Cord cutting and other cable risks $CHTR

Cord cutting and other cable risks $CHTR

An increasingly long time ago, I was an analyst for a consulting firm. In ~2012, we were working with one of the big cable companies and I was on a call discussing some work I was doing modeling their finances going forward using different assumptions for cord cutting (things like what if 3% of customers cut the cord every year versus 5%). My focus was, in particular, on how it would impact the company’s cash flow going forward. I was going through some different assumptions when one of their top managers jumped on, cut me off, and said something along the lines of, “It won’t matter. We’ll just raise their broadband prices when they drop TV.”

I’d forgotten about that experience until pretty recently, and ,unfortunately, forgetting that experience has certainly cost me a lot of money, as I had habitually avoided investing in any of the cable companies because every time I looked at them I just thought “cord cutting + competition from fiber overbuild (Google Fiber) + faster wireless = declining industry,” which is actually the complete opposite of how I feel about the industry after spending a lot of time looking at it (I think it's a secular grower for years to come).

But that experience popped in my mind over the past few days, as I’ve been talking to a few other fellow cable investors after my recent post on Charter. And those three risks (fiber overbuild, faster wireless / 5g, and cord cutting) were, not surprisingly, what most of them are focused on (I also worry about some type of regulatory crackdown (a la Europe, which seems to have much tighter regulation on telecos that limits earnings / returns ) or in a super bear case a crazy regulation that tries to turn cablecos into a regulated utility, though admittedly that’s a super tail risk and almost certainly not happening under this administration). I thought the takeaways were pretty interesting

Most of them agreed with me that fiber overbuild worries are behind us at this point: Google Fiber couldn’t make it work, and Verizon pulled back on FiOS as well, though AT&T is still building out the requirements from its DTV merger and could make a dent.

A somewhat related concern so I’ll throw it in here- several investors wondered where penetration levels top out at. Charter and Comcast are both approaching 50% homes penetrated with broadband; how much higher does it go? 55%? 60%? What happens when the growth from natural penetration increases slows? This wasn’t a huge concern of mine- I think investors at today’s prices will make money on CHTR whether penetration rates top out at 50% or 55% or 60% (thought they make a lot more money in the later than the former) because they have some pretty serious untapped pricing power; my bigger concern is a super bear case where 5G takes penetration from 45% to 25% or cable has to slash broadband prices by 40% to be competitive with 5g (see point 2 below).

Another related concern: most everyone agreed capex would fall over time, but there was a lot of debate over how far it could / would fall. I said ~$100 in capex / home passed in my last post and I was by far the lowest person. I was basing some of that target on Altice, who is currently spending ~$112/pass and dropping, but there was both a lot of skepticism over the Altice model and some concerns that Altice’s density in some areas gave them a bit of a leg up in lowering capex.

5g / faster wireless was an interesting topic. My bottom line remains consistent with my last write up (as I dive more into the industry, it becomes clear that cable’s infrastructure will prove critical in some form in most 5g worlds I can envision, and that Verizon and Sprint / Softbank both approached Charter provides me huge confidence in that thesis). I wasn’t able to find any investors who really took the other side of that bet (that 5g will make cable completely obsolete in some way), though I was talking to a pretty biased crowd since most of them were long Charter in some form.

An interesting thought I’ve been toying with- what if the real threat as the landscape evolves is not wireless destroying cable but cable eating wireless? A basic evolution would be cable offers an unlimited package that simply offloads all your data consumption to their wifi whenever you’re in home and then made use of an MVNO to provide wireless whenever you weren’t connected to wifi. Since most data is consumed in home and a cable company would have huge buying power if they were aggregating tens of thousands of customers to buy blocks of data from telecom companies, you could pretty quickly see how this type of bundled offering would outclass a pure 5g offering from a wireless company: the cable offering would be more reliable and faster in home given the wired connection, and the cable company could price competitively as they’re leveraging their existing infrastructure for the most part and using huge buying power when buying any data they need to offload. I could envision an even more aggressive case where the cable company turns every house that’s signed up for their service into a general wifi hotspot for their customers, which would allow them to offload even more data on the network. I don’t know how it plays out, but it’s certainly encouraging to think about when you see that Comcast’s MVNO seems to be gaining a bit of traction in its early months.

