sources of value. I’ll go over them briefly below, but I’d encourage you to check out their FY16 letter for a bit more depth into their businesses:

Match.com (MTCH): IAC owns 80%+ of publicly traded Match.com, which owns Match, Tinder, and several other popular dating sites.

ANGI Homeservices (ANGI): IAC owns ~85% of ANGI Homeservices, which was formed by the merger of IAC’s HomeAdvisor with Angie’s List.

Video- IAC fully owns this segment, which includes Vimeo, CollegeHumor, Daily Burn, and a few others. The main driver here is Vimeo, a video sharing platform that is growing rapidly (Q2’17 saw paid subscribers increase 15% to 828k and gross booking up 20%)

Other segments- I use this as a grab bag of IAC’s other segments, which includes Applications (mainly browser extensions) and publishing (ask.com, about.com, and a few others). While these will almost certainly go to zero overtime, they are currently cash flow machines (applications will do ~$130m in adjusted EBITDA this year while Publishing will do ~$10m).

Net Cash- At the end of Q2, the IAC holdco (IAC consolidates MTCH, so you need to back that out) had ~$600m in net cash.

Offsetting some of that value is corporate expense, which runs at ~$120m/year and includes a very healthy dose of stock comp. I am not a fan of excessive stock comp and think this is clearly a value drag; however, if there’s one thing I’ve learned from studying John Malone’s Liberty complex, it’s that talented managers incentivized with heavy stock compensation can create really fantastic returns for both themselves and shareholders over time. I think that’s worth keeping in mind when looking at IAC’s stock comp.

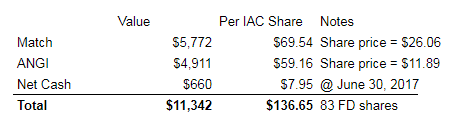

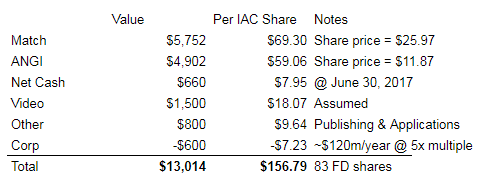

Anyway, the crux of the investment in IAC is that you are buying into the value of their stakes in ANGI + MTCH and getting everything else thrown in for free. Unfortunately, I’m not exactly the only one to notice this discount: IAC’s Q2’17 shareholder letter lamented this fact and went through the exact math to arrive at the discount. I’ve reposted the table they included below.

If I updated that table for today’s share prices (MTCH = ~$26; ANGI = $11.90), their Match shares would be worth ~$70/IAC share and their ANGI shares would be worth ~$59/IAC share for a total of ~$129/IAC share, a bit higher than today’s share price before factoring in everything else IAC owns (note: some MTCH employees exercised some IAC options in Q3 that caused IAC’s shares to go up a bit, but it was offset by MTCH giving IAC more shares to compensate them. So the numbers will change a bit in Q3, but the overall result stays the same).

The math on that is pretty easy, and the discount story is pretty visible (again, the company is highlighting it in their shareholder letters!), so I don’t want to focus on that too much. Instead, I want to focus on the two reasons I find IAC to be more attractive than the typical “trades at a discount to a publicly traded stake” story. Those two reasons are:

Management has a history of creating shareholder value and a clear path to doing it again

IAC has a history of successfully investing in “flywheel” companies, and all of their current big investments have the potential to be successful flywheels. Match is a clear secular winner that already has its flywheel started, and both Vimeo and ANGI have the potential to be successful flywheels.

Let’s start with the first point: Management has a history of creating shareholder value and a clear path to doing it again. There are plenty of companies that trade at a discount to the value of their publicly traded stocks, but almost all of them have some hair on them that could be pointed at to justify that discount (tax issues around disposing of the stake, controlling shareholder siphoning off value, the stake is an illiquid non-controlling stake, etc.) or raise questions around if the value will ever be raised. IAC has none of those issues: they control both ANGI and MTCH so the subsidiaries can’t play games with IAC’s stake / transfer value from IAC’s shares to other shareholders, IAC’s management has a history of creating value for shareholders, and there’s a clear path to a tax-efficient value realization through spinning off IAC’s shares in the subsidiaries along with a precedent for doing so. I’ll dive into valuation later, but to jump ahead a bit at today’s prices I estimate IAC trades for a >20% discount to its NAV. To make a quick comparison, Altaba (disclosure: long) trades for a ~30% discount to its NAV, and while I think that’s attractive, Altaba is also plagued by tax issues on their minority Alibaba shares that IAC doesn’t have on their stakes. For IAC’s discount to approach Altaba’s makes no sense to me.