I think several European cable companies have experimented with this type of cable driven quad play offering, though I admittedly need to do more work there.

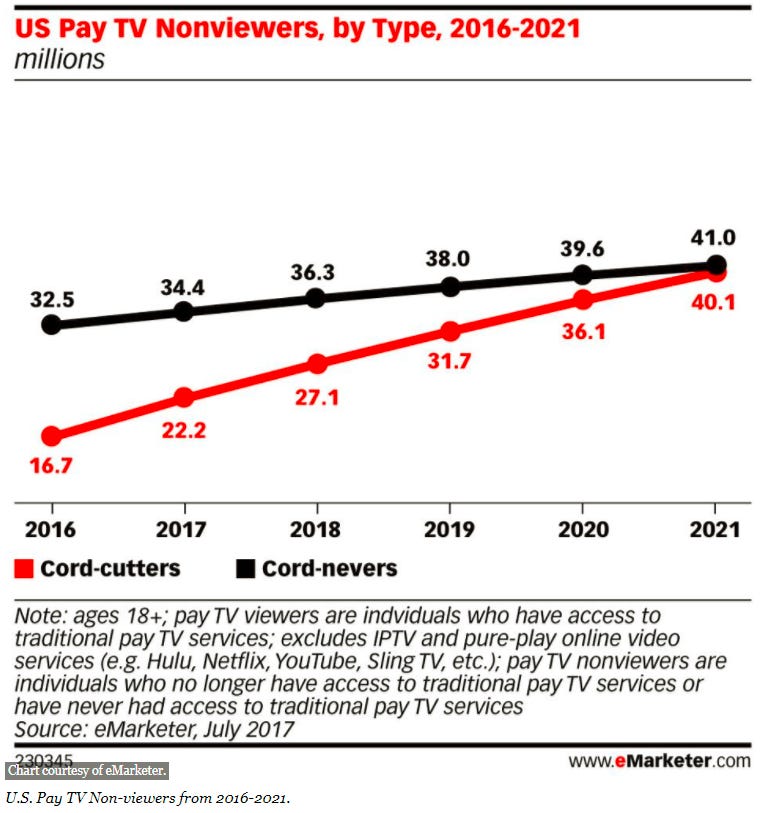

What I was most surprised about was the divergence in thoughts on cord cutting. Don’t get me wrong: no one who I talked to thought that increased cord cutting was going to lead to Charter going out of business. But a lot of people who I talked to thought trends in cord cutting would be the difference between the stock being “meh” over the next few years (if cord cutting really accelerated) and the stock being a home run (if cord cutting slowed or reverse). So I wanted to spend some time on cord cutting.

Let’s just start with a quick definition: cord cutting refers to dropping the traditional cable pay TV package and getting your media fix from OTT services like Netflix, YouTube, Amazon Video, etc (cord-never refers to something similar; it’s simply a person who has never even paid for the cable TV Package). Cord cutting is a separate worry from the 5G replacing cable worry; a cord cutter generally still needs a relationship with a cable or telecom company to give them high speed internet. The doomsday case for a cable company is the rise of cord cutting combined with 5G offering a competitive / replacement service that makes the cable wire into someone’s house irrelevant. I’ve discussed the 5G concerns above so we won’t mention them again; the thing to remember about cord cutting is it’s focused purely on the cable pay TV side and the cord cutter still needs a relationship with a cable company or teleco to get high speed internet.

There’s no doubt that cord-cutting is a trend and it’s probably one here to stay. To me, it’s simply about the value proposition: the cost proposition of Netflix at ~$10/month with no ads and the ability to watch whatever you want whenever you want to versus cable TV at >$50/month for hundreds of channels filled with ads and the requirement you watch what they are showing when they are showing it is not even a contest.

But I’m just not sure that cord cutting really matters to cable companies. Yes, it’s nice to have customers subscribe to more products as it decreases customer churn and you probably make a bit more money off of them. But programming costs have risen so high that cable companies make basically no money on their video subs.

I am far from the first person to point this out. Cable One (CABO, a rural cable provider) has been hammering this point home for years; here’s a slide I pulled from their December 2016 investor deck that I think illustrates this point nicely.

CABO has made their strategy very clear: treat video and phone service like a pass through cost if a cable sub decides to sign up for them and make all their money / margin from internet service. And you can see that strategic decision pretty clearly in their numbers: Cable One’s Video penetration (% of homes that their systems passed who have subscribed to their video service) was 19.2% at 12/31/16 versus Charter at 35% and their voice penetration was just 6.9% versus Charter at 23.1%. If video was really profitable, you’d expect Cable One to be way less profitable than Charter. But it’s tough to really see that in their numbers:

Well, that’s pretty interesting, no? CABO is less profitable on a homes passed basis, which makes sense given substantially lower internet penetration. But on a profitability per relationship basis, CABO is actually well ahead of CHTR despite substantially lower double / triple play subscribers. I do think there is a lot of noise and idiosyncrasies in those numbers (CHTR still integrating two acquisitions; CABO seems to have been a bit more aggressive on price than Charter), but if video and internet were really adding to the bottom line, there’s no way CABO should even be approaching CHTR given those numbers.

Now, I don’t want to oversell the meaning of the economics of one small rural cable provider. And, again, I think having a double/triple play customer almost certainly adds value when you look at the reduced churn over a customer’s lifetime. But the fact that CABO is even in the same league as CHTR on profitability per relationship suggests to me that there’s simply not much margin on the video / phone side, particularly once you consider that CHTR’s scale gives them better leverage with content providers so their apples to apples content costs versus CABO should be lower / video margins higher.