Let’s turn to the second point: IAC’s history with flywheel companies / Match and ANGI are secular winners. Diller hinted at it a bit in this NYT interview, but IAC’s strategy has been pretty simple: IAC buys companies where scale improves the product. In their words, they look for companies where “the 10,000th customer on the platform improves the product for the 1,000th customer”. ANGI and specifically Match obviously fit the definition of a flywheel company to a “T”, and it’s my belief that the stock market today is undervaluing both of them.

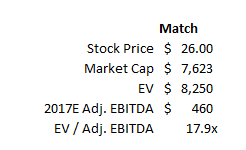

I’ll start with Match. Diving fully into the company is a bit beyond the scope of an IAC focused article, but I will provide a brief overview and focus on where I think my bullish view diverges from consensus. Match is the owner of most of the major online dating brands, including Match (of course), PlentyofFish, okcupid, meetic (the leading European dating site), and Tinder. At today’s prices of ~$26, Match trades for ~18x their 2017 EBITDA guidance (~20x if you back out stock comp) and ~20x unlevered FCF (Adjusted EBITDA less capex). While those numbers aren’t super cheap, I believe it well undersells what an industry leader with a wide moat like Match should trade.

It’s pretty clear that there are network effects in dating sites. You can think about this with a simple thought experiment: a dating site with only one user is worthless and a dating site with two users is basically worthless. As the number of users scales, the number of potential matches increases and the value of the dating site increases. So the network effects of a dating site are pretty obvious. I think what’s less obvious is just how strong Match’s moat is. Most investors worry that Match doesn’t have much of a moat for a variety of interconnected reasons:

Starting a dating app is easy

There are tons of competitors (Bumble, Coffee Meets Bagel, eHarmony), and user lock in is low, particularly on free sites (users will download and switch back and forth freely between all the sites)

Users will eventually “graduate” into a relationship and stop using the app, so Match needs to constantly compete for new users

Most of Match’s websites are broad and can be picked off by dating sites focused on different niches (i.e. Grinder for LGBT; Farmers Only for Farmers, etc.)

Match’s pay websites will be cannibalized by free / freemium websites

This was the main risk I was worried about at the IPO. At this point, Tinder has been around for several years and the main paysites have stabilized / are growing, so I think the major concerns are behind us.

I think all of these fears undersell just how strong Match’s moat is; it’s difficult for me to envision a scenario where we look back ten years from now and Match’s core brands aren’t still the dominant dating sites / apps and generating a lot more revenue than they are today. I base this on a few things

If you look back ten years ago, the big dating sites then (eHarmony, Match, plenty of fish) remain the major dating sites today. While there are some new players (notably Tinder and Bumble), it’s difficult to point to a major dating site from 10 years ago that has flamed out / gone away. This suggests dating sites and their networks have significant sustainability.

Perhaps it’s scary that some new dating sites (Tinder, Bumble, etc.) have emerged, so this isn’t like soft drinks where Pepsi and Coke have dominated for a hundred plus years. My theory here is that when the dominant method for connecting / dating changes, there’s a brief window when a new site / app can build a network before big players respond. That’s how Zoosk (desktop/browser to Facebook) and Tinder (browser / Facebook to mobile) got started. But the windows are rare, fleeting, and quickly replicated by legacy players (that’s why Match.com is still around and growing). It’s also difficult to see a new main form of connection coming that would replace mobile (the next mode of connection seems to be voice driven (think Alexa), and it’s difficult to envision a voice driven app).

While it’s easy to start a new dating site / app, it’s not easy to build a sustainable app that gains traction. Most of the new entrants into the space have flamed out. The reason is simple: any new feature (whether it’s an action like swiping, a new way of defining dating networks, or a novel way of paying) a newcomer invents can be pretty easily replicated by a larger player, but the newcomer cannot quickly replicate the larger player’s network or their tech spend (i.e. they can’t recreate how smooth already built apps or, nor do they have the data that can arrange matches / profiles to make the app more engaging).

Hinge is a pretty good example: the app was built around dating within your extended Facebook social network. The company eventually pivoted to a new “everyone pays” model when their growth stalled out and they couldn’t figure out a way to monetize.

It’s also worth noting that customer habit is difficult to overcome. Once a consumer becomes used to using an app / opening it up every day, it’s pretty difficult for a new app to switch them off that behavior. People engage with Tinder and other match apps constantly; that user habit is tough for any new app to break.

While it’s true Match needs to constantly grab new users, new users will download / join the app where most of their peer group / target dating market already sits, which should constantly refresh Match’s user-base / moat.

Consider a college- if everyone is already on Tinder, then when a new freshman come in they’ll join Tinder. Eventually those freshman become sophomores who push the new freshman to join Tinder.

It’s also worth thinking about customer re-acquisition. Not every relationship works out, and people who are coming out of relationships will likely turn to whatever app they used before they got into a relationship or whatever app their social circle is already in, which benefits Match’s established apps / network.

Put it all together, and I think significant evidence exists that Match’s brands / moat are much more durable than investors have traditionally given it credit for.

The other piece of the Match story that I think is interesting is Tinder’s monetization. Tinder just started monetizing in ~2015, and while the company hasn’t broken out Tinder’s individual income statements they have provided us with some details that suggest Tinder is growing at close to triple digit annual rates currently (for example, Tinder average paid member count was up 86% YoY in Q2’17). Obviously that growth can’t continue forever, but given how new Tinder’s monetization is and the success of their recent Tinder Gold launch, I think Match is just starting to scratch the surface of Tinder’s monetization potential. It’s also worth noting that the continued tailwind from online dating’s increasing social acceptability will be a huge driver for all of Match’s brands.

There are a bunch of other things to think about with Match, but the bottom line to me is that at today’s pricing you’re creating a fast growing market leader with a defensible moat for <20x EBITDA. There’s no pure play comp for Match, but Twitter trades for a similar adjusted EBITDA multiple despite huge stock comp, no growth, and a questionable long term moat. LinkedIn sold to Microsoft for ~24x adjusted EBITDA (and, again, their stock comp was way higher than Match’s). As Tinder continues to grow and become an increasingly important driver of the company, I’m not sure why Match can’t trade at or above Linkedin’s multiple in the near future, which would imply a price of ~$30 with continued accretive growth as their businesses scale.