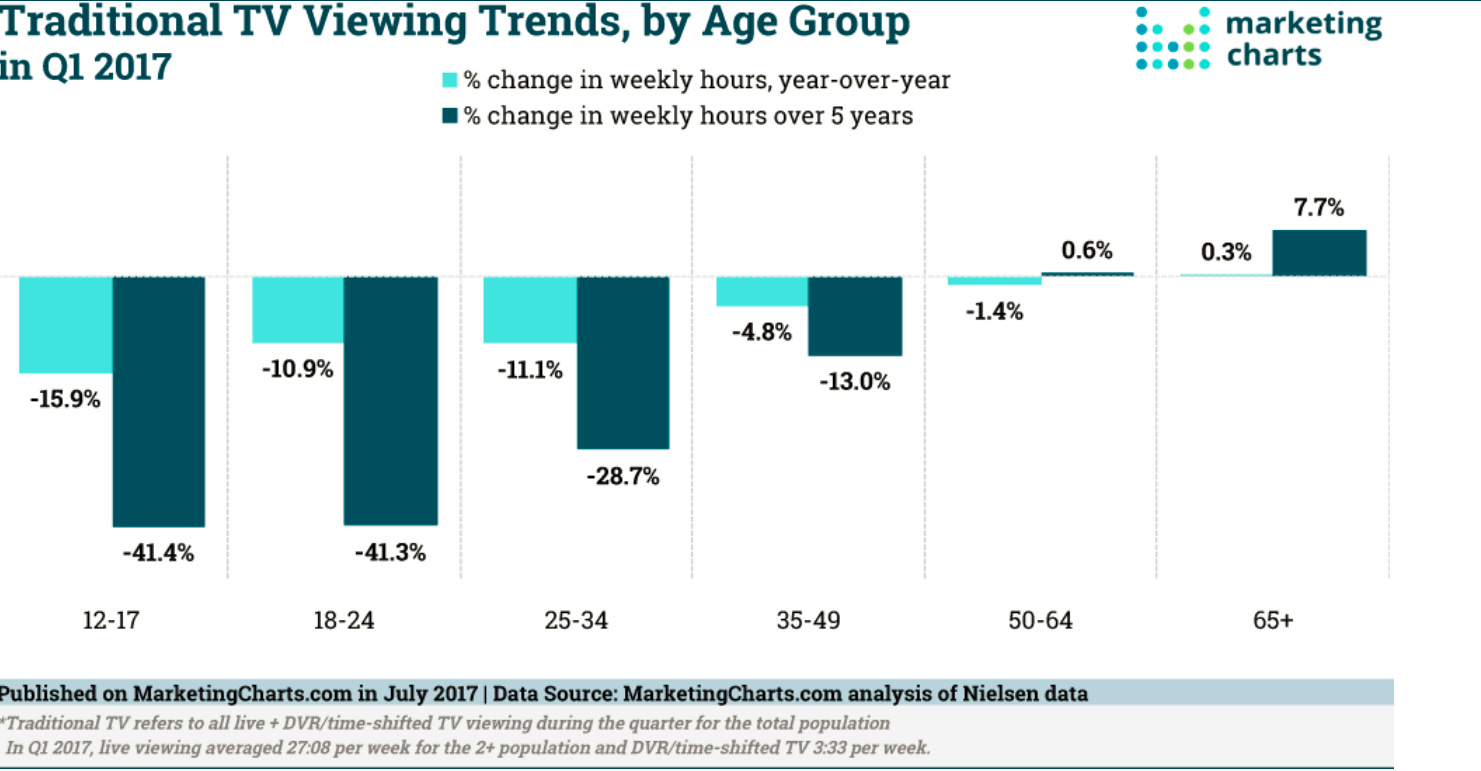

Here’s something else interesting I’ve been toying over. Traditional Pay TV isn’t being affected by cord cutting alone; overall viewership of Pay TV by the people who still pay for it is going down as well. This makes sense: we have way more competition for our time (Netflix, dancing cat videos on YouTube, video games, etc.), and that should naturally lead to less time devoted to traditional TV. And this isn’t just a small drop: we as a country are watching substantially less traditional TV.

The charts below show the ratings for some primetime ABC and CBS shows. Obviously they’re less scientific than the Nielsen ratings (maybe viewers just hated the CBS / ABC lineups and switched to watching something else in the cable TV package, and these numbers are clearly impacted by cord cutting as well), but I actually like the way they illustrate this phenomena more.