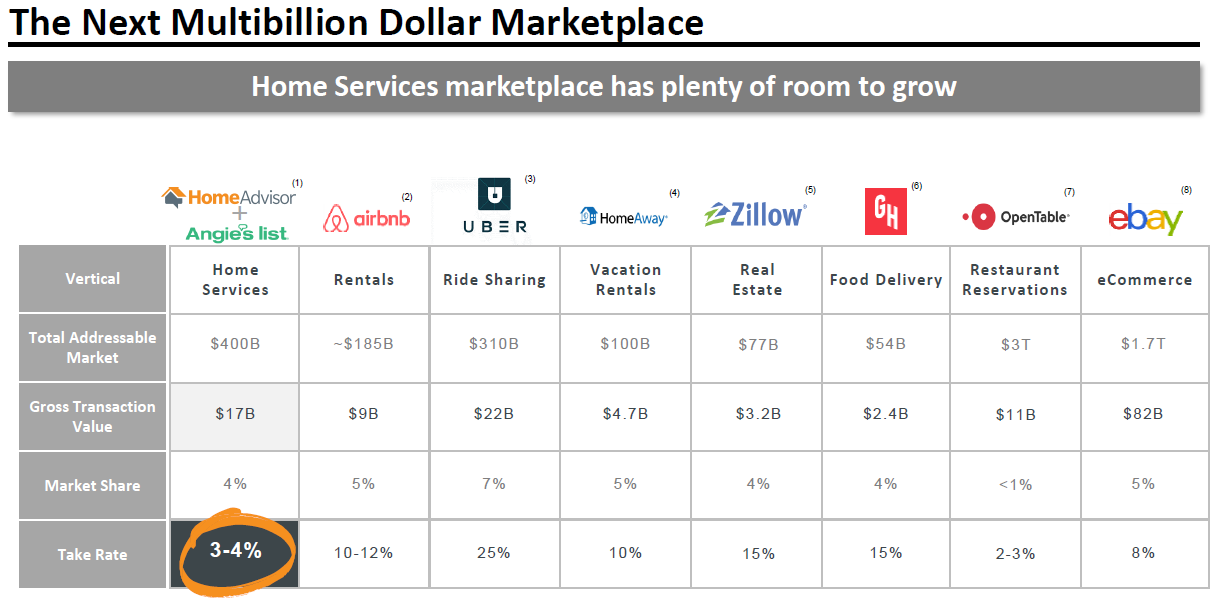

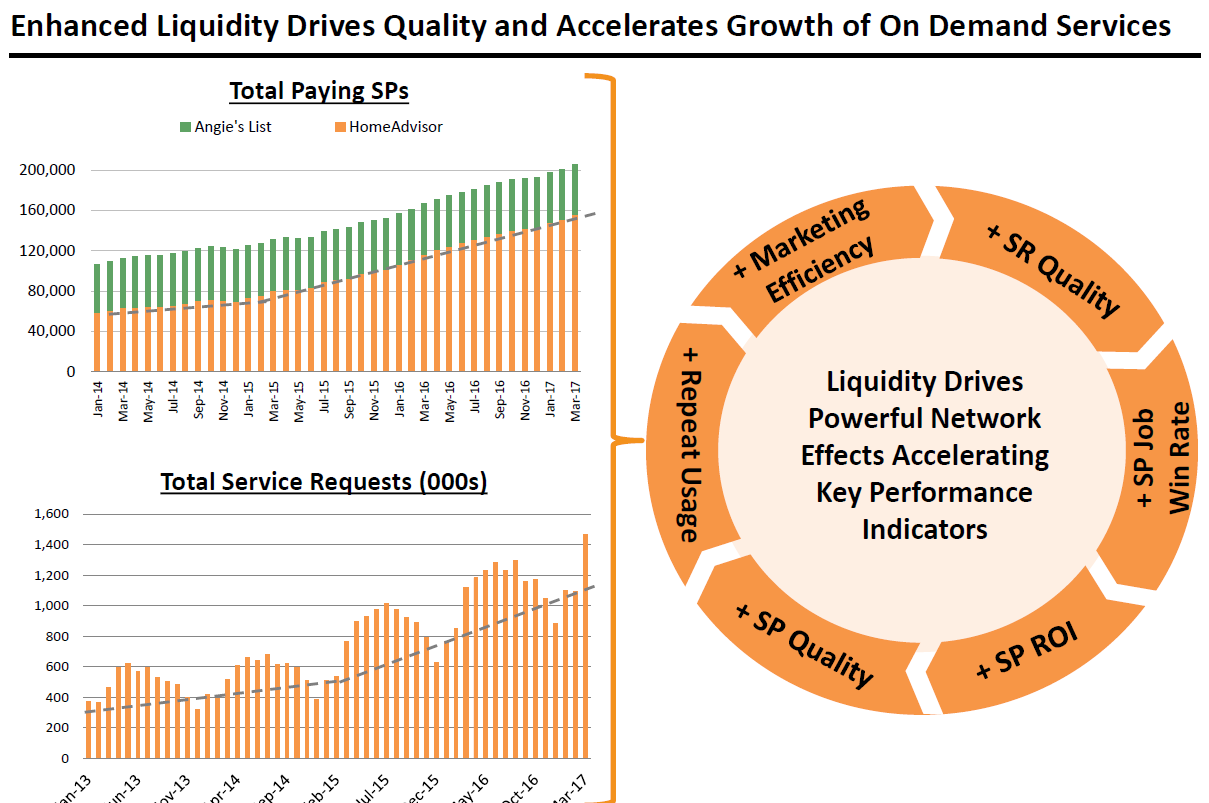

Let’s now turn to ANGI Homeservices. This company was formed by the merger of HomeAdvisor and Angie’s List (which was announced in May and completed last month), and IAC is clearly bullish on the potential for the combo to create and capture significant value.

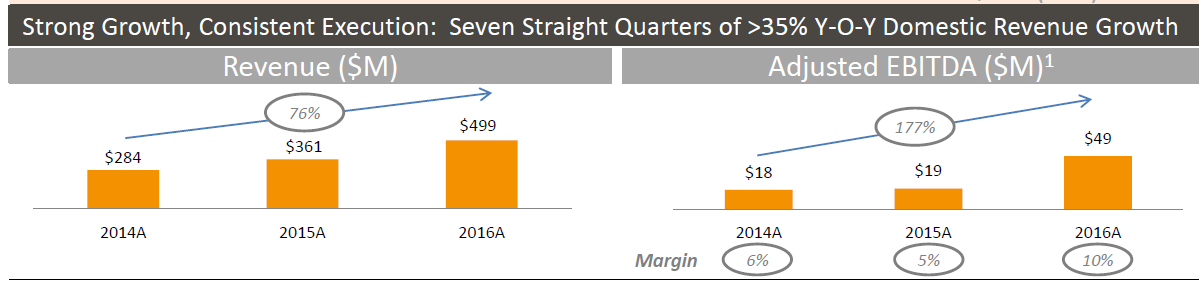

The core of the new business is HomeAdvisor. HomeAdvisor is a marketplace for homeowners and service providers. The basics of the business is home owners can go on and request a variety of home services (plumbing, remodels, etc) and get matched up with several service providers who can provide them quotes and availability. The business has performed fantastically over the past few years, with domestic revenue growth exceeding 35% annually and adjusted EBITDA margins doubling.