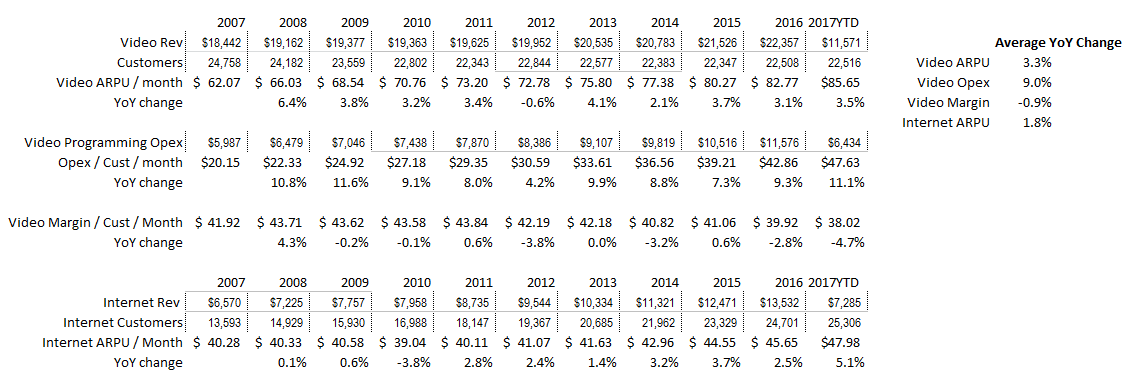

Anyway, the bottom line is that not only are less people paying for traditional cable TV, but those who are paying for it are watching substantially less of it. If people are watching less of it, you’d think that means that are getting less value from it. But cable video costs have continued to go up much faster than internet costs. The data below shows Comcast’s video revenue, internet revenue, internet and video customers, and their video opex for the past ~10 years. I simply lifted all of these numbers from their trending schedules (you can still see the formatting Comcast provides them in).

So, over past ~ten years, Video ARPU has gone from $62 to $86, video programming opex has gone from $20 to $48, and video margin has decreased slightly from $42 to $38. Internet ARPU has increased from $40 to $48.

Here’s my core question: if I just add the current internet ARPU and video ARPU together, the average double play video + internet customer is paying Comcast ~$135/month (this is a huge simplification but bear with me). Comcast is saying $86 of that revenue is attributable to video while $48 of that goes to internet. If I’m the consumer, is that how I’m bucketing the value allocation in my head? My guess is no, the consumer probably thinks they are getting the majority of value from their broadband services. Looked at another way, if I just take the pricing of each offering ten years ago as the starting point, it’s nonsensical to me to think that the value of delivering liner video has increased ~3% annually versus <2% for high speed internet when people are watching less traditional video in general and using the internet to stream more.

All of this is a longwinded way of saying the more I look at these numbers and the industry overall, the more I come around to the CABO way of thinking: video revenue doesn’t have much (if any) profit to it, and fears over cord cutting are a side show for cable investors in the long run as basically all of cable’s value is being generated by the high speed broadband offering.

Counterpoint: I know this post is long, but for those of you still reading here’s a fun little counterpoint. One of the key things Netflix has used is their customer viewership data to determine which shows to produce, renew, etc. Cable owns that data for their cable subscribers when they watch cable TV, and it’s not clear to me they’re doing anything with it currently (perhaps Comcast is quietly feeding their data to NBC, but I haven’t seen anything suggesting they’re leveraging that data). Even if providing video is low margin overall, isn’t gaining the viewership data for your subscribers valuable going forward? As ad targeting gets better, aren’t there ways to leverage that into more ad revenue? Or, thinking more broadly, could cable companies look to partner with content creators and leverage the cable companies data / access to customers to create more valuable content and own a stake in it (Charter has dabbled their toes in these waters with AMC, but nothing huge yet)? I guess the bottom line here is that while video may be low / no margin today, looking longer term it’s actually pretty valuable both because it brings tons of data about customer viewing habits and because it reduces customer churn which helps protect the valuable high speed internet franchise.

One last bonus thought- The cost of cord cutting and switching to OTT services can add up. There’s a reason the cable bundle was so powerful: bundling tens of millions of customers together gives huge buying power (which is also the reason why video may be 0% margin for a small player like CABO but turn some profit for a larger player like CHTR) and allows consumers to get access to a huge variety of content. As cord cutting continues, we’ll likely see new bundles start to form (Amazon Prime is basically a video + music + delivery bundle, T-Mobile may be forming another with Netflix on Us and AT&T is clearly thinking about another with their purchase of HBO, and Hulu and Spotify are offering a bundle for students, and Apple may even be thinking about a hardware + entertainment bundle to differentiate the iPhone). I wouldn’t be surprised if cable, who already owns tens of millions of customers, can offer new and innovative bundles as the traditional pay TV bundle collapses (something like using their buying power to offer a bundle of Netflix, HBO, and hulu for $25/month?). Who knows how it evolves, but recent history has shown that owning tens of millions of customers (and having an automatically recurring payment on their credit card) opens up tons of strategic options.

Additional reading: here’s Nielsen’s Q1’17 audience analysis report if you want the original data for Traditional TV watching trends.