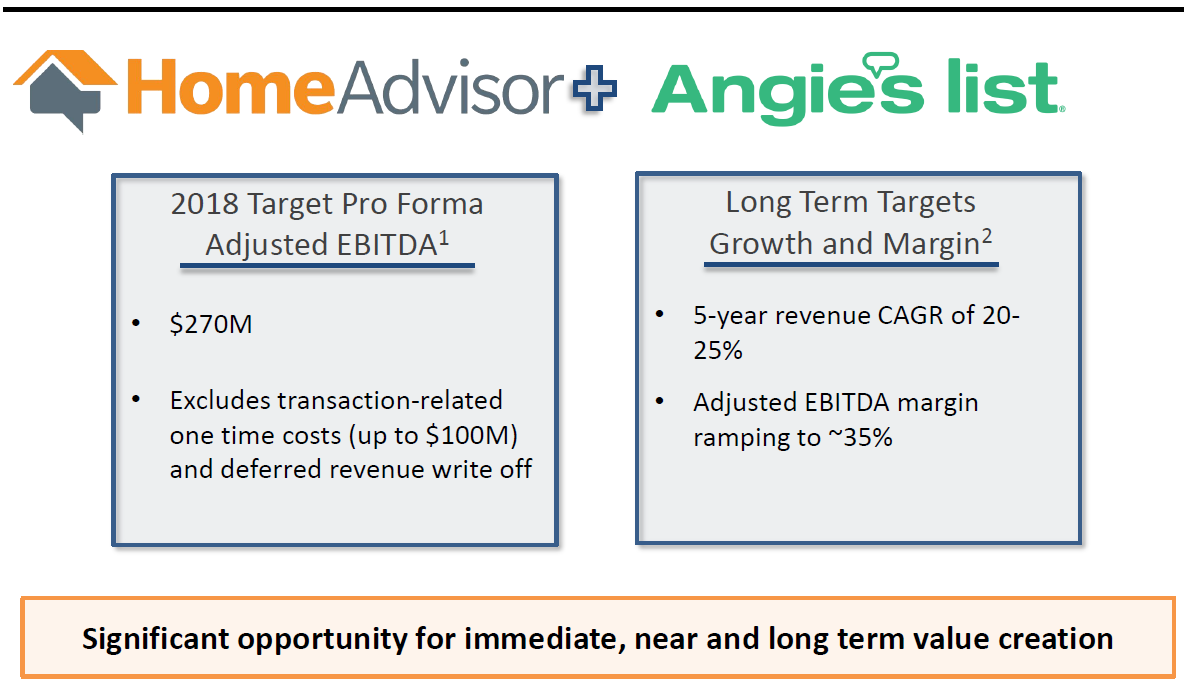

The basic thesis behind the merger is simple: take Angie’s user base and traffic and connect them with the HomeAdvisor network and technology. The increased traffic from Angie will improve HomeAdvisor’s network and get the flywheel turning a little quicker. As the flywheel starts to gain momentum, the value creation opportunity is huge: IAC is forecasting the combined company will do ~$270m in EBITDA in 2018 while growing revenue at 20-25%/year and ramping EBITDA margins up to 35%. ANGI’s EV is currently ~$6B, which will clearly prove much too cheap if ANGI can even come close to hitting IAC’s projections.

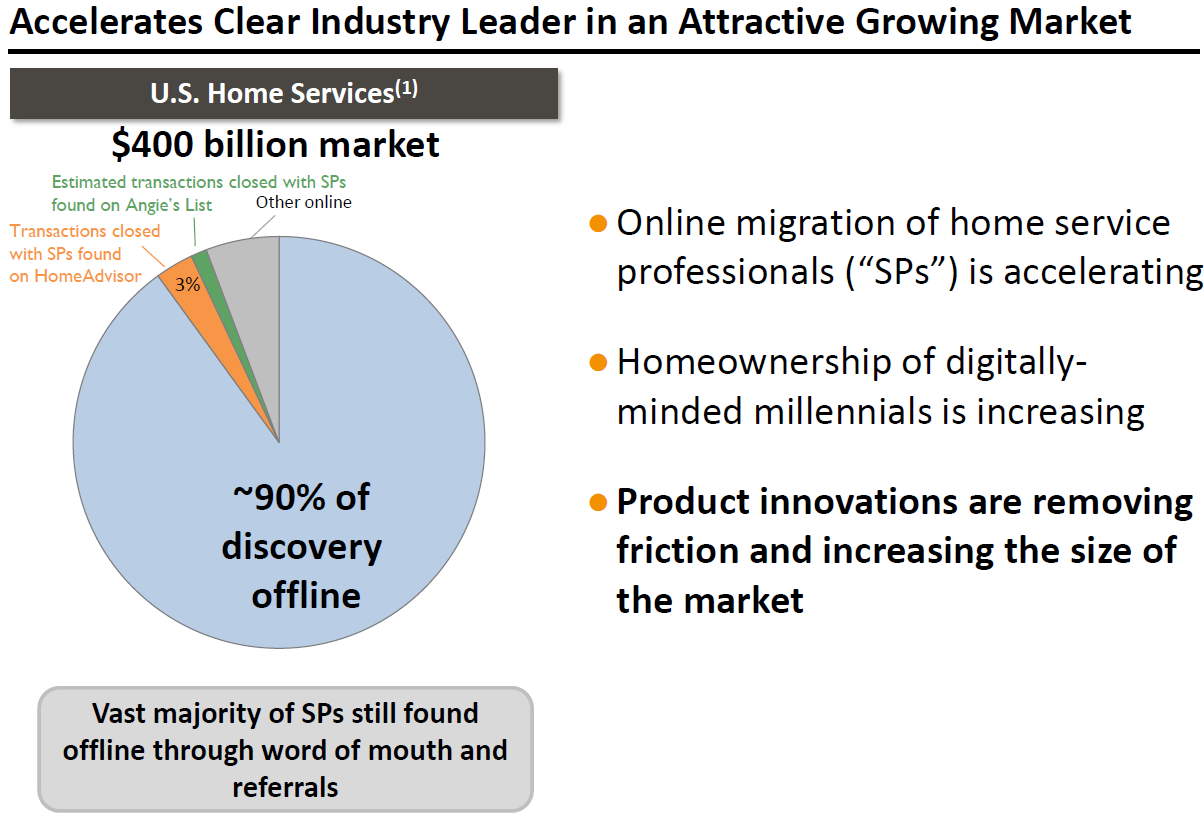

The biggest question with ANGI is clearly how much of the market they can penetrate, as they estimate ~90% of discovery is still done offline through things like word of mouth and referrals. Penetrating that 90% will go a long way towards determining if ANGI can approach an AirBNB type valuation or if its path looks more like an OpenTable, which Priceline bought for ~$2.6B and subsequently wrote off ~$1B from the purchase price.

My personal guess is that IAC is right and ANGI can continue to take share from offline discovery. Offline discovery is slow (you need to go ask a bunch of different people if they’ve ever had the type of work you’re looking for done, then see if they’d recommend the person who did it, then call and set up an appointment, etc.) and inefficient (wildly varying experiences with the same provider). Having a website that allows you to quickly find top rated providers and immediately book a time with them that is convenient for you should create significant value.

To wrap it up, I’m pretty bullish on the long term potential of both ANGI and Match, which will be the two main drivers of IAC’s value going forward. And, at today’s share price of ~$125, investors in IAC are basically just paying fair value for IAC’s MTCH and ANGI stake and getting everything else thrown in for free. So what else does IAC own?

Net Cash: IAC has ~$660m in net cash, or ~$7.80/IAC share, at 6/30/17

Vimeo / Video Segment: Vimeo is a video-sharing website. At Q2’17, the platform had 828k subscribers (up 15% YoY) who paid >$100/year to subscribe. Given that growth rate and the multiples similar SaaS video platforms get, Vimeo is probably worth well over $1B. The video segment as a whole is on pace to do well over $300m in revenue in the next twelve months. We don’t have a ton of info here so it’s tough to definitely pin down exactly how much this segment is worth; however, given the growth rate and loose peer multiples I would guess it’s worth ~$1.5B, or ~$17.90/share.

Other segments: I lump in both their Publishing segment (ask.com, about.com, dictionary.com, and some others) and their Applications segment here. These aren’t the most valuable businesses of all time, but they throw off a ton of cash and are quite stable (publishing did $132m in EBTIDA in 2016 and is on pace for a similar number this year). In total, I value them at ~$800m, or ~6x their combined 2017E EBITDA. This is probably a bit conservative given they generate tons of FCF with almost no capex, but given they’re declining segments in the long run I’m fine with it.

IAC owns their corporate headquarters, 555 W 18th Street. It was built specifically for them and, in 2007, the NYT referred to it as a 10-story $100m structure. I would guess it’s worth substantially more than that at this point (they sold the property development rights to a nearby property for $35m last year) given the substantial appreciation in NYC buildings over the past ten years, but I haven’t included value for it anywhere.

Corporate: IAC spends ~$120m in corporate overhead / year, split roughly evenly between stock comp and cash expense. I estimate this is a drag of ~5x annual spend, though given management’s history of value creation that’s probably pretty draconian.

Put it altogether and you get a total per share value of ~$157.

So how does this play out? Over time, I’d expect IAC to continue to invest successfully in flywheel companies. Some will probably never get the wheel turning, but given management’s track record I would not bet against them being able to either successfully start some flywheels internally (note that Tinder was developed inside Match) or acquire some just as they are getting started at attractive valuation.

Key risks

Tax- I’ve assumed no taxes on their ANGI / MTCH or other stakes because I believe they have several avenues for tax efficiently monetizing them. Given IAC’s tax basis, if that assumption proves wrong, today’s discount would be more justified.

Match / ANGI – The majority of the value comes from Match and ANGI. If I’m wrong about either of the companies’ network effects / moats, value would suffer.

Amazon is a company I’m particularly worried about when it comes to ANGI, as Amazon seems increasingly focused on last mile services, but honestly that fit just doesn’t seem like a good one for Amazon (handling hundreds of local contractors and matching them with customers seems out of what the normally do).

I’ve always worried Facebook would make a move into dating, but if they haven’t done it yet it seems unlikely they’d change course this late into the game.

Key man risk- IAC is controlled by Barry Diller, insiders are paid very well, and Diller has made moves to try to consolidate his control before. Obviously a risk and concern, but it’s tough to argue with IAC’s history of shareholder value creation here